ADVERTISEMENT

S&P 500 Options Skew Shows Markets Still Calm on Tail Risks

S&P 500 Options Skew Shows Markets Still Calm on Tail Risks

20 Nov 2018, 11:40 PM IST

(Bloomberg) -- VIX is elevated, yet there’s no sign of extreme downside hedging panic on the S&P 500’s short-dated skew.

- One-month normalized volatility skew, the difference between 25-delta puts and calls normalized by 50-delta implied volatility, is not showing signs of panic

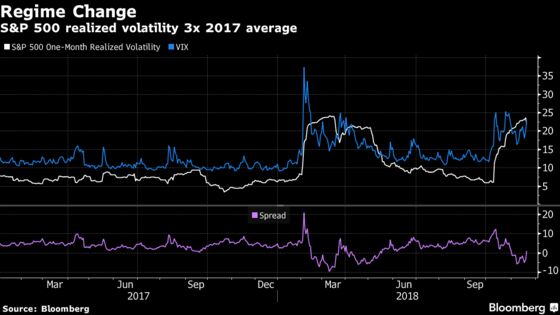

- SPX realized volatility remains historically elevated (10-day at the 80th-percentile of the 5-year range) as the index closes the gap between emerging-market and European equities

- Collar structures at increasingly higher strikes and funding of S&P 500 downside has provided a hedging strategy for those previously reluctant on spending premium against downturns given the low frequency of market sell-offs

- Even though inverse VIX ETP rebalancing on vol spikes needs only a fraction of the vega buying seen in the February blow-up, vol likely continues to settle in a higher range (VIX <20, the long-term average, >9, the short-vol bubble) given the need for increased vol insurance as quantitative tightening and growth concerns become the main drivers

- NOTE: Tanvir Sandhu is a global interest-rate and derivatives strategist who writes for Bloomberg. The observations he makes are his own and are not intended as investment advice

To contact the reporter on this story: Tanvir Sandhu in London at tsandhu17@bloomberg.net

To contact the editors responsible for this story: Ven Ram at vram1@bloomberg.net, Neil Chatterjee

©2018 Bloomberg L.P.