Risk Averse Poles Fleeing 0% Bank Accounts Just Can’t Win

Risk Averse Poles Fleeing 0% Bank Accounts Just Can’t Win

(Bloomberg) -- Near-record inflows into Polish mutual funds in recent months may be a boon for the country’s 291-billion-zloty ($74 billion) asset management industry, less so for its clients.

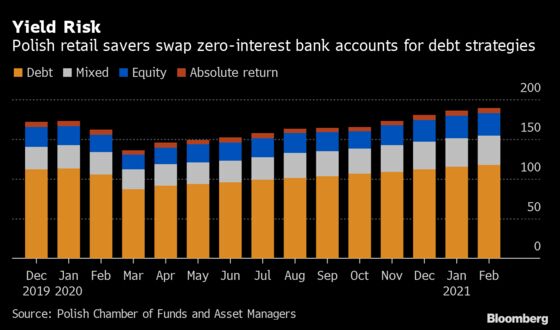

With bank deposits paying little to no interest, Polish savers have been piling into mutual funds at the fastest pace since the global financial crisis. Yet more than 80% of the money is ending up in debt funds, potentially exposing clients to significant losses at a time markets have started fearing higher inflation.

“Clients in Poland are generally quite conservative,” said Piotr Zochowski, chief executive of Poland’s largest manager of open-ended mutual funds, PKO TFI SA. “Judging by their age and wealth, they could be buying riskier products,” such as equities.

The picture looks similar across central and eastern Europe, where households generally prefer safety to outsize returns for their savings. In the Czech Republic, retail investors bought more stocks last year, but the asset class still represents a fraction of their overall savings. In Hungary, a large share of domestic savings has gone into five-year government bonds.

Polish debt funds have seen continuous inflows since March last year when the losses on foreign corporate bond holdings during the first wave of Covid-19 triggered massive redemptions. In the first two months of 2021 alone, assets in debt-focused funds rose by 5.9 billion zloty to 117.9 billion zloty, despite global turmoil in bonds in February.

Yields on Polish zloty bonds jumped to the highest level in almost a year amid investors’ concern that a spike in inflation will push the central bank to raise interest rates. Governor Adam Glapinski has repeatedly sought to quell speculation that a rate increase is imminent. Consumer-price increases accelerated to a six-month high of 3.2% in March.

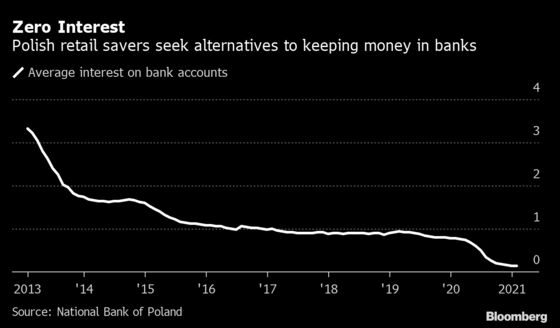

As the main interest rate in Poland was cut to 0.1% in the wake of the pandemic, most banks effectively stopped paying interest on short-term deposits, the most popular savings instrument in Poland. With inflation spiking, Poles started to look for alternatives to park their money.

Their first choice was often to buy mutual funds distributed by their own banks. In an automated risk assessment process, the mostly inexperienced savers were tagged as the safest group of so-called target markets, with debt and money market funds becoming a default choice for them.

“We certainly have to diversify the way Poles are saving money, so that clients aren’t exposed to risks of turning market trends just as they’re trying to escape low fees on deposits,” said Tomasz Kubiak, chief financial officer at Bank Pekao SA. “This is a process, we’re all learning the reality of ultra-low interest rates.”

The caution among Polish savers can’t be explained away by blind automation. The general experience of investing in local stocks has been anything but stellar, according to PKO TFI’s Zochowski.

“A bull market has pretty much lasted forever in the U.S., whereas in Poland we can only dream of the WIG20 reaching levels from before the global financial crisis.” PKO TFI’s Zochowski said, referring to Poland’s equities benchmark. “Even if a Polish fund has no investments domestically, clients would still perceive it via what’s happening on the Warsaw stock exchange.”

Temporary losses on bond funds aren’t a novelty for Polish investors and probably won’t trigger a U-turn in their approach, according to Rafal Boguslawski, director for strategy at Polish fund tracker Analizy Online.

“Yet if inflation continues to rise in the second half of the year, new investors in debt funds will be disappointed.”

©2021 Bloomberg L.P.