Real Money Hasn’t Jumped on the Bandwagon Yet: Taking Stock

Real Money Hasn’t Jumped on the Bandwagon Yet: Taking Stock

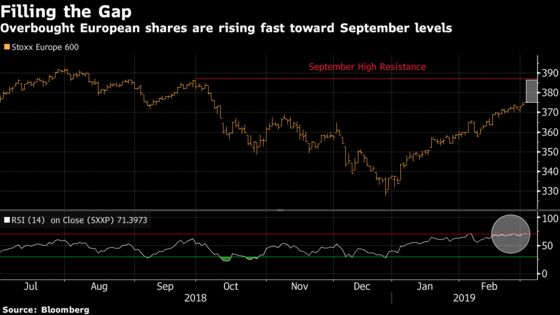

(Bloomberg) -- After an equity rally that’s lasted two full months, are we done for the year? There were rising voices warning that levels look stretched -- at least in the near term -- and that was even before China cut its growth target. The Stoxx Europe 600 has posted an 11 percent gain in 2019 and has been trading in overbought territory for a few days now.

Goldman Sachs strategists still have a positive view on equities this year, although they adopted a neutral stance over a three-month horizon in their latest asset allocation note. The fact is that this market rebound came after a year of extreme bearishness and record outflows, and it may need more than a China-U.S. trade deal to keep going.

European shares have seen a consistent net exodus since March 2018, and the real money keeps selling on the market gains, according to the latest flow data. It remains to be seen if a more dovish Fed and an impending trade-deal will be enough to lure asset managers back.

The current rally has gone “too far, too fast,” according to Fabrizio Quirighetti, chief investment officer of Syz Asset Management, who has a neutral stance in his portfolios. He took some profit and implemented some derivative strategies in February on equities and fixed income for downside protection.

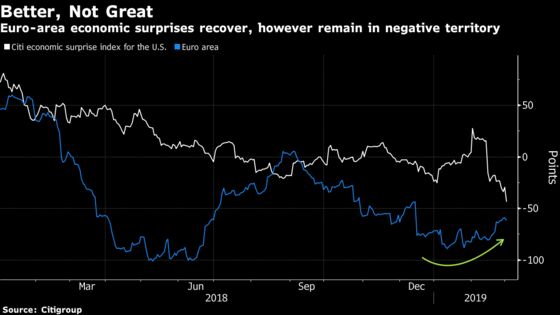

With a week of critical macro news ahead, including the ECB meeting, there could be fresh reasons for caution. “European data was abysmally poor recently, still stocks have rallied with the U.S.,” Deka portfolio manager Uwe Maderer said in an email. He pointed out that Purchasing Managers’ Index data for France and Germany were better than the euro area, and speculated that Italy must be lagging.

From a technical view, short-term participants may use every excuse to exit the rally. There is no clear sell-signal yet, nor a reason to jump onto the running train at this point. But as illustrated below, yesterday’s move in Asia is an alarm bell that may soon be heard in Europe as well.

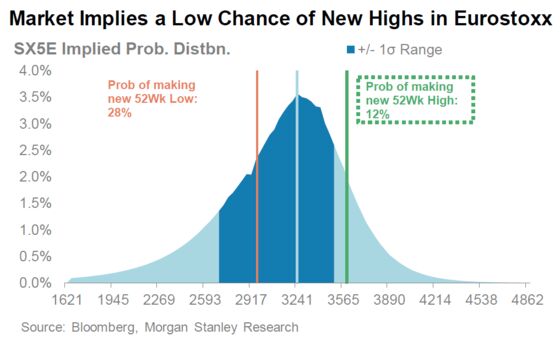

Turning to derivatives, Morgan Stanley strategists have looked into volatility to assess the odds of a bigger rally and these aren’t a pleasant read. The options-implied probability of the Euro Stoxx 50 making a new 52-week high is about 12 percent, and the analysts see more opportunities to buy volatility than sell it, as trade optimism and a dovish Fed are in the price.

Does it mean the market rally should stop? JPMorgan strategists acknowledge the run may look stretched and could take a breather. Still, they recommend buying into any consolidation period as they see more upside momentum, while investors’ positioning may improve as seasonals in March and April are favorable. The next few weeks of flows will tell us if this is likely to materialize. In the meantime, equities didn’t pause yesterday and Euro Stoxx 50 futures are little changed ahead of the open.

