Saudi Arabia Is Set to Win Its Big Market Test

Saudi Arabia Is Set to Win Its Big Market Test

(Bloomberg Opinion) -- Saudi Arabia is back with another bumper bond issue, launching new 10-year and 31-year paper. It’s the first real test of investor demand since the murder of columnist Jamal Khashoggi in October, but a hefty premium on the yield will no doubt solve any residual qualms – in market terms, at least.

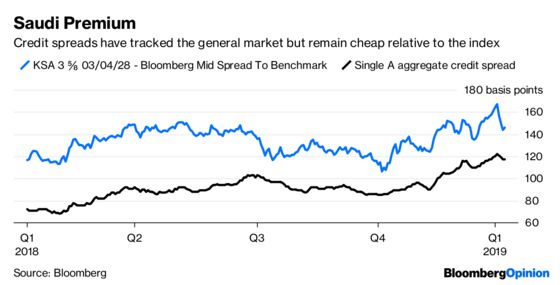

There’s also the benefit of early-mover advantage, with the sale coming in the first real business week of the year just as bond funds are itching to put new money to work. With credit spreads widening everywhere in recent months, effectively closing the new-issue window in the last weeks of 2018, most issuers will be cautious. (Saudi spreads have widened too, though not much more than has been the case at other sovereigns, despite the political furor). But a deal of this size – probably close to $10 billion in total – should overcome any investor hesitation and provide a solid start to the Gulf states’ 2019 debt sales.

Riyadh last came to the international bond markets in April 2018 when it issued seven-, 12- and 31-year maturities for a total of $11 billion, with no roadshow (as is the case this time too). It received orders of about $52 billion, illustrating the depth of demand. The kingdom has carefully established its capital market access with a succession of mammoth deals across maturities since October 2016, when it announced its presence to the debt markets with a $17.5 billion raise.

A spread of 200 basis points for the new 10-years over U.S. Treasuries, and 250 basis points for the new 31-year maturity, will certainly help; it’s a premium of 35-55 basis points over existing Saudi debt. The offered price might well be “walked in” before the bonds’ launch if demand is strong. But investors will see Saudi Arabia as one of the few early opportunities to buy high-quality A+ rated paper – with plenty of liquidity – from the primary market. As both deals will go straight into the major bond indexes, it will be hard for many funds to resist.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2019 Bloomberg L.P.