Run-it-Hot Eurozone Economy Robs Junk Bond Market of Real Yield

Run-it-Hot Eurozone Economy Robs Junk Bond Market of Real Yield

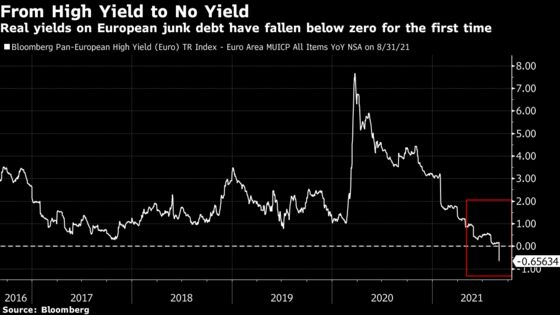

(Bloomberg) -- Europe’s economy is getting too hot for its credit market.

Inflation-adjusted yields on junk-rated debt have turned negative for the first time ever after euro-area consumer prices jumped to a decade-high in August, leaving fund managers to worry about not just the risk of default but also price growth.

Sub-zero yields have long been the scourge of European sovereign debt, sending investors into riskier realms to chase returns. As central banks flood markets with liquidity to rescue pandemic-shocked economies, sapping returns on most debt, European junk bonds are attracting more cash than ever.

Now, even as growth picks up and inflation surges, the European Central Bank guides no move higher in rates for some time, putting investors in a quandary of paying for the privilege of holding sub-investment grade debt.

Negative yields showed up in about a dozen companies with euro-denominated, junk-rated debt last month, but it’s suddenly become a problem for the broader market.

While that means investors lose cash if holding the debt to maturity in the event inflation persists, traders can make money should it keep rallying. That’s been the case for euro-zone junk bonds this year as corporate earnings rebound.

So far this year they’ve delivered the second-highest returns, of 4.4%, among 18 major bond markets tracked by Bloomberg, behind only their U.S. peers.

Meanwhile, policy makers are confident that the risk of European inflation is transitory, with August’s surge to 3% a short bounce as the region emerges from lockdowns. Bank of France Governor Francois Villeroy de Galhau said last week he sees no risk of overheating in Europe.

That view is also the accepted market consensus for now, keeping junk bonds in demand despite negative real yields.

“Most market participants think it will drop back to the old levels once the Covid stimulus is withdrawn,” said Konstantin Leidman, portfolio manager at Wellington Management International Ltd, which manages more than $1 billion in European high-yield assets. “Should it not be the case, this will be a problem for many financial markets.”

Europe

The region’s primary market kicked off with at least 9 issuers for the equivalent of about 5 billion euros ($6 billion) in issuance.

- Portugal’s EDP launched a 60.5-year hybrid green offering in two parts

- Spain is set to raise 5 billion euros from a debut green bond offering this week, according to two people familiar with the matter

- The leveraged loan and CLO markets are also seeing some activity, with issuers marketing deals

- Investors are looking at two term loan offerings, including a 1-billion euro deal from Dutch holiday park operator Roompot

- Among CLOs, U.S.-based investment manager Nassau Corporate Credit is in the early phase of marketing a 350-million euro debut CLO via Barclays

Asia

Concern that the liquidity crisis at China Evergrande Group will worsen is hammering China’s dollar junk bonds and potentially raising the cost of borrowing for real estate companies.

- Yields on the notes, which are dominated by property firms, rose to 12.9% on Friday, the highest since March 2020, a Bloomberg index shows

- Indiabulls Housing Finance Ltd., one of India’s largest mortgage lenders, is seeking to raise funds in the local public bond market after an absence of three years by the group.

- In the primary market, KWG Group Holdings is looking to price a tap of its dollar bond due 2025

U.S.

The investment-grade primary market is expected to spring back to life following the U.S. Labor Day holiday, as borrowers look to issue debt with low coupons.

- Syndicate desks expect $40 billion to $45 billion of fresh high-grade supply in the four days of trading

- Companies will continue the aggressive borrowing seen through most of 2021, helped by the low-rate environment and driven by the necessity of funding a growing pipeline of M&A activity

- For the month, $130 billion to $140 billion of supply is expected, according to an informal survey of debt underwriters

©2021 Bloomberg L.P.