Biggest Correlation Spike on Record Means More Bad News for Quants

Biggest Correlation Spike on Record Means More Bad News for Quants

(Bloomberg) -- Call it the curious case of correlation? Co-movements between factors, or investments based on a particular style such as growth or momentum, have reached the highest level in at least two decades, according to research from Sanford C Bernstein Ltd.

The move is unusual and poses an additional headache for quantitative funds after a difficult year, according to Bernstein’s Head of Global Quantitative and European Equity Strategy Inigo Fraser-Jenkins, who once suggested that passive investing was worse for society than Marxism. While correlations typically tick higher during big selloffs, he said, individual stocks haven’t been moving in lockstep as much as factor groupings in recent weeks.

“This is the first time that we have seen this,” the analysts wrote. “This implies there has been a significant change in the structure of the market.”

Quant strategists have spent years telling investors they could beat benchmarks by slicing and dicing the market into buckets like ‘value’ or ‘quality’ stocks, each offering distinct behavior in different market conditions. If, as Bernstein writes, such factors are increasingly moving in tandem, investors may face unwanted risks and quants might struggle to generate idiosyncratic returns.

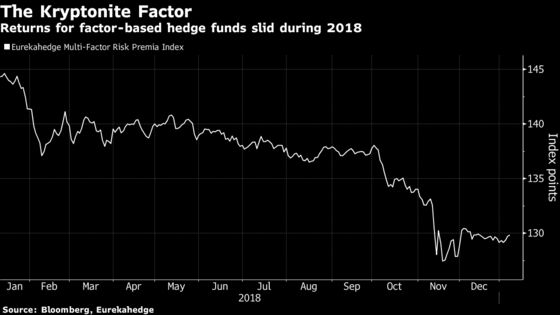

The research may be the latest example of historical models misfiring for such funds after a year which saw dismal returns for risk premia portfolios and prompted job cuts at industry giant AQR Capital Management. The Eurekahedge Multi-Factor Risk Premia Index declined 10 percent during 2018, its second annual loss in eight years.

While weakening macroeconomic data is most likely the immediate cause of the increase in factor correlations, the widening gap in valuations between the cheapest and most expensive stocks has also played a role, according to Bernstein.

“What makes this different is that stock correlation is not so elevated,” the strategists wrote. “Stocks are moving depending on which factor bucket they are in.”

While some of the increase in correlation reflects the growth in exchange-traded funds tracking factors, the limited scale of these flows means that they are “unlikely to be a driving force,” they added.

To contact the reporter on this story: Gregor Stuart Hunter in Hong Kong at ghunter21@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Cormac Mullen, Ravil Shirodkar

©2019 Bloomberg L.P.