5 Reasons Investors Can’t Get Enough of Saudi Aramco’s Debt

5 Reasons Investors Can’t Get Enough of Saudi Aramco’s Debt

(Bloomberg Opinion) -- Saudi Aramco checks just about every box for a bond investor.

Not only is it the world’s largest oil company, it also generated the most profit of any corporation across the globe in 2018. Moody’s Investors Service says it has “many characteristics of a Aaa-rated corporate,” yet with a rating four steps lower than that, it still offers a decent yield pickup. It has never issued dollar debt before, a big perk for money managers who crave diversification. And it has the star power of JPMorgan Chase & Co.’s Jamie Dimon behind it. Put it all together, and it’s little wonder that the $10 billion deal has already received more than $60 billion of orders.

That’s not to say it’s without risks. As my Bloomberg Opinion colleague Liam Denning pointed out earlier this month upon reviewing some 500 pages of offering documents, the overarching concern is Aramco’s tight link to the Saudi government. The biggest winner from the sale probably isn’t Aramco but rather the sovereign wealth fund. It’s also worth wondering what the energy sector — and therefore the financial situation of Saudi Arabia itself — will look like in 20 to 30 years when portions of this bond sale mature.

But those are clearly an afterthought, judging by Aramco’s initial price talk. The sale is set to wrap up Tuesday. Let’s drill a bit deeper into five possible reasons investors are gobbling up what’s being called the “most highly anticipated sale of the year.”

1. New Name

This offering marks Aramco’s debut in the dollar-bond market. That’s a bonus for money managers because it helps diversify their portfolios.

Not only does it add a new “name” to the market, but Aramco also represents higher credit quality when more than half of the Bloomberg Barclays U.S. Corporate Bond Index is rated in the triple-B tier. Aramco, by contrast, has an A1 grade from Moody’s and an equivalent A+ from Fitch Ratings. While lower-rated securities are somewhat back in vogue, nothing has changed about their inflated debt levels and stretched balance sheets. That’s not the case for Aramco.

2. Unique Risks

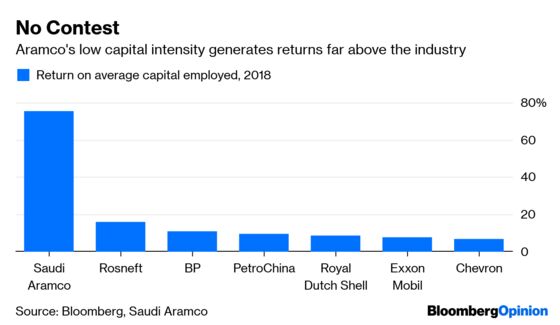

Aramco has “minimal debt relative to cash flows, large scale of production, market leadership and access in Saudi Arabia to one of the world’s largest hydrocarbon reserves. These features position it favorably against the strongest oil and gas companies,” Moody’s analyst Rehan Akbar wrote in a report earlier this month. Its adjusted debt-to-book capitalization of 14.7 percent as of the end of 2018 was even better than top-rated Exxon Mobil Corp.

The best way to visualize Aramco’s advantages is this chart that Denning compiled of the integrated oil industry’s main financial metric, return on capital employed:

That’s nothing short of phenomenal. Still, Aramco’s location and its ties to the government pose unique risks. It’s worth remembering that the entire point of this bond sale is to buy a majority stake in Saudi Basic Industries Corp., the country’s largest listed company. Denning wrote that it “effectively shuffles state assets from one pocket to another.”

Again, for investors, it comes back to diversification. In many ways, Aramco and Saudi Arabia are one and the same. So adding quasi-sovereign obligations may simply be more palatable than taking on debt of another leveraged American company.

3. Yield Spread

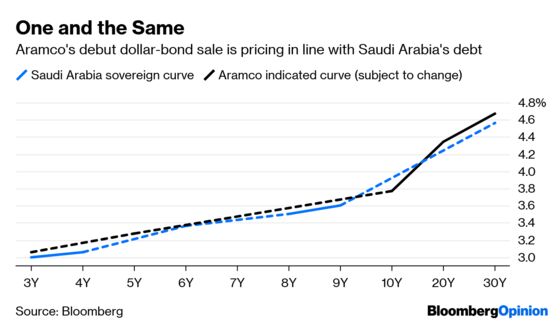

To be sure, there are lines that some investors won’t cross. Jim Barrineau, head of emerging-market debt at Schroders Plc, told Bloomberg News that he wouldn’t buy Aramco’s bonds at a rate lower than the Saudi government’s. That’s a very real possibility, given the initial price talk was in line with the sovereign curve. My Bloomberg Opinion colleague Marcus Ashworth figures that with such demand, Aramco can either boost the size of the deal or offer even lower yields.

While far from a perfect comparison, the Bloomberg Barclays index of U.S. corporate debt has an average maturity of 11 years and a spread of 116 basis points to Treasuries. Aramco’s 10-year portion may have a yield equal to the benchmark 10-year Treasury note plus an extra 125 basis points. In that sense, it might not be a bargain, but it’s not vastly overpriced either.

4. Favorable Market

The broad bond market is on solid footing. The Federal Reserve looks as if it’s done raising interest rates indefinitely, pushing credit spreads to the narrowest in months. Only about $16 billion of investment-grade U.S. bonds priced last week, short of estimates of $20 billion to $25 billion, potentially freeing up extra cash among fund managers who saw $2.9 billion come pouring in during the week ended April 3. It was the 10th consecutive week of inflows.

Plus, in a boon to Aramco, oil prices are the highest in five months.

5. Dimon, FOMO

To top it off, some star power is backing this bond sale, and persistent updates on the swelling order book may have created a fear of missing out.

Dimon, JPMorgan’s chief executive officer, spoke at a lunch in New York last week to market the deal, according to a person with direct knowledge of the matter who spoke to Bloomberg News. A widely successful sale could give the banks involved an inside track on running an initial public offering by Aramco, should that ever happen.

Perhaps it’s little surprise then that details on the huge order book have been easy to come by. Saudi Arabian Energy Minister Khalid Al-Falih said in early U.S. hours on Monday that demand was higher than $30 billion. Six hours later, Bloomberg News reported it was about $40 billion. A few hours later, word came in that the deal received $60 billion in bids, surpassing the previous record held by Qatar.

I’m of the mind that a deal being “oversubscribed” is a fairly useless metric — it just means yields were too high to begin with — but I can see how strong demand could reassure investors that liquidity will be strong in the secondary market.

Put it together, and Aramco has all the ingredients for a blockbuster sale.

Aramco could still increase the size of the offering.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.