S&P 500 Valuation Floor Is as Wobbly as 2019 Earnings Estimates

S&P 500 Valuation Floor Is as Wobbly as 2019 Earnings Estimates

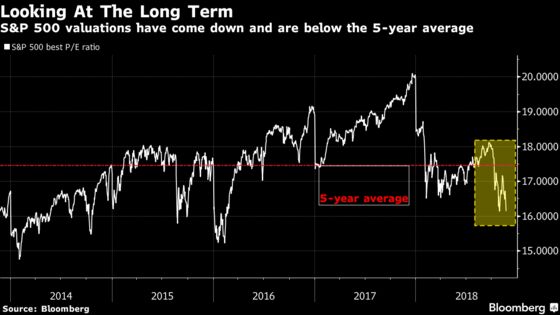

(Bloomberg) -- On paper, the S&P 500 is looking cheap. Its 10 percent tumble since September has pushed valuation versus expected profits to levels that compare well to almost any price-earnings ratio of the past five years.

For investors operating in the real world, however, the calculus is less soothing. Gusts of worry blow up around the phrase “expected profits,” with signs mounting that hopes have gotten too high. All the anxiety has ignited a plunge in equities that on Tuesday erased the S&P 500’s gain for the year and threatened to push it into a correction.

"Here’s the challenge: valuation is price divided by earnings, and analysts are notoriously too optimistic when it comes to earnings,” said Alec Young, managing director of global markets research at FTSE Russell. "People are saying all these negatives are priced in. But if macro negatives get worse, earnings get worse and the market is more expensive than it looks. ”

At the bottom of every bull case is the belief that buyers will step in when stocks are cheap enough to make their risk worth bearing. Knowing when that happens isn’t easy.

Mathematically, here’s where things stand. With the S&P 500 at 2,642 and consensus estimates for 2019 profits standing at $175.50 a share, the forward P/E is 15. That’s lower than almost any multiple since 2012.

Complicating matters is the squishiness of next year’s forecast, which for the first time in Donald Trump’s presidency are coming down. To simplify, the S&P 500 will only prove too cheap if earnings manage to jump somewhere around the 10 percent analysts predicting, to about $175.50 a share. Should they sit still at this year’s $159.50, the valuation floor looks decidedly less sturdy at 16.5 times profits.

Right now, the market seems to be leaning toward the “sit still’ scenario. Investors reckon something -- president Donald Trump’s trade war, the Federal Reserve, inflation -- will rise up and torch the economy before profits get a chance to post another year of growth.

“The market is saying, if not screaming, the turn in the economic cycle is imminent, if not already upon us,” said Rich Weiss, chief investment officer and senior portfolio manager of multi-asset strategies at American Century Investments. “When you see a rotation where tech stocks tumbled and utilities were flat or gaining -- that’s the market making a pretty big call on what’s about to come. This cycle is winding itself finally after nine years of recovery.”

Ominously, the market has often proven a better guide to future earnings than equity analysts. Take 2015, when the S&P 500 barely budged, posting the second-worst return of the bull market. In retrospect, it’s possible to read that performance as a verdict on 2016 earnings, which analysts said would be great. In fact, they fell.

For a lot of bulls, concern about next year’s forecasts is overblown and is just one of many delusions feeding the current frenzy to sell. Ten percent earnings growth may represent a big decline from this year’s rate of around 20 percent, but is also a fairly low bar going by recent history.

“Valuation is screaming at investors: ‘Stocks on sale,”’ said John Stoltzfus, chief investment strategist at Oppenheimer Asset Management. “If you look at three to five years, it’s likely going to be a small blip on the screen. We think the markets are going to digest this once the cooler heads prevail.”

At the same time, the changing tone on earnings calls has been a gut-check for anyone hoping the longest bull market on record gets longer. For all the robustness in third-quarter earnings, companies are notably dour on the future. Guidance is deteriorating, with firms that said sales will miss estimates outpacing those saying they will exceed them by the most since 2009, data compiled by Evercore ISI showed. The trend also worsened for profits.

Going by history, more downgrades may be on the way. Thanks to tax cuts, 2018 stands as an outlier, a year in which profits estimates have kept rising as it went on. That’s not what usually happens. Over the last 30 years, analysts have generally started way too optimistic and then cut annual forecasts as time went on -- by an average of 8 percent, data compiled by Goldman Sachs showed. Should 2019 track that pattern, EPS would erode to $161.50 -- not the $175.50 forecast now.

“At a little less than 15 right now, stocks look inexpensive, if you expect the bull market to continue,” said Chris Zaccarelli, chief investment officer at the Independent Advisor Alliance. “The market’s thinking that if we go into a recession, valuations would go much lower. I don’t see that happening. I think the market’s just discounting a lot of trade concerns, and concerns over what’s happening in Europe and global growth. The market is being cautious. Valuations are pretty compelling here."

To contact the reporters on this story: Vildana Hajric in New York at vhajric1@bloomberg.net;Elena Popina in New York at epopina@bloomberg.net;Lu Wang in New York at lwang8@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi

©2018 Bloomberg L.P.