Risk Rally Spreads as Dovish Fed, Economic Data Beat Back Bears

Another week of gains as risk assets ride the late-cycle surge.

(Bloomberg) -- Of all the questions thrown up by the rebound in risk appetite so far this year, at least one is easy: What’s winning?

Pretty much everything, that’s what.

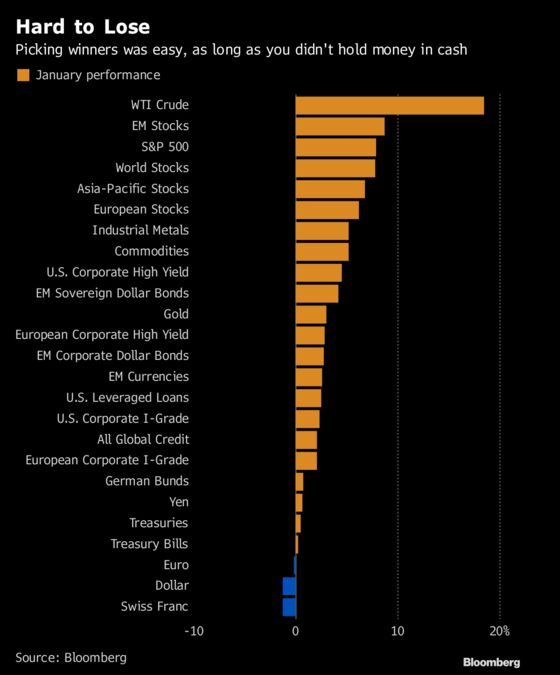

The end of the first trading month of the year brought a surge in superlatives -- the biggest January gain for a gauge of global equities in at least 30 years; the S&P 500 Index’s best month since 2015; the strongest start for U.S. high-yield debt in a decade; the largest first-month jump for commodities since 2003.

The tough question is how long all this can last.

At first blush, the past five days have delivered something close to a Goldilocks scenario for investors. The U.S. jobs number was solid, but wage growth cooled. A gauge of American manufacturing rebounded, but not too much. Most important, the Federal Reserve was more dovish than expected -- with member James Bullard reckoning the shift away from rate hikes sets the economy up for “a very good couple of years.”

Yet late-cycle signs are everywhere, and after December’s near-death experience market signals conflict at every turn. It’s a big problem for investors -- especially those who missed the January melt-up.

“It’s too late to be super bullish, and too early to be super bearish,” said Sophie Huynh, a cross-asset strategist at Societe Generale in London, who has been warning of a late-cycle economy. “Investors will have to pick up opportunities where they can -- in value, in the euro zone and in emerging markets.”

They’d better be quick. Emerging-markets stocks surged 8.7 percent in January. European equities jumped 6.2 percent. U.S. value shares climbed 7.6 percent.

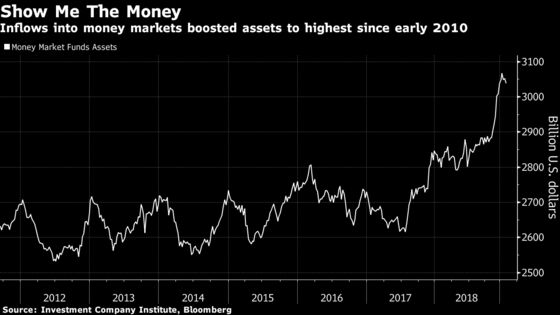

Plenty of people may have catching up to do. In the wake of the fourth-quarter rout, investors sought shelter in the money markets. Following six consecutive months of inflows through December, exchange-traded funds backed by short-dated securities hit the highest level since 2010 -- and it looks like plenty of capital is still there.

Unfortunately for them, cash was not a great place to be in January, and Bloomberg’s dollar spot index dropped 1.3 percent. Treasury bills were a laggard, only managing to eke out a 0.2 percent gain.

As for being quick, the so-called fast money has so far been anything but. Hedge funds pursuing long-short equity strategies came into January with bearish positions toward the S&P 500, judging by the portion of their returns attributable to the benchmark, a measure known as beta.

There are grounds for optimism, however. Positioning has since recovered to levels consistent with a 60:40 equity and bond allocation, Nikolaos Panigirtzoglou, a strategist at JPMorgan Chase & Co. said in a note on January 25. That suggests there could be more upside for U.S. stocks as hedge funds finally join the rally.

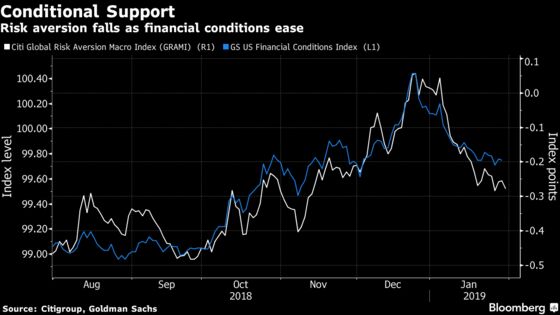

Just as the stock rebound from December’s lows appeared to run out of steam, Fed Chairman Jerome Powell this week scaled back tightening expectations even further than already anticipated. A dovish turn by the central bank in December helped ease financial conditions and has been key to the return of risk appetite -- after Powell spoke on Wednesday, the S&P 500 closed 1.6 percent higher. It added 1.6 percent in the week and closed Friday at the highest level since November.

