The Winners and Losers From Surging Iron Ore Prices

The Winners and Losers From Surging Iron Ore Prices

(Bloomberg) -- In the world of metals and mining, sometimes it’s better to sell the raw product rather than the finished one.

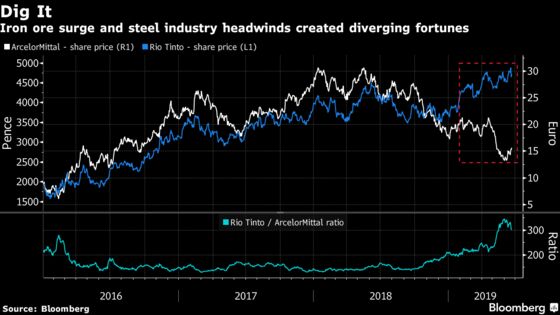

This seems to be a lesson for investors who chose to hold shares in ArcelorMittal rather than Rio Tinto Group this year. Despite nagging trade tensions and fears about global growth, Rio is up 30% in 2019, while the world’s biggest steelmaker has dropped 16%.

Global diversified miners have rewarded investors with record payouts and benefited from soaring iron-ore prices due to the supply concerns that followed Vale SA’s dam disaster in January. At the same time, Chinese mills have continued to set new production records, consuming more of the steelmaking ingredient.

Rio Tinto was carried by a “perfect storm,” said Arnaud du Plessis, a senior portfolio manager at CPR Asset Management in Paris, citing iron ore’s gains of about 75% in a year, the star performer among commodities. “Rio, which is highly exposed to iron ore and which benefits from very low production costs, has been the clear winner.” The London-based miner draws investors because of its strong balance sheet and high free cash flow generation, he said.

The gains might not be over. Jefferies analysts including Christopher LaFemina said in a June 12 note that Chinese iron-ore inventories continue to dwindle and should reach critically low levels in the second half of the year. Further economic stimulus from the Asian giant is also likely to support demand, with Rio Tinto among the main beneficiaries, they said.

Iron ore scaled new highs this week after Rio Tinto cut its production guidance, piling more pressure on supplies despite Vale’s authorization to restart a shuttered site.

Weak Autos

The forces that have made Rio Tinto a winner have partly been the cause of ArcelorMittal’s woes. The rising cost of its key raw material have pressured the steelmaker’s margins, while higher production in China and U.S. tariffs on imports have pushed European manufacturers into overcapacity, further weighing on prices.

Du Plessis noted that U.S. steel prices have fallen by more than 40% over the past year. “As a highly leveraged company, ArcelorMittal has not been in a good position at all,” he said. “As it’s highly exposed to the automotive market, the weak environment for that industry over the recent period has also affected ArcelorMittal.”

ArcelorMittal has responded by cutting production, while the industry is lobbying the European Commission for further safeguard measures to stop cheaper Chinese steel from flooding the market. Goldman Sachs analyst Eugene King this month upgraded European steelmakers, saying margins are showing signs of inflection, while a decline in iron ore prices could provide further relief.

A positive outcome in China-U.S. trade talks planned around the G-20 meeting in Japan at the end of June could be the ultimate catalyst steelmakers need to start outperforming again. Further dovishness from central banks could also support global growth, as well as a recovery in the carmaking industry, among the biggest consumers of steel materials.

“Trade war resolution will be key for the rest of the year,” said Du Plessis. The fund manager prefers Rio Tinto over ArcelorMittal as long as the crisis remains unresolved. Under a positive outcome, ArcelorMittal could outperform initially, with Rio Tinto lagging behind it, especially after its recent outperformance, he said.

ArcelorMittal’s current trading levels suggests it may be an attractive value proposition, offering 46% return potential over 12 months, according to the consensus of analysts tracked by Bloomberg. In contrast, the average analyst consensus sees Rio Tinto as fairly priced. The problem might be that at the moment, few investors are keen to bet on value.

To contact the reporter on this story: Michael Msika in London at mmsika4@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, John Viljoen, Jon Menon

©2019 Bloomberg L.P.