- Watch trade sensitive shares, particularly miners and steelmakers, after China cut its economic growth target to a level where the lowest point would mark the slowest pace of growth for three decades but also announced a major tax cut.

- Watch software names after U.S. cloud software maker Salesforce fell in extended trading after a revenue forecast which fell short of estimates. Watch SAP as the clearest peer to Salesforce in Europe, though the news could read across into other software stocks including Micro Focus, Dassault Systemes and Nemetschek.

- Watch the pound and U.K. stocks as the U.K. says there is more work to be done on the controversial Irish backstop, forcing negotiators to reach for some obscure international treaty law as a way to get around the sticking points.

- Watch for trade losers, with further evidence the U.S. economy is suffering, and more pain for gold as appetite for the safe haven abates.

COMMENT:

- “Despite the strong start to 2019, fund flows into ETF and mutual funds have not reflected the same enthusiasm. Investor caution doesn’t bode well for continued equity market strength like we’ve seen, but a lot hangs on the outcome of U.S.-China Trade relations,” Citi strategists wrote in a note. “The valuation spread in low risk has narrowed, but is still at historical wide. This suggests that the premium investors are willing to pay to stay defensive has moderated in the first two months of 2019, but it still high when compared to history.”

COMPANY NEWS AND M&A:

- Evonik Agrees to Sell Plexiglas Unit to Advent for $3.4 Billion

- Evonik Full Year Dividend Per Share Misses Estimates

- Peugeot Owner’s CEO Said to Seek Deals After Reviving Europe

- VW CEO Diess Says Brand Portfolio Under Review

- Italy’s State Lender May Back Elliott at Tel Italia Vote: Stampa

- Ghosn Closer to Release as Tokyo Court Grants Bail Request (1)

- BHP Group’s Henry Says No ‘Secret Lever’ to Lift Iron Ore Output

- Credit Agricole to Present Strategic Plan in June: Les Echos

- Siltronic 2018 Dividend EU5.00/Share, Est. EU4.84 (1)

- Nordea Gets Drawn Deeper Into Nordic Dirty Money Scandal

- Lindt & Spruengli Full Year Ebit Meets Estimates

- Oerlikon Full Year Ebit 2.6% Below Estimates

- Garanti Bank Proposes No Dividend Payout From 2018 Profit

- Zumtobel Nine Month Adjusted Ebit EU23.9 Mln

- Eurofins CEO Says to Reduce M&A and Capex, Focus on Margins

- Angry Birds Maker Rovio Actively Seeking M&A Targets, CEO Says

NOTES FROM THE SELL SIDE:

- Morgan Stanley writes that the de-rating of Voestalpine’s shares is overdone and creates "a rare opportunity" to get some exposure to the business, upgrading the stock to overweight from equal-weight. The bank sees ~30% upside from re-rating if market gets convinced FY20 Ebitda can be reached.

- Liberum says African Swine Fever should benefit Genus in the longer-term, despite the disease “keeping a lid” on the artificial insemination company’s short-term forecasts. Upgrades to buy from hold, PT to 2500p from 2400p; also acts as corporate broker.

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 379.9 (23.6% Fibo); 383.5 (trend line)

- Support at 374.4 (June 2018 low); 369.8 (200-DMA)

- RSI: 71.1

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,340 (June low); 3,368 (trend line)

- Support at 3,315 (38.2% Fibo); 3,287 (200-DMA)

- RSI: 72.5

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- DWS upgraded to buy at Citi

- Genus upgraded to buy at Liberum; PT 25 Pounds

- Greene King upgraded to neutral at JPMorgan; PT 7.20 Pounds

- Mitchells & Butlers raised to overweight at JPMorgan

- Salzgitter upgraded to buy at Bankhaus Lampe; PT 35 Euros

- Semperit Upgraded to Hold at Erste Group; PT 13.20 Euros

- Voestalpine raised to overweight at Morgan Stanley; PT 36 Euros

DOWNGRADES:

