Rob Arnott Says He Told You Tesla Would Be a Drag on the S&P 500

Rob Arnott Says He Told You Tesla Would Be a Drag on the S&P 500

(Bloomberg) -- Tesla Inc. has been a disappointment to many since going into the S&P 500 Index. But not to Rob Arnott.

Arnott, founder of Research Affiliates, would like the world to know he was right. He just published a study locating Tesla’s flop in what he considers the long history of bloated companies dragging down capitalization-weighted benchmarks.

Consistent with his claim that these benchmarks have a bad habit of buying high, Arnott’s data shows that in the first six months following a rebalance, index additions lag the stocks they effectively replaced by 14%, a gap that grows to 20% when measured a year out from the event. The addition of the electric-vehicle maker at the “near its highest-yet valuation levels is a striking confirmation of this pattern,” wrote Arnott with colleagues Vitali Kalesnik and Lillian Wu in a paper titled “Revisiting Tesla’s Addition to the S&P 500: What’s the Cost, Before and After?”

Certain quants, Arnott among them, late last year in the run-up to Tesla’s inclusion into the benchmark gauge raised the issue that megacap companies have the potential to harm passive returns. Arnott calls Tesla’s inclusion “the mother of all S&P 500 rebalances,” given its market cap at the time and the hype surrounding the company.

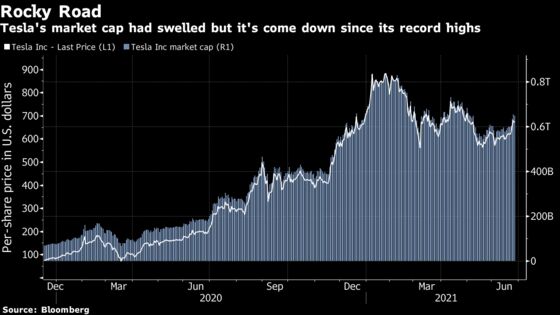

Shares of Tesla rose roughly eightfold in 2020, with much of the gains powered by investors anticipating that the carmaker would be added to the S&P 500. This year, they hit an intraday high of about $900 per share, but they’re down roughly 5% since the start of 2021 to trade around $670. The decline has wiped out about $21 billion in the firm’s value and is the biggest drag on the S&P 500 year-to-date.

“The big takeaway is that there’s this fairly reliable pattern with stocks that are added to the index providing market performance are a little worse on average and stocks that are dropped from the index providing markedly superior performance on average,” Arnott said by phone from Newport Beach, California.

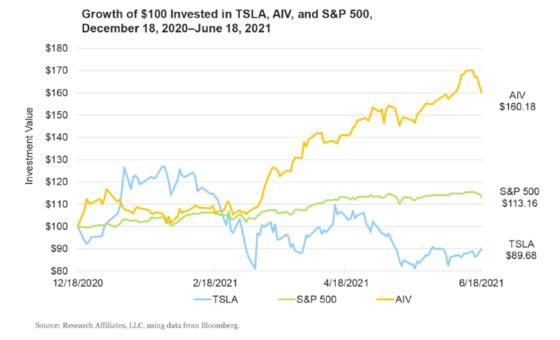

A $100 mid-December investment in Tesla, when the rebalance occurred, would have depreciated to $89.68 at the six-month mark. The same investment in Apartment Investment & Management Company, the company that got booted from the index, would have grown to $160.18. And an investor who chose to buy Apartment Investment on December 18 at the market close would, six months later, be enjoying a 78.6% relative return advantage over someone who bought Tesla -- an advantage that likely does not end here, according to Research Affiliates.

While Arnott’s focus on how returns vary among index members may seem obsessive, it reflects a decades-long debate in money management over how to construct passive benchmarks. A key tenet of Arnott’s smart-beta crowd is that traditional equity indexes have flaws, among them a propensity to embrace companies whose best days are behind them.

A common complaint is that index compilers often wait too long to make a change, long after a stock has taken off or languished. About two-thirds of stocks added to indexes had risen between the announcement date and the effective date, and only 43% had gained in the subsequent year following the rebalance. But around 50% of deletions had gained in the subsequent year following the switch, with the winners up by far more than the losers were down, Arnott’s research found.

“The way I like to describe it is the stocks that are added are companies that the S&P index committee is embarrassed that they haven’t added it already, and the stocks that are dropped are companies that the index committee is embarrassed that they’re still in the index,” Arnott said.

To be sure, Tesla might represent an “extreme outlier,” Arnott said. But a rebalance could be a great opportunity “to do the opposite of what the index does: buy the deletion and sell the addition.”

Arnott recalls being approached, following a presentation he gave at a conference, by the head of investments at an index company, who told him he’d been asked by his marketing department to stop buying additions or selling deletions ahead of the actual rebalancing. Arnott recalls the department telling the manager, “‘stop it! You’re adding value, you’re beating the index and we’re losing business because people say we’re sloppy because we don’t track the index perfectly,’” he recollected. But, “it’s a little bit of tilting at windmills because they probably won’t do it.”

©2021 Bloomberg L.P.