The Exchange Traded Product That Lost 99% Of Its Value Is Finally Dying

The Exchange Traded Product That Lost 99% Of Its Value Is Finally Dying

(Bloomberg) -- The most popular way to play volatility is going to its grave this week, but the impending death of an exchange-traded note sold by Barclays Plc is not the end of the story for futures traders.

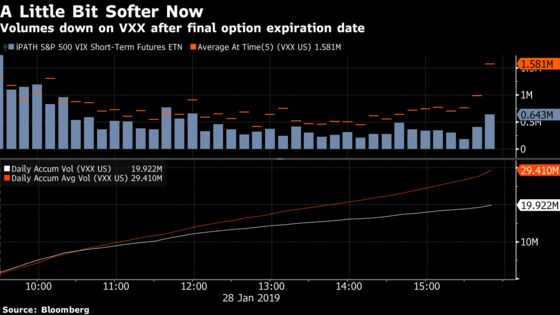

The iPath S&P 500 VIX Short-Term Futures ETN, ticker VXX, will mature as scheduled on Jan. 30, ending a favored means to bet on a gauge of expected gyrations in the S&P 500 Index. Anyone still owning the note at maturity will receive a cash payment based on its indicative value at the previous session’s close.

It’s a mixed legacy -- due to a structural quirk, the note lost 99 percent of its value over its life -- but it also democratized investor access to implied U.S. equity volatility. And there exists the potential, however slight at this point, for the wind-down to create one last wave in the futures market, if Barclays is forced to liquidate its hedge for the almost $500 million still invested in the note by 4 p.m. today.

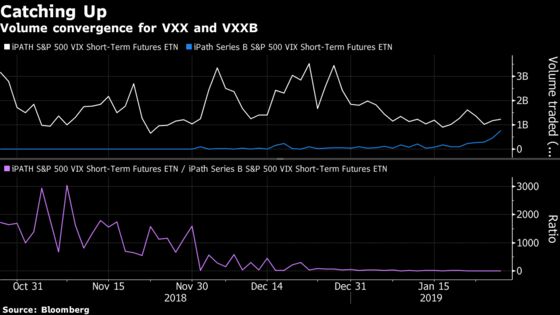

The bank is replacing VXX with VXXB, a note identical in almost everything but ticker and maturity date, but shifting assets and trading volume to the replacement has proved slow, and memories of exchange-traded products fueling market turmoil are still fresh, prompting caution.

“We’ll see, and keep an eye on the Tuesday close,’’ said Benn Eifert, chief investment officer at QVR Advisors. “It started slow, but looks to be an orderly transition -- everyone’s known about, and talked about, this for a while.’’

While VXX still has more shares outstanding than VXXB, the pace of the transition has accelerated. The most recent data shows assets have dropped to $488 million, as VXXB’s have climbed, down from $920 million one week ago and an average of $950 million throughout the fourth quarter. Likewise, the dollar volume traded in the two products has converged.

The eleventh-hour transition isn’t necessarily indicative of a large swath of holders having fallen asleep at the switch. The last expiration date for futures on VXX was Friday, and dealers or market makers who held the note to hedge themselves against an option they’d written would likely have looked to maintain that exposure through Friday.

But if some traders fear a lumpy exit today, they could look to sell VIX futures or options before the close to front-run the expected impact of a large sale, or enact spread strategies to bet on a pick-up in the implied volatility of implied volatility.

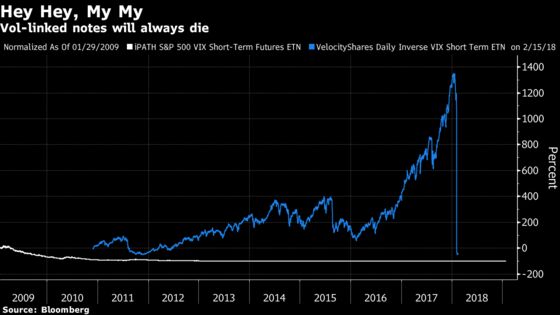

Giving some comfort, there’s far less at stake today than when XIV, a short volatility product, was forced to shutter last February, according to Vance Harwood, president of Six Figure Investing.

The dollar value of futures contracts that XIV, the now-defunct VelocityShares Daily Inverse VIX Short-Term ETN, was required to buy rose by billions in just a matter of 15 minutes during the chaotic session that felled the product, according to Harwood. By comparison, a couple hundred million dollars worth of VIX futures hangs in the balance with VXX’s well-telegraphed exit, he said.

“The odds of a disruption are very low, but you never know, and there might be some people who are going to speculate on that,’’ said Harwood. Pravit Chintawongvanich an equity derivatives strategist at Wells Fargo & Co., agrees, “I don’t think the long-only VXX base is very large, because most VXX exists to be shorted or in conjunction with options.”

Barclays is the largest owner of VXX, according to data compiled by Bloomberg. The firm lends out its shares to investors who want to bet against VXX, earning a fee in return.

VXX’s prospectus warns that the product is only suitable for “a very short investment horizon” -- and with good reason: The note will mature having lost more than 99 percent of its value.

That’s because the note’s rebalancing strategy involved consistently selling front-month contracts to purchase second-month contracts to be prepared for the contract’s roll. Generally, the VIX futures curve is upward-sloping –- in so-called contango –- because the outlook for U.S. stocks is generally more uncertain over longer periods of time, so the roll eats into returns.

For that reason, it was heavily shorted by traders -- a functionality that was slow to come to some brokerages for VXXB -- which also may have contributed to the glacial migration.

Ironically, XIV -- which blew up spectacularly -- ultimately vastly outperformed VXX over its lifetime, proving for some that Neil Young’s maxim still holds: It’s better to burn out than to fade away.

To contact the reporter on this story: Luke Kawa in New York at lkawa@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Rachel Evans, Dave Liedtka

©2019 Bloomberg L.P.