Revenge of the Doves: How the Fed Mainstream Joined Two Outliers

Powell, chairman since February 2018, has managed to avoid any dissents in his term so far.

.jpg?auto=format%2Ccompress&w=200)

(Bloomberg) -- The Federal Reserve is embracing the views of two occasionally ridiculed doves within its ranks who’ve argued for years that interest rates were heading the wrong way.

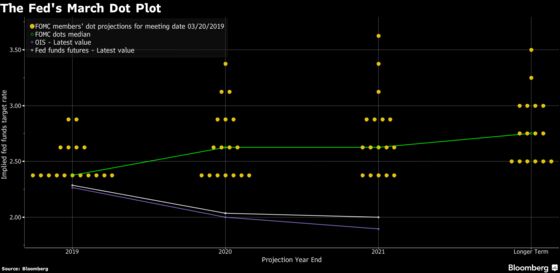

For a long time, St. Louis Fed President James Bullard and Minneapolis Fed chief Neel Kashkari were the lonely duo projecting no rate increase at the bottom of the Fed’s quarterly dot plot of policy forecasts. On Wednesday they had company, with 11 officials now penciling in no move this year.

The dots are anonymous but both officials had previously outed themselves by declaring a desire to keep rates on hold.

Bullard, 58, a Minnesota native who’s been president of the St. Louis Fed since 2008, has argued for two years that persistently lower growth has moved interest rates into a new low-inflation regime where higher rates are not needed. Kashkari, 45, president since 2016 and a former Treasury official under President George W. Bush, has maintained that sluggish wages reflect more slack in the labor market than widely understood.

“A lot of people made fun of those voices,’’ said Diane Swonk, chief economist at Grant Thornton in Chicago. “There is a competition within the Fed: If you are a Fed president, you want to outdo the board and its research, and they have. The Fed has benefited from a diversity of opinion and a willingness to give everyone a voice.’’

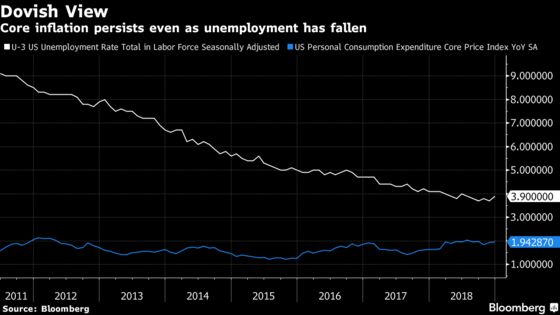

What separated the two from the rest of the Federal Open Market Committee was a contrarian view, now validated, that low unemployment alone would not lead to higher inflation.

While the two policy makers have been on the same page in terms of their prescription for rates, they have very different styles. Bullard is a Ph.D. economist who gives technical slide presentations that sometimes confuse regional audiences with arcane mathematical models.

Kashkari, who oversaw the U.S. government’s bank bailout during the financial crisis, began his professional life as an aerospace engineer. He speaks without notes in town-hall meetings in communities throughout his bank’s district, tackling questions on everything from monetary policy to affordable housing. He has also become a social media darling on Twitter, displaying baby pictures and talking up the intelligence of dogs relative to cats.

Fed Chairman Jerome Powell, while not citing either in his press conference after the meeting, echoed their views in his comments. Low inflation is “one of the major challenges of our time,’’ and there’s no easy explanation for it, Powell said, sounding like Bullard. The natural rate of unemployment may be “lower than people think’’ and “there’s still more slack in the economy,’’ he added, aligning with Kashkari.

Powell, chairman since February 2018, has managed to avoid any dissents in his term so far. The FOMC is composed of as many as seven governors who vote every meeting, plus 12 presidents of regional banks, with the New York Fed president voting each meeting and the others rotating their votes. Bullard votes this year. Kashkari, who dissented three times in 2017 against rate increase, votes next in 2020.

While Fed chairs usually lead policy, Ben Bernanke in 2006 sought to democratize decision-making and Fed presidents have become a source of ideas later adopted by the committee. Bullard’s 2010 paper called on the central bank to avert deflation, which was followed by a second round of bond buying. Chicago Fed President Charles Evans proposed tying policy to predetermined thresholds, adopted by the FOMC as the Evans Rule.

‘More Dovish’

Bullard outlined his low interest rate regime idea in June 2016 and has been arguing to go slow on rates since then. “I am one of the more dovish people on the committee and the committee has moved in a more dovish direction so things are looking up for me,” he said in St. Cloud, Minnesota, in February.

Kashkari has argued that a 3.8 percent unemployment rate, though near a 50-year low, gives a misleading picture of the labor market that is better described by wage gains. “Businesses love to say we’ve got shortages -- it’s this historic worker shortage. Well, show me the money,” Kashkari said last year, an often-repeated refrain of his.

Kashkari’s predecessor, Narayana Kocherlakota, said his own views were also “much-ridiculed’’ as outside the mainstream. “The Fed’s structure allows for ‘outsiders’ like myself, Bullard, and Kashkari to offer views that counter the group-think of the New York-DC nexus,’’ he said.

To contact the reporter on this story: Steve Matthews in Atlanta at smatthews@bloomberg.net

To contact the editors responsible for this story: Brendan Murray at brmurray@bloomberg.net, Alister Bull

©2019 Bloomberg L.P.