S&P 500 Wipes Out $4 Trillion in Its Second-Worst May Since ‘60s

If euphoria was the concern, you can stop worrying.

(Bloomberg) -- If euphoria was the concern, you can stop worrying.

With books now closed, the S&P 500 has formally delivered its worst May return in seven years and second-worst since the 1960s, falling 6.6%. For tech traders watching the Nasdaq 100, the experience was only a shade less harrowing than the crash months of October and December.

“Clearly there’s potential for further downside,” Steve Chiavarone, a portfolio manager with Federated Investors, said in an interview at Bloomberg’s New York headquarters. “For markets to really rebound, I now need positive clarity on China, Mexico, politics in general and the Fed’s probably going to have to do something. That’s an awful lot to ask for.”

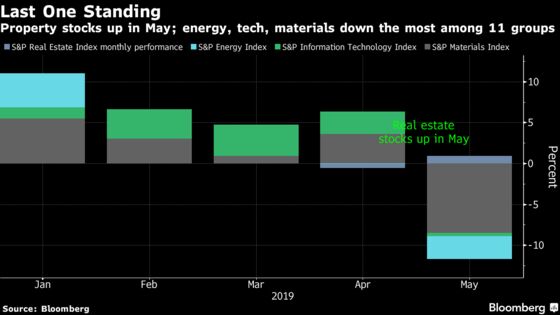

The list of May casualties is long. All but one of the 11 S&P 500 groups fell, with real-estate shares getting a boost as the 10-year Treasury yield plunged to a 20-month low. Chipmakers exposed to China got hammered, sending the Philadelphia Semiconductor Index down 17% for its worst month since the financial crisis. Technical support levels cracked as the S&P 500 sank through its 50-, 100- and 200-day moving averages for the first time in months.

Echoes of the mayhem from December abound, from erratic bets on volatility to the boom in hedging and the surge in defensive trading.

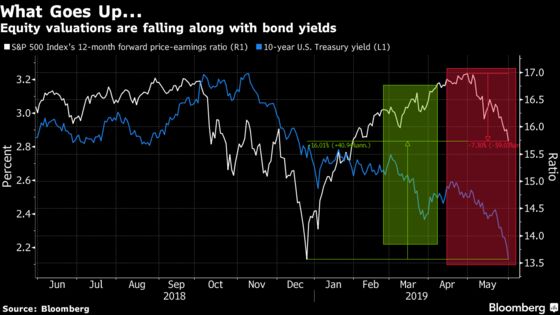

The Treasury market has delivered the most ominous signals in recent weeks. A 37 basis-point plunge in the 10-year yield took it below the level of three-month rates, inverting a key part of the yield curve by the most since 2007. While declining bond yields initially buoyed valuations in the first quarter, they’re now ostensibly reflecting deteriorating growth prospects that are bringing down equity multiples.

While lower valuations can boost the allure of equities relative to bonds, the prospect of a prolonged global trade conflict is an ever-present threat to corporate earnings and risk appetite.

“There needs to be a clear catalyst” for stocks to rebound, said Edmund Shing, global head of equity derivative strategy at BNP Paribas SA in London. “A U.S.-China trade deal could be one, but this is not our central scenario. The hardening of positions will be difficult to step back from, in the short term at least.”

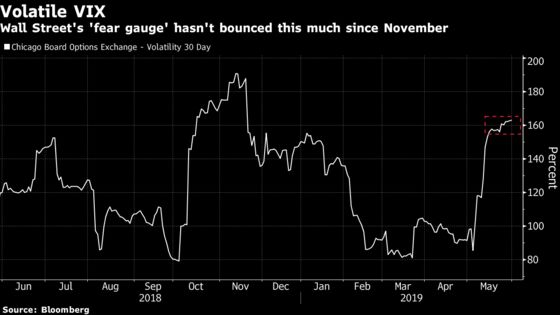

The uncertainty is reflected in the options market. While S&P 500 swings have remained relatively subdued this month, the VIX hasn’t bounced around this much since November. In fact, the Cboe Volatility Index spent time both above 21 and below 15 during two different weeks in May, something that’s never happened in the same month, according to data compiled by Twitter user OddStats and Bloomberg.

