Resurgent Volatility Shows Why Distrust of Stocks Runs So High

Thought markets were hard to fathom back when the trade war was cooling and the Federal Reserve preparing to cut rates? Try now.

(Bloomberg) -- A stock market that has been scaring Wall Street for months got a lot more frightening this week as Jerome Powell and Donald Trump helped deliver the worst drop of the year and volatility surged.

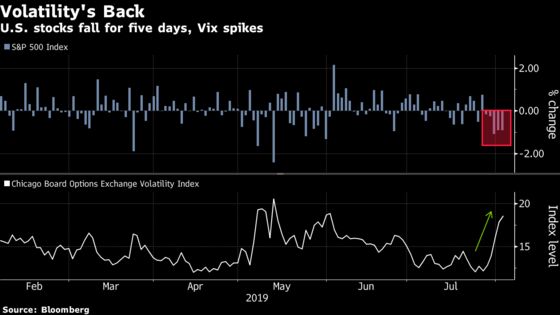

Thought markets were hard to fathom back when the trade war was cooling and the Federal Reserve preparing to cut rates? Try now, with Powell playing down his easing cycle and Trump slapping new tariffs on China. Solid jobs data couldn’t stem the slide. Stocks fell all five days while the VIX rose the most since 2018.

While investors can’t squawk too loudly with a 17% year intact, should things worsen, they’ll remember the twin blows from the Fed and Trump as defining the week when the safety net broke.

“That was one of the most manic 36 hours of trading I have ever witnessed in my 18-year career,” said Charlie McElligott, a cross-asset strategist at Nomura. “President Trump has again changed the market calculus. And thus investors, myself clearly included, are now forced to adjust their views on the monetary policy path.”

A week ago, bulls could at least fake answers when questioned about the rally. Earnings stagnating? Powell’s got our back. Economic growth in jeopardy? The trade war’s a bluff. And while neither thesis has suffered catastrophic damage, anyone hoping for an equity melt-up on the order of 2013, when the S&P 500 surged 30%, has been forced to adjust his spreadsheet.

“This has been a difficult week to navigate,” said Delores Rubin, a senior equity trader at Deutsche Bank Wealth Management. “As a trader, you can prepare for the FOMC and the potential reactions, but as has been the case for the past year, it is very difficult to navigate the tweets.”

The S&P 500 fell 3.1% in the five days after closing last week at an all-time high. The measure notched its first loss of at least 1% Wednesday and after a brief rebound Thursday suffered its biggest reversal of the year. The Cboe Volatility Index spiked above 19 in its biggest surge since March 2018.

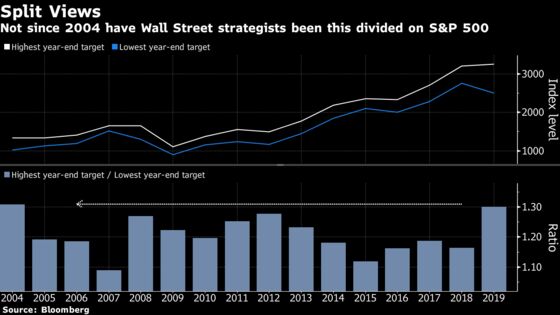

Confusion is everywhere. One way of measuring it is to plot the distance between the highest and lowest forecasts for the S&P 500 among strategists tracked by Bloomberg. Right now, the gap is the widest since 2004. Meanwhile, hedge funds and other discretionary buyers are avoiding stocks, while robots go all in. Earnings growth has ground to a halt while valuations are having one of their biggest expansions of the century.

“Investors are puzzled, no question about that,” said Gary Bradshaw, a portfolio manager at Hodges Capital Management. “Some are saying, ‘look, this market is long in the tooth, we’re in the eighth inning,’ and bulls say, ‘hey, we may be in the eighth inning, but we’re going to have a 14-inning ball game.”’

To be sure, if you’re looking to make either a bearish or bullish case, there’s ample evidence to back it. Manufacturing is weakening at the same time consumer confidence is running high. The jobless rate is stuck near a 50-year low. Second-quarter earnings have beaten estimates, but guidance is weakening. President Trump’s trade war has put global growth in danger, and yet central banks are still easing.

Not that people are supposed to agree, but it’s rare to see opinions as widely divided as now. From Binky Chadha at Deutsche Bank predicting the S&P 500 will end the year at 3,250 to Peter Cecchini of Cantor Fitzgerald seeing the index falling to 2,500, the 30% gap between Wall Street’s highest and lowest target is unusually wide.

The central bank’s pivot to monetary easing prompted David Kostin at Goldman Sachs to lift his year-end forecast for the S&P 500 even as corporate profits worsened faster than expected.

To Cecchini, the Fed’s rate cut is an acknowledgment that the economic slowdown will eventually morph into a recession. As hard as it’s been to stick to his bearish stance, he’s not wavering.

“It’s just one of those times when the forces bending markets in unnatural ways are too strong to fight. At some point markets will break, but the ‘when’ is notoriously difficult to predict,” he wrote in a recent note. “For those of us who have lived through more than one credit cycle, the bizarre feeling now is as extreme as any in memory.”

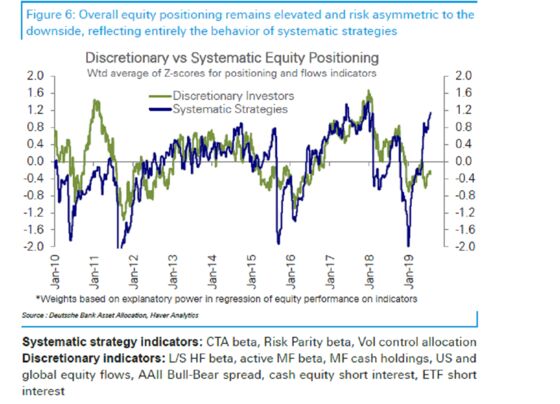

The split is also on display among investors. Individuals have kept pulling money out of equities this year and stock pickers from hedge funds and mutual funds are reluctant to embrace the rally. Meanwhile, traders who make bets based on momentum and volatility signals have boosted their exposure to some of the highest levels in a decade, data compiled by Deutsche Bank showed.

Despite this week, bulls remain in control. Rising in all but one month, the S&P 500 is on course for the best annual increase in six years. Almost all the gains have come from valuation expansions as the index’s forward price-earnings ratio jumped to 17.2 from 14.5 in January.

“Valuations are pretty stretched here. That alone will give you a significant divergence in opinions,” said Bruce Bittles, chief investment strategist at Robert W. Baird. “The Fed is cutting rates when the economy is doing pretty well. When is the last time that happened?”

To contact the reporters on this story: Lu Wang in New York at lwang8@bloomberg.net;Elena Popina in New York at epopina@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi

©2019 Bloomberg L.P.