Revenge of Real Rates: 2018 Set for Worst Returns in Decade

Revenge of Real Rates: 2018 Poised for Worst Returns in a Decade

(Bloomberg) -- Even as U.S. stocks flirt with records, investors are staring at a cross-asset landscape that hasn’t been painted with this much red since the depths of the financial crisis.

The dollar’s upswing, brewing price pressures and cracks in the synchronized growth story have pushed asset returns into negative territory across much of the world.

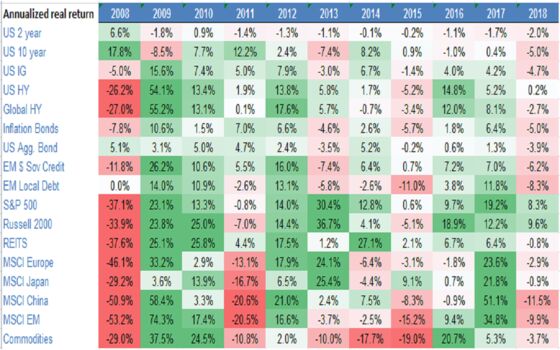

This year is on track to deliver the lowest share of positive returns adjusted for inflation across 17 major asset classes since 2008, according to Morgan Stanley.

Real yields are on the verge of breaking into a higher post-crisis range, threatening more damage to besieged portfolios.

Only the Russell 2000, S&P 500 and U.S. high-yield bonds -- some of the most expensive asset classes around -- have provided unhedged investors shelter from the storm in dollar terms.

“There always seems to be a level of griping, on both the buy- and sell-side, that conditions are challenging for one reason or another,” Morgan Stanley strategists led by Andrew Sheets wrote in a report on Sunday. “But this year it really seems to be the case.”

The Federal Reserve is poised to usher in a new era of real policy rates when it makes its forecast interest-rate increase this week -- turbo-charging the competition for capital and testing asset valuations anew. Longer-term inflation-protected Treasury yields hit their highest since 2011 on Tuesday. Real rates play a key role in discounting projected corporate earnings.

The investment landscape marks a volte-face from 2017’s Goldilocks regime, characterized by subdued inflation, a synchronized global upswing and a clamor for yield that pushed emerging-market assets higher.

Rising short-term rates adjusted for inflation are now allowing portfolio managers to satisfy their craving for yield lower down the risk spectrum, while increases at the long-end challenge equity valuations.

“We’re big believers that real rates matter most for risk markets, as it’s the rate over and above inflation that matters most for discounting future cash flows,” the bank’s strategists write. “As ‘invincible’ as the U.S. equity market has been, it hasn’t had to confront a different rate regime.”

Rate Ransom

Price action in recent weeks provides solace for bulls. The S&P 500 notched a fresh record while U.S. financial conditions have loosened from June levels -- even as 10-year real rates have climbed. Resilient risk appetites, a still-low effective cost of capital and stellar earnings have powered American assets across the board.

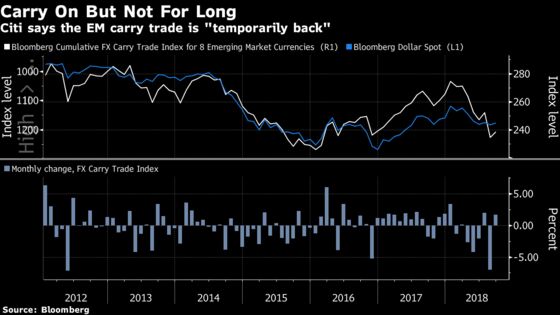

And the beaten-up emerging market complex has defied the rise in the discount rate, with bargain-chasing real money investors shifting back into debt products and bearish voices in retreat. A Bloomberg currency index that tracks developing-market returns from carry trades is up about 2 percent this month on the heels of its worst month in over six years.

But higher real yields -- in tandem with the repatriation of greenbacks, the outperformance of American equities and the U.S. economy’s strong momentum -- give Citigroup Inc. cause to question the longevity of the rebound.

“We are still reluctant to call the peak in EM sell-off as the major underlying medium-term factors behind the USD magnet may be still in place,” strategists led by Luis Costa wrote in a note. The carry trade is only “temporarily” back, he said.

A cruel new world may await cross-asset money managers.

GMO LLC, a value investor with $71 billion in assets, projects negative returns across most asset classes adjusted for inflation for the next seven years, with cash in dollars alongside emerging-market assets offering the only source of gains.

While U.S. stock investors are taking the rate sell-off in their stride, markets are humming a decidedly late-cycle tune, according to Morgan Stanley strategists.

“Rising real rates here are not an automatic negative, but do reflect that an age-old pattern is unfolding: Better growth --> Fed tightening --> higher real rates --> slower growth --> equities, challenged by a higher discount rate and the growth drag.”

To contact the reporters on this story: Sid Verma in London at sverma100@bloomberg.net;Luke Kawa in New York at lkawa@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Yakob Peterseil

©2018 Bloomberg L.P.