Red Flags in Corporate Debt Markets Are Worrying Some Bond Kings

Red Flags in Corporate Debt Markets Are Worrying Some Bond Kings

(Bloomberg) -- Some of the biggest buyers of corporate debt are getting antsy.

Executives at Pacific Investment Management Co. and MetLife Inc. are sounding alarms about companies’ ballooning debt loads after more than a decade of cheap money and deteriorating lending standards. As the U.S.-China trade wars heat up, top money managers at Pimco called the market “probably the riskiest ever” and “the area of most concern for us” in interviews with Bloomberg.

The money managers aren’t calling a turn in the market just yet, and they acknowledge it could get even frothier. Investment-grade company bonds have gained 6.6% this year through May 29, their best performance since 2003. U.S. corporate debt offers the highest coupons in a world where there’s more than $11 trillion of negative-yielding securities, the highest level since 2016. That’s spurring investors to buy U.S. securities on increasingly risky terms.

That near term market support could make it a good time for money managers to cut risk, Pimco said. Some investors may be doing so: investment-grade funds in the week ended May 29 had their biggest weekly withdrawal since December 2015, according to Lipper. Pimco is favoring higher- quality bonds, and prefers asset-backed securities to corporate credit, said Scott Mather, chief investment officer of U.S. core strategies. Here are some of the biggest red flags the fund manager sees in the market:

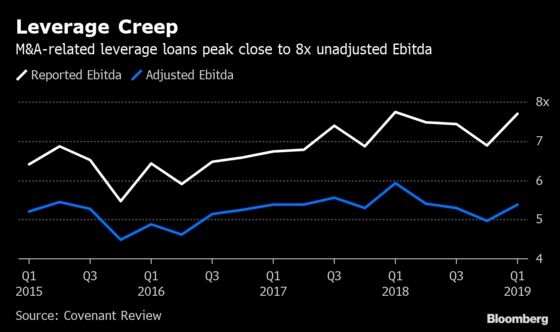

Leverage

Corporate credit quality, as measured by company debt levels relative to earnings, has been deteriorating as companies add cheap debt. On average, leverage levels at high-yield companies seeking loans to fund mergers and acquisition are close to 8 times a measure of unadjusted earnings, according to Covenant Review, well above the 6 times levels regulators had pushed for. The trend has caught the attention of regulators. Federal Reserve Governor Lael Brainard called out “a notable deterioration in underwriting standards” for leveraged loans in December, noting that corporations with the riskiest balance sheets “have been increasing their debt loads the most.” MetLife Chief Investment Officer Steve Goulart said last month his firm is avoiding debt from companies that are active acquirers.

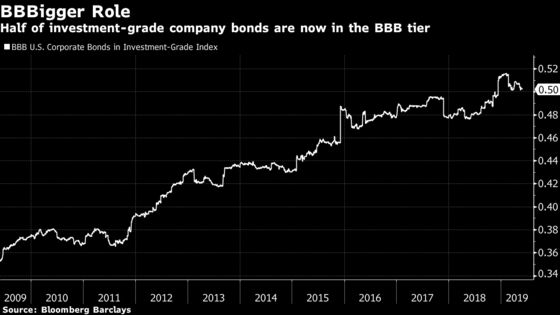

Market Size

The amount of high-grade U.S. company bonds outstanding has more than doubled to $5.44 trillion, from $2.2 trillion in 2009. More concerning to many investors is the growth of BBB rated bonds, which sit in the lowest tier of investment-grade debt and now account for around half of that market. Companies that let their credit ratings slide and took on billions of debt to fund acquisitions may be weaker than their ratings suggest and could struggle with their debt loads if earnings falter. The junk-rated market has expanded too -- it’s now about $1.2 trillion, compared with less than $600 billion a decade ago. The market value for leveraged loans exceeds $1.2 trillion, also representing big growth.

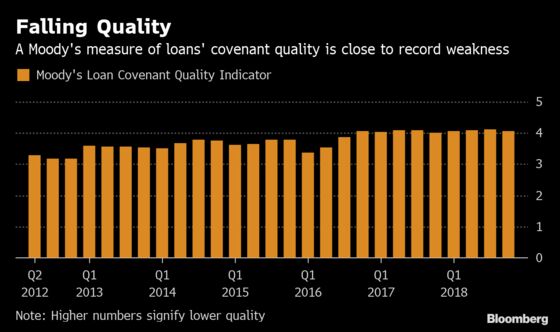

Loan Quality

Key protections for loan investors -- namely the covenants and terms that allow them to seize assets and take other steps when companies falter -- keep getting weaker. Moody’s Investors Service said covenant quality for 2018’s last quarter was close to a record low, and it sees no signs of improvement this year. One big concern is that borrowers can now easily move more collateral out of the reach of lenders. That will translate to bigger losses in a downturn, strategists say. UBS Group AG estimates investors may end up recovering somewhere around 40 cents on the dollar on bad leveraged loans, possibly less than half what their usual recoveries are in recessions, in part because of the deterioration in protections.

Liquidity

Investors have long griped that regulatory changes after the financial crisis have crimped corporate bond liquidity. Dealers keep fewer bonds on their balance sheets now compared to pre-crisis and the Financial Industry Regulatory Authority is considering testing a disclosure delay on block trades that large asset managers say could help boost liquidity.

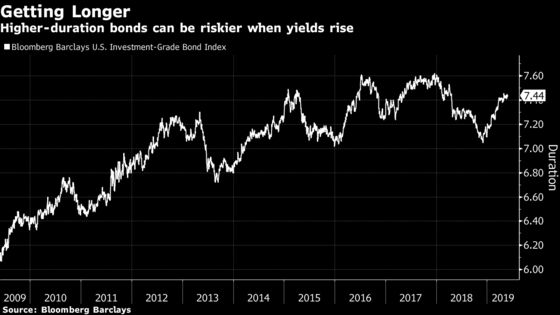

Duration

As companies have piled on more debt, they’ve taken advantage of lower interest rates to issue longer-dated securities. While long-duration debt is popular with investors like pension funds and insurers that seek to match long-term liabilities with assets, adding duration can also add risk. For one, investors are staking their bets on the health of a company for a much longer time horizon. And long-dated company bonds are more sensitive to changes in interest rates, meaning they can take a beating as rates rise, even if a company’s prospects look healthy.

--With assistance from Lisa Lee.

To contact the reporters on this story: Claire Boston in New York at cboston6@bloomberg.net;Sally Bakewell in New York at sbakewell1@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, Dan Wilchins

©2019 Bloomberg L.P.