Repo Market’s Liquidity Crisis Has Been a Decade in the Making

In normal times, not even Wall Street thinks too much about the arcana of short-term money markets.

(Bloomberg) -- It sounds crazy: even National Public Radio is talking about repo rates.

In normal times, not even Wall Street thinks too much about the arcana of short-term money markets.

But over the past week, the Federal Reserve has had to work unusually hard to rein in a key policy rate after overnight repo lending dried up. Suddenly, everyone is asking the same question: what does it mean?

The answer is sobering. Despite assurances by the Fed and others to the contrary, the stress in the market for repurchase agreements, or repos, has exposed some fundamental weaknesses in the nation’s financial system which have been a decade in the making. While they don’t pose a significant problem during good times, the risk is clear: without a permanent fix, sudden cash shortages could lead to broader financial market turmoil in a downturn.

“The machine of liquidity management is just not oiled anymore,” said GLMX Chief Executive Officer Glenn Havlicek, who runs a trading platform for repo securities and has four decades of experience in funding markets.

The repo market is important because it serves as the grease that keeps the global capital markets spinning. In a repo, firms borrow cash from each other by putting up securities like Treasuries as collateral. When the agreement expires, the borrower “repurchases” the collateral and returns the cash, though in practice repos are often rolled over day after day.

Hedge funds often use repos to finance purchases of higher-yielding assets, while dealers that are obligated to bid for Treasuries at U.S. debt auctions use them as a way to avoid putting up their own capital.

Participants point the finger at two structural changes that have drained too much cash from the system and made the repo market more prone to seizing up: crisis-era monetary policies and financial regulations designed to curb risk-taking. They contend that those two forces, rather than a mere confluence of technical factors, are what’s really behind this past week’s disruptions.

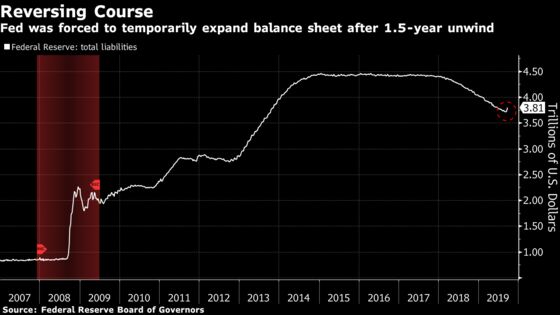

The first has to do with the unwinding of the Fed’s quantitative easing program, or QE. Simply put, after buying trillions of dollars of bonds to pump cheap money into the banking system, the Fed reversed course and started reducing its holdings (and thus draining cash) in October 2017 as the economy strengthened. It stopped altogether last month.

The problem is that, in reducing the asset side of its ledger, the Fed has also had to shrink its liabilities to balance its balance sheet. Those liabilities consist of currency in circulation, which has naturally increased with the economy, and bank reserves, which have fallen.

Of course, that in itself wouldn’t be enough to cause a scarcity of cash in the banking system since firms in aggregate still have over a trillion dollars in reserves. But because of post-crisis rules such as Dodd-Frank and Basel III, banks have been forced to set aside much of those same reserves to meet the more stringent requirements, putting a strain on the available cash they can use. What’s more, capital constraints have made taking large positions in short-term money markets far less lucrative.

“The Fed wanted the market to restructure to a new equilibrium and institutions to figure out how to fund themselves,” said Julia Coronado, president of Macropolicy Perspectives. But “if you have an excess reserve system, you are by definition a primary source of liquidity. And when you squeeze funding markets, you are usually squeezing hedge funds and other investors that may have to cut positions which can spark broader volatility.”

JPMorgan CEO Jamie Dimon summed up the conundrum last week, saying that “banks have a tremendous amount of liquidity, but also have a tremendous amount of restraints on how they use that liquidity.”

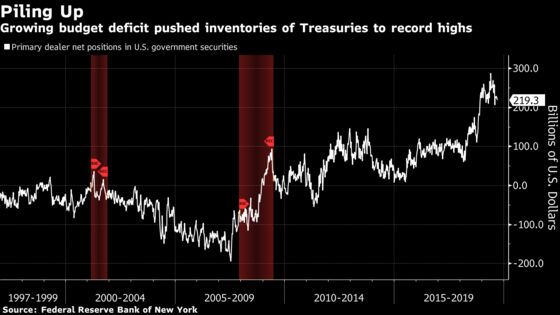

The swelling U.S. deficit caused by President Donald Trump’s tax cuts hasn’t helped matters. For one, the money that investors and dealers lend to the government in the form of bond purchases takes money out of the banking system. For another, dealers at Treasury auctions have increasingly turned from lenders to borrowers in the repo market to absorb the additional supply. This year, net issuance will reach roughly $1.2 trillion, after $1.3 trillion last year, according to JPMorgan. In 2017, it was less than half that.

Those liquidity constraints came into full view over the past few days when corporate tax payments, big Treasury auctions and maneuvers by financial firms to manage their capital requirements prior to quarter-end drained cash available for repo transactions. The overnight lending rate quickly shot up to 10% and the Fed temporarily lost control of its benchmark rate.

In the past, the Fed has disputed the idea that its balance-sheet unwind left bank reserves in short supply. And at his post-policy news conference on Sept. 18, Fed Chairman Jerome Powell sidestepped questions about whether he felt bank regulations were a catalyst for the market turmoil.

Instead, the Fed has opted for a temporary fix. On Friday, the New York Fed announced a series of overnight and term operations over the next three weeks to boost short-term liquidity. That follows four straight days of repo transactions, something it hasn’t done in a decade.

A number of investors, strategists and at least one former Fed official have come out to warn that more may need to be done.

“Maybe we have gotten some hints that reserves are no longer ample,” said Michael Feroli, JPMorgan’s chief economist. “The longer the Fed goes without making changes, the more often you might have these type of incidences.”

Earlier this year, TD Securities’ Priya Misra predicted the Fed would have to resume its bond purchases as a permanent solution. She says this past week’s events have convinced many of her skeptical clients to come around to the idea. They are now asking her “how much” the Fed will need to buy.

While no decisions have been made, Boston Fed President Eric Rosengren acknowledged last week that permanently expanding the Fed’s balance sheet is one option on the table and the one he personally prefers. (The other two being continued ad-hoc interventions or a so-called standing repo facility, which would make cash loans available on a daily basis.)

Growing the balance sheet might also be the easier one, some strategists say. Pumping cheap cash into the financial system has historically come with the risk of spurring too much inflationary pressure, but after a decade of ultra-low inflation, that isn’t much of a concern today.

And the fact the New York Fed stumbled out of the gate as it tried to come to the rescue on Tuesday shows just how out of practice the institution is when it comes to those types of ad-hoc operations, according to GLMX’s Havlicek.

“The repo market isn’t used to being prime time,” in terms of liquidity management, he said. And, the Fed is “out of practice.”

To contact the reporters on this story: Liz Capo McCormick in New York at emccormick7@bloomberg.net;Matthew Boesler in New York at mboesler1@bloomberg.net;Craig Torres in Washington at ctorres3@bloomberg.net

To contact the editors responsible for this story: David Gillen at dgillen3@bloomberg.net, Michael Tsang, Mark Tannenbaum

©2019 Bloomberg L.P.