Don’t Blame Risk Parity Quants for This Stock Sell-Off

Don’t Blame Risk-Parity Quants for the Stock Selloff

(Bloomberg) -- Turns out Wall Street’s favorite whipping boy isn’t to blame for the market sell off.

A meltdown in stocks in concert with a slump in bonds is seen as a noxious cocktail for the booming quantitative-investing strategy known as risk parity.

But any theories these leveraged players are fueling the global rout with forced divestments en masse are likely wide of the mark. Funds tracking the investing style are easily outperforming equity and fixed-income gauges.

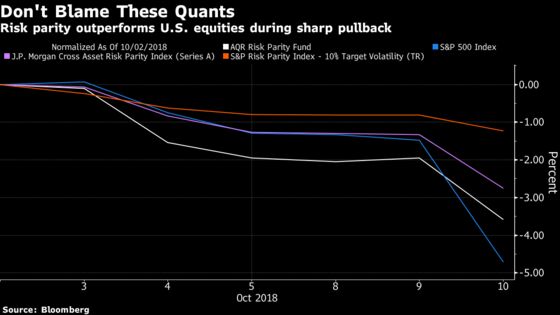

The S&P Risk Parity Index has lost a modest 1 percent over the past six days versus a 6.3 percent slump in the S&P 500. It’s also besting a benchmark exchange-traded fund tracking long-dated Treasuries and a classic 60/40 portfolio.

“Risk parity does not seem to be suffering anywhere as much volatility as it did in February, meaning that it won’t need to delever as much,” said Pravit Chintawongvanich, equity derivatives strategist at Wells Fargo Securities.

The investing style allocates across asset classes based on volatility, awarding larger weightings to more-subdued securities. Add leverage, and managers say the strategy ensures a smoother ride with higher long-term returns.

Yet, one feature emerges from this portfolio design that critics are all-too-often keen to point out: It has an outsized exposure to bonds relative to traditional portfolios, raising the prospect of forced divestitures during market disruptions.

So far in this week’s stress-test, however, the volatility-based allocation has insulated these funds from pain -- even as traditional two-decade correlations between stocks and bonds crater.

The S&P 500 Index fell more than 3 percent on Wednesday while the iShares 20+ Year Treasury Bond ETF also declined, an in-tandem slump registered only three times during bull-market cycles in the 16-year history of the product. The benchmark stock index was down as much as 2.7 percent Thursday.

This breed of quant has also benefited from lucky timing.

As bond and stock volatility awakened in recent months, most programs had already delevered heading into October’s maelstrom, according to modeling by Nomura Holdings Inc.

“Most funds probably took down-side hedged positions for their longs of gov bonds by selling futures in advance,” said Masanari Takada, a quantitative strategist at the Japanese bank. “Thus, loss could be limited this time.”

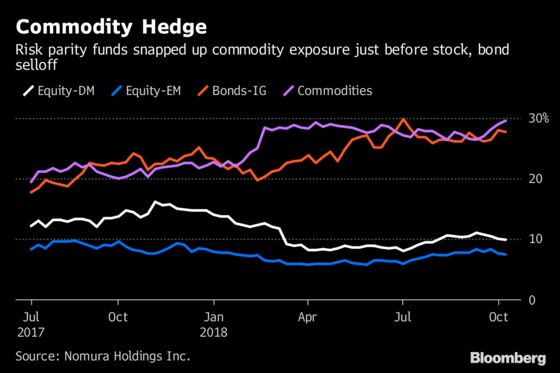

Risk-parity funds have also increased their commodity holdings over the past year -- a winning bet. With a 30 percent weighting as of Monday, commodities are the largest allocation among risk-parity managers, beating developed-market equities by 20 percentage points, Nomura data show.

And look what happens when a risk-parity strategy effectively eschews direct ownership of raw materials. The Wealthfront Risk Parity Fund, which typically gets exposure to the asset class through energy stocks rather than commodity futures, is down more than 6 percent over the past six sessions, lagging the S&P 500. Wealthfront’s fund also has a higher volatility target than some of its peers, which offers an alternative reason for the underperformance.

A spokesperson for the fund noted these differing volatility targets and said that judging a long-term strategy by narrow time frames can foster negative investor behaviors that ultimately harm performance.

A related cohort of quant perennially blamed for indiscriminate selling -- commodity trading advisers -- are also unlikely to have added insult to market injury. CTAs aren’t nearly as leveraged with their long-stock exposures compared with early 2018, according to Wells Fargo’s Chintawongvanich.

“The February 2018 ‘forced seller’ bogeymen are not as important now,” he concluded.

To contact the reporters on this story: Dani Burger in London at dburger7@bloomberg.net;Luke Kawa in New York at lkawa@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma, Jeremy Herron

©2018 Bloomberg L.P.