“A month ago the stock market was not only pricing in a trade deal with China, but the Iran issue wasn’t a problem, Brexit didn’t look that bad. Suddenly all of these issues are on a table,” Matt Maley, equity strategist at Miller Tabak & Co.

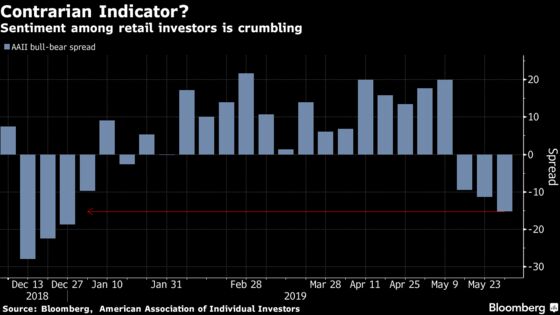

It’s not all doom and gloom, say the bulls. Crumbling sentiment, demand for safer companies and bonds that are sending terror alarms create the climate for contrarians.

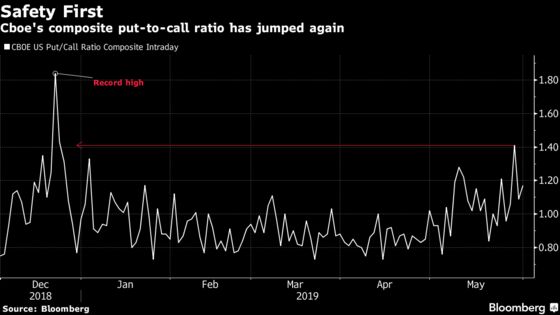

Cboe’s composite put-to-call ratio, which tracks outstanding options to sell stocks versus those to buy them, jumped to the highest since December’s record on Wednesday. Prior jumps “occurred near tradeable lows,” Jonathan Krinsky, technical analyst at Bay Crest Partners, wrote in a note.

Meanwhile, one U.S. metric of the relative bullishness of individual investors has plummeted -- a potential sign of a trough given the ensuing rebound when it notched similar levels late last year.

This “gives us some confidence that things in the short term aren’t necessarily going to deteriorate unless we see corporate earnings drop,” said Punit Patel, a fund manager at London and Capital Asset Management.

Arbuthnot Latham, a London-based private bank, has added Chinese domestic stocks recently as it sees pressures growing on both sides to reach an accord. A potential occasion for a detente: the Group of 20 summit in June, where Trump and Chinese President Xi Jinping are scheduled to meet.

“I believe that at the G20, Xi and Trump kiss and make up, and the equity market will love it,” said co-chief investment officer Gregory Perdon.

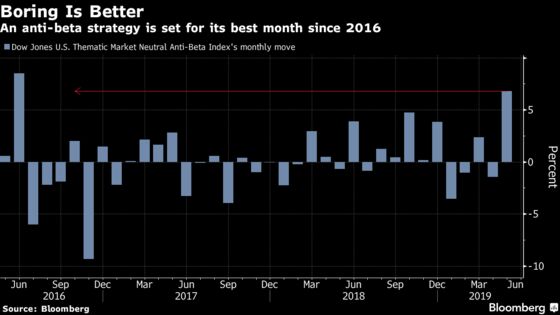

For now, safety plays are winning the day for any investor still in the market. A quantitative strategy that buys low-beta stocks -- those least sensitive to broad market moves -- and dumps high-beta ones capped its best month since 2016. Shares tied to economic growth and trade, in particular, have meanwhile become very difficult to price.

“The next couple of weeks will be volatile and choppy. The rally’s unfortunately going to be sold into,” said Donald Selkin, chief market strategist at Newbridge Securities Corp. “I don’t see any consistency on the upside because what is there to make it go up? Unless they announce a deal with China, but that seems very unlikely.”

--With assistance from Andrew Cinko, Yakob Peterseil and Elena Popina.

To contact the reporters on this story: Justina Lee in London at jlee1489@bloomberg.net;Vildana Hajric in New York at vhajric1@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Sid Verma, Jeremy Herron

©2019 Bloomberg L.P.