Meanwhile, volatility gauges across currencies, stocks and bonds suggest a new period of tranquility may be emerging as option traders shake off December’s wild swings. The Cboe Volatility Index for stocks, known as the VIX, is back around its 200-day average. The MOVE Index, the equivalent gauge for Treasuries, this week hit the lowest since October.

Muted gyrations should help offset some of the lingering fears out there, such as concern about the trade war.

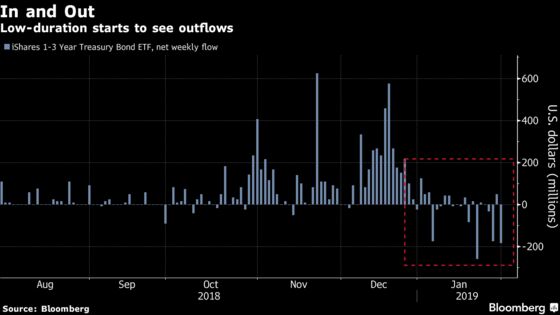

Even the dash for the safety of cash and short-dated government notes shows signs of ebbing. An iShares fund that invests in Treasuries with one- to three-year maturities saw $535 million pulled out in January, the first monthly outflow since July.

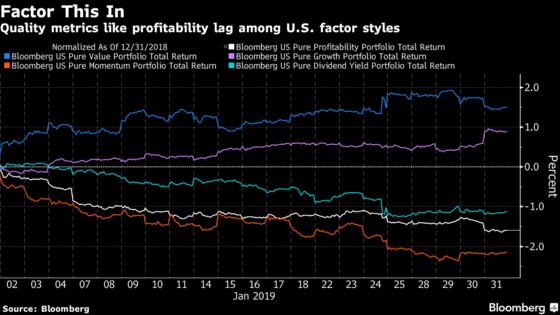

And remember how value shares performed? Quantitative investing styles following the strategy also gained, alongside those tracking growth stocks. More defensive factors, such as those based on profitability or dividend yields, have lagged.

But the value investing style’s outperformance of a factor like momentum also happens to be a typical late-cycle dynamic -- one of a slew of reasons for caution.

Even after earnings expectations were slashed, there have been disappointments from bellwether companies such as Caterpillar and Nvidia. The Fed message this week was more dovish than many expected, yet U.S. stocks showed a measured response overall -- a hint that the rally may need a different catalyst if it’s to continue.

A defensive picture was also on show in equity-focused ETFs, where quality and low volatility products attracted $4.6 billion between them in January.

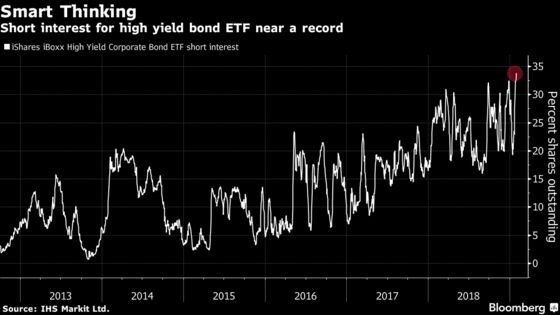

The incredible rebound in credit -- U.S. high-yield corporate bonds returned 4.5 percent in January -- comes with a caveat. Short-interest in the biggest high-yield bond ETF, is near a record. Clearly, the smart-money remains cautious that the rally in risk may be temporary in nature.

“Bear rallies are normal, the market trends remain negative,” said Charlie Morris, a fund manager at Atlantic House Ltd. which manages $1 billion in assets. He reckons those who didn’t get in on this bounce early have probably missed out.

After all, the Fed’s dovishness -- Powell signaled the U.S. central bank won’t raise interest rates again until inflation accelerates -- is another signal of the maturing cycle. And while it may open the door for the risk rally to continue, gains at last month’s pace are impossible to sustain. If they were, the MSCI All Country World Index would more than double this year and Brent would hit $400 a barrel.

For the laggards to catch up, they may need to be highly leveraged or jump down the credit and duration curves. That presents a conundrum, because those kinds of strategies are high-risk in a late-cycle environment.

“Most investors we talk to are still skeptical about this rebound because it’s been so quick and sudden,” said Roland Kaloyan, the head of European equity strategy at Societe Generale. “What’s changed is that there are no more rate hikes priced in. The market has relaxed. The market wants growth but without rate hikes, and that’s not possible for long.”

--With assistance from Lu Wang, Melissa Karsh, Sid Verma, Cecile Gutscher, Lujia Yu, Carolina Wilson and Ksenia Galouchko.

To contact the reporter on this story: Eddie van der Walt in London at evanderwalt@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Jeremy Herron

©2019 Bloomberg L.P.