Safe Havens, U.S. Rates and Physical Demand: Gold Myths Busted

Safe Havens, U.S. Rates and Physical Demand: Gold Myths Busted

(Bloomberg) -- In a year when investors have been caught off guard by everything from emerging-market woes and the dollar’s tailwind to a brewing trade war, gold has been a conspicuous head-scratcher.

Why, investors ask, has the yellow metal tumbled as economic and geopolitical risks pile up?

Whether you blame it on ideology or the wretched complexity of global finance, the rules of thumb that govern gold investing are wide of the mark all-too-often. Busting five bullion myths right now could be key to understanding the current slide.

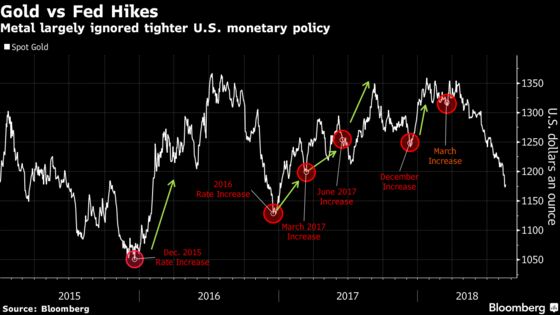

Myth 1: U.S. rates drive gold

The received wisdom is that when inflation-adjusted yields rise, assets bereft of income streams like gold tend to suffer given the opportunity cost.

But that’s not what is behind the current slump.

The argument hasn’t rung true for a while now, in fact. There’s very little correlation between the metal and 10-year inflation-linked Treasuries, coming in at -0.2 on a rolling 120-day basis. And just look at what happens when the Fed raises rates.

The key driver of gold, in fact, is the dollar. Few assets have a stronger inverse correlation to the Bloomberg Dollar Spot Index. The 120-day rolling measure stands at -0.6, indicating that the metal and currency typically moves in opposite direction. Other assets priced in dollars, particularly commodities, also have inverse correlations by construction -- but gold is by far the strongest.

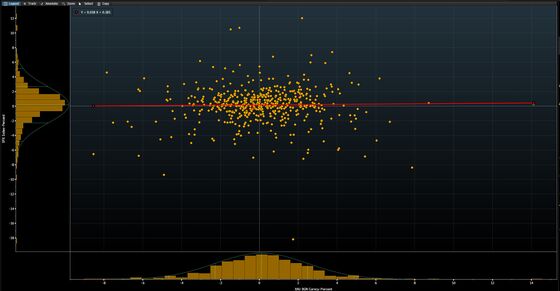

Myth 2: The precious metal is the anti-Dow

As an asset seen benefiting from haven demand, bullion goes up when stocks go down, right?

Not quite.

The shiny metal offers no such inverse correlation to equities -- the metal’s co-movement to the Dow and Nasdaq was less than 0.03 in the past decade.

Its allure is down to very fact there’s little relation between the two, because portfolio managers can lower the amount of risk they’re exposed to per expected unit of return through buying unrelated assets.

True to form, a regression plotting movements in the S&P 500 against that of gold looks like it was fired from a shotgun.

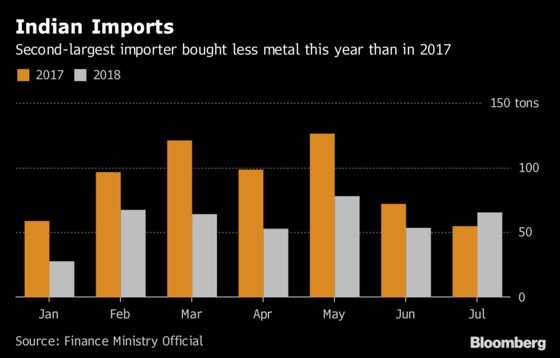

Myth 3: The physical market never matters

Another supposition: consumers of physical metal, such as jewelry and coin buyers, wield little power. After all, gold is a tradable asset overwhelmingly gripped by the ebbs and flows of global finance.

But while physical buyers aren’t key in fueling rallies, real-economy demand has historically proved a faithful floor when prices have fallen.

Gold’s woes this year, therefore, may come as little surprise given the diminished appetite of a key marginal buyer: India. The world’s second-biggest investor has held back, driving global demand down to its lowest in almost a decade in the first half of the year.

Myth 4: ETFs don’t move the needle

Gold exchange-traded funds can have an outsize influence on the broader market -- much more than commonly assumed.

ETF vaults hold the equivalent of roughly two-thirds of the fresh supply mined in 2017, for example. And those tracked by Bloomberg contain more than 2,100 tons, worth about $80 billion.

As a rule of thumb across markets, flows follow performance. That’s particularly true for precious metals, where passive allocations and bullion prices broadly move in the same direction. In every single tracked year where holdings went up, gold increased, and vice versa. The takeaway? Dismiss the underbelly of ETFs at your peril.

Myth 5: Central banks sell gold to avert financing crunches

Finally, there’s the vexed question of whether gold sales can come to the rescue for countries with external liquidity pressures.

For years, various episodes of financial turmoil across emerging markets, and even southern Europe, have spurred speculation there could be a looming fire-sale of gold held by monetary authorities. It rarely works out that way.

Big disposals risk spooking markets, and the divestiture mechanics are far from straight forward. For instance, Turkey is the 19th largest sovereign owner of gold. Yet, it’s unlikely to sell metal to ease balance-of-payments woes of late, in part because a chunk of holdings aren’t directly available for sale.

--With assistance from Sid Verma and Swansy Afonso.

To contact the reporter on this story: Eddie van der Walt in London at evanderwalt@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma

©2018 Bloomberg L.P.