Repo Firepower Reduced by Falling Cash Levels at Big U.S. Banks

Repo Firepower Reduced by Falling Cash Levels at Big U.S. Banks

(Bloomberg) -- Even as hedge funds and smaller broker-dealers lean more heavily on the biggest U.S. banks for borrowing in repo markets, the lenders’ cash holdings have been declining, reducing their ability to jump in and relieve pressure when rates spike.

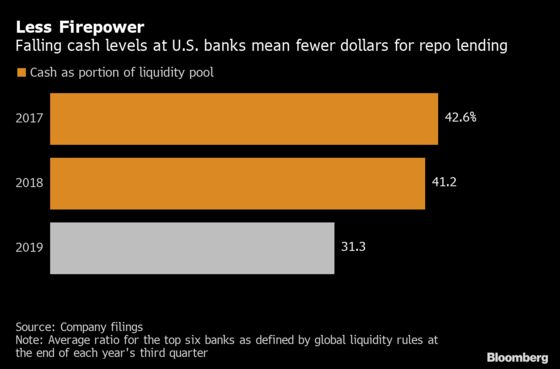

The average portion of liquid assets held as cash by the six biggest lenders fell to 31% by the end of September, down from more than 40% in the previous two years. The portion of Treasuries and other securities considered easy to sell under international regulations, meanwhile, rose.

The top U.S. banks have become “marginal lenders” in the repo market as money-market funds have retreated somewhat in recent years, according to an analysis from the Bank for International Settlements, released Sunday. When demand temporarily surged in September and repo rates spiked as a result, those firms were slow to jump in, constrained by new rules, stronger risk-management controls and a shortage of traders with expertise.

The Federal Reserve’s efforts to calm the repo market after September’s troubles may prove too minimal to prevent a repetition at the end of December, when large European banks shrink repo lending to minimize capital charges calculated annually. The Fed, which was shrinking its balance sheet until midyear, reversed direction in October to provide more cash to the system.

“The reduction of reserves in favor of Treasuries has been more pronounced at some of the biggest banks -- more so than what the Fed’s balance-sheet reduction would require,” said Darrell Duffie, a Stanford University finance professor who’s researched the repo market. “That was possibly to benefit from declining bond yields, which has happened. But it also reduces the amount of cash reserves available when others come calling.”

JPMorgan, Citi

The most pronounced shift to Treasuries and other securities happened at JPMorgan Chase & Co., where cash holdings dropped to 37% of high-quality liquid assets at the end of September, from 64% a year earlier. Citigroup Inc. was the only company among the six biggest U.S. banks to increase its cash holdings -- to 37%, up from 33%.

The biggest banks have traditionally served as intermediaries between money-market funds and hedge funds. Before the 2008 crisis, they were net borrowers in the market, meaning that, in addition to the cash they were supplying to other repo borrowers, they also were borrowing for their own financing needs.

Post-crisis, the banks have become net lenders, supplying borrowers some of their own cash in addition to what they intermediate from other suppliers. Since the middle of 2018, other large U.S. banks also have cut their repo borrowing, turning the banking sector into a net lender this year, the BIS said.

Post-crisis regulation tamed the repo market. The biggest banks are now less reliant on it for financing, and its use for funding esoteric securities has been nearly eliminated. Yet new rules, and the accompanying focus on risk management, also make it harder for the biggest banks to jump in when the market needs them most.

Rules, Tests

Liquidity rules, stress tests and living wills all restrict the amount of cash that banks can deploy quickly. Stricter risk-management rules prevent them from helping those in desperate need of cash, bank executives and regulators have said in private conversations.

“Banks have become more cautious, thinking twice before moving when there’s a sudden change in any market,” said Greg Hertrich, head of U.S. bank strategies at Nomura Securities International Co. “Regulators have urged them since the crisis to act that way. That’s probably a net positive for the financial system.”

Post-crisis rules punishing lenders for their reliance on repo funding and balance-sheet size also have reduced the biggest banks’ overall footprint. Their market share in one of the main repo markets dropped to as low as 22% at the end of last year, from 50% before 2012, according to New York Fed data. But the smaller dealers who have filled the void are only intermediaries without their own source of funding when money markets or other cash suppliers pull back.

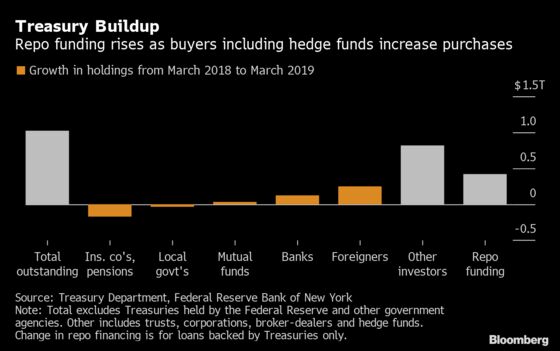

Hedge funds betting on the Treasury market have increased their demand for repo funding in recent quarters, the BIS said, without detailing the reasons for the rise. Data on Treasury ownership and repo volumes hint that hedge funds might be the biggest buyers of U.S. government bonds in recent quarters as typical cash investors, such as sovereign wealth funds, have slowed their purchases.

As U.S. government debt rose by $1 trillion in the 12 months through March, more than 80% of it was absorbed by “other investors,” a category in the U.S. Treasury Department’s database that includes broker-dealers and hedge funds. Repo funding rose by at least $400 billion in the same period, New York Fed data show, a sign that the debt increase was taken up mostly by leveraged investors like hedge funds.

That reliance on short-term funding is likely to hurt Treasury yields at year-end, when foreign banks reduce their exposure and U.S. peers don’t have the ability to step in and fill the void, said Zoltan Pozsar, a Credit Suisse Group AG analyst.

“The safe asset –- U.S. Treasuries –- is being funded overnight, and therefore it depends on balance sheet to be held,” Pozsar said in a note to investors Monday. “Balance sheet for the safe asset isn’t guaranteed around year-end, and if balance sheet won’t be there, the safe asset will go on sale. Treasury yields will spike.”

To contact the reporter on this story: Yalman Onaran in New York at yonaran@bloomberg.net

To contact the editors responsible for this story: Michael J. Moore at mmoore55@bloomberg.net, Daniel Taub, Dan Reichl

©2019 Bloomberg L.P.