- Altice Europe cut to underweight at Barclays; PT 1.50 Euros

- EON downgraded to neutral at JPMorgan; PT 10.20 Euros

- ICADE cut to neutral at Kempen & Co; Price Target 76 Euros

- Iliad downgraded to equal-weight at Barclays; PT 105 Euros

- Innogy cut to underweight at JPMorgan; Price Target 36.76 Euros

- Moncler downgraded to hold at Berenberg

- Orange downgraded to equal-weight at Barclays; PT 16.50 Euros

- Safestore cut to sell at Kempen & Co; Price Target 5.40 Pounds

- United Utilities downgraded to neutral at Citi

- Wacker Chemie Cut to Hold at SocGen; Price Target 100 Euros

- Xior Student Housing cut to neutral at Kempen & Co; PT 42 Euros

- Young & Co’s downgraded to neutral at JPMorgan; PT 12.90 Pounds

INITIATIONS:

- Big Yellow Group rated new buy at Panmure Gordon

- Capital & Regional rated new hold at Panmure Gordon; PT 30 Pence

- Grainger rated new buy at Panmure Gordon; PT 2.80 Pounds

- Hammerson rated new sell at Panmure Gordon; PT 3.20 Pounds

- Intu rated new sell at Panmure Gordon; PT 1.05 Pounds

- PRS REIT rated new buy at Panmure Gordon; PT 1.07 Pounds

- Safestore rated new hold at Panmure Gordon; PT 6.35 Pounds

- Segro rated new buy at Panmure Gordon; PT 7.12 Pounds

- Unite Group rated new hold at Panmure Gordon; PT 9.28 Pounds

- Workspace rated new buy at Panmure Gordon; PT 10.63 Pounds

MARKETS:

- MSCI Asia Pacific up 0.5%, Nikkei 225 down 0.4%

- S&P 500 down 0.4%, Dow down 0.8%, Nasdaq down 0.2%

- Euro down 0.14% at $1.1324

- Dollar Index up 0.04% at 96.72

- Yen down 0.15% at 111.92

- Brent down 0.5% at $65.4/bbl, WTI down 0.4% to $56.4/bbl

- LME 3m Copper up 0.8% at $6460/MT

- Gold spot little changed at $1287.3/oz

- US 10Yr yield little changed at 2.72%

MAIN MACRO DATA (all times CET):

- 9:15am: (SP) Feb. Markit Spain Services PMI, est. 54.3, prior 54.7

- 9:15am: (SP) Feb. Markit Spain Composite PMI, est. 53.9, prior 54.5

- 9:45am: (IT) Feb. Markit/ADACI Italy Services PMI, est. 49.5, prior 49.7

- 9:45am: (IT) Feb. Markit/ADACI Italy Composite PMI, est. 48.6, prior 48.8

- 9:50am: (FR) Feb. Markit France Services PMI, est. 49.8, prior 49.8

- 9:50am: (FR) Feb. Markit France Composite PMI, est. 49.9, prior 49.9

- 9:55am: (GE) Feb. Markit Germany Services PMI, est. 55.1, prior 55.1

- 9:55am: (GE) Feb. Markit/BME Germany Composite PMI, est. 52.7, prior 52.7

- 10am: (EC) Feb. Markit Eurozone Services PMI, est. 52.3, prior 52.3

- 10am: (EC) Feb. Markit Eurozone Composite PMI, est. 51.4, prior 51.4

- 10am: (IT) 4Q F GDP WDA YoY, est. 0.1%, prior 0.1%

- 10am: (IT) 4Q F GDP WDA QoQ, est. -0.2%, prior -0.2%

- 10am: (UK) Feb. New Car Registrations YoY, prior -1.6%

- 10:30am: (UK) Feb. Markit/CIPS UK Services PMI, est. 49.9, prior 50.1

- 10:30am: (UK) Feb. Markit/CIPS UK Composite PMI, est. 50.1, prior 50.3

- 10:30am: (UK) Feb. Official Reserves Changes, prior $1.54b

- 11am: (EC) Jan. Retail Sales MoM, est. 1.3%, prior -1.6%

- 11am: (EC) Jan. Retail Sales YoY, est. 2.1%, prior 0.8%

To contact the reporters on this story: Michael Msika in London at mmsika4@bloomberg.net;Jan-Patrick Barnert in Frankfurt at jbarnert3@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Jon Menon

©2019 Bloomberg L.P.