Rally Time or Time Out? Wall Street Asks What's Next for Stocks

Rally Time or Time Out? Wall Street Asks What's Next for Stocks

(Bloomberg) -- The easing of U.S.-China trade tensions might not be as unabashedly bullish as investors had expected.

An early 440-point gain in the Dow Jones Industrial Average shrank to 132 points by late morning as investors weighed President Donald Trump’s weekend agreement to delay a planned increase in tariffs on Chinese goods. It’s since recovered to about 250 points but the warning to bulls sounding the all-clear for a year-end rally was unmistakable.

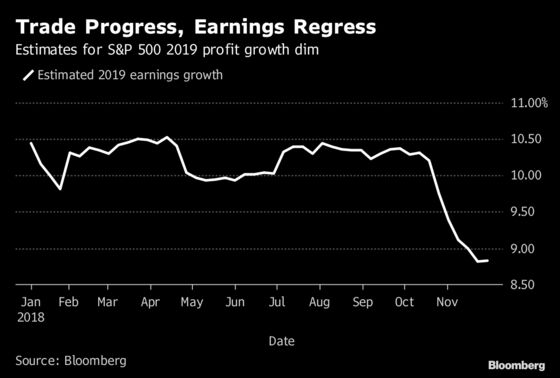

While the combination of a less-aggressive Federal Reserve and ebbing trade tensions sparked the best week for U.S. stocks in seven years, Wall Street remains split on whether that’s enough to overcome the weakening global economic fundamentals that sent the S&P 500 Index into a correction last month.

For Peter Tchir, head of macro strategy at Academy Securities, the truce opens the path to a more lasting trade deal, clearing the way for a rally in risk assets.

“I’m staying the risk-on course for now,” he wrote in a note to clients Monday. “Still nervously, but the number of people who have expressed interest in fading this risk-on move gives me the conviction it has more room to run. Within the next 24 hours equities will likely trade lower, U.S. Treasury yields will come back in, but within the next 48 hours stocks will be higher, Treasury yields higher and credit spreads tighter.”

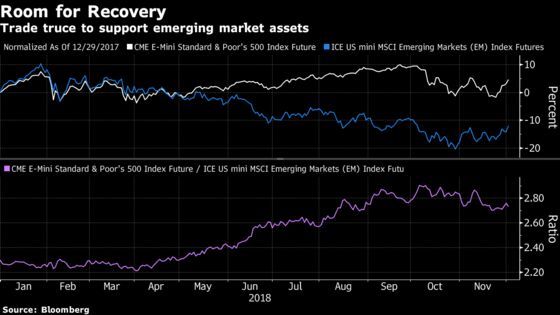

The S&P 500 rose 0.8 percent to 2,782 as of 12:25 p.m. in New York, cutting a gain that reached 1.5 percent. The 10-year Treasury yield rose to 3.05 percent before settling just below 3 percent. The dollar slumped and emerging-market equities surged 2.4 percent.

Consumer discretionary and energy shares paced gains in American equities, closely followed by technology stocks that bore the brunt of selling during the correction. For the trade-truce rally to persist, it may need leaders other than the stocks that carried U.S. indexes to all-time highs in September, according to Evercore ISI.

“A return to multiple months of growth and momentum leadership remains unlikely given the persistent headwinds of slowing economic and earnings growth,” Dennis Debusschere, head of portfolio strategy at Evercore ISI, wrote in a note to investors.

Short-Term Positives

Investors rattled by the correction positioned for possible progress ahead of the talks by owning option bets that pay off if equities rise -- an unusual approach since bullish bets usually come in the form of buying stocks themselves, according to Pravit Chintawongvanich, equity derivatives strategist at Wells Fargo Securities.

This dynamic provides a narrow window in which the S&P 500 could be squeezed up to 2,800-2,825 over the next few sessions, he said in a Friday note.

“In the near term, risk is rallying because 1) vol (uncertainty risk) was priced too high going into the event, and 2) the buildup in upside calls means dealers are ‘short gamma’ and buying stock to hedge, exacerbating the move higher,” he said on Monday. “The ’upside hedging’ means the pain trade is to the upside.”

Stocks fell from their highs on Monday in part because traders were monetizing gains on call options that expire Dec. 7 to lock in profits, the strategist added.

Quants are confident the advance has more room to run compared to the 2.1 percent relief rally in the S&P 500 that followed the U.S. midterm elections -- but warn it might not persist.

“We expect speculative fast money investors such as CTAs and global macros to increase their pace of buying from here on,” writes Masanari Takada, quantitative strategist at Nomura.

Emerging Strength

A temporary trade detente may be all that embattled emerging-market assets need to make up ground on their American counterparts. Indeed, while U.S. stocks have pared a substantial part of Monday’s gains, emerging-market equities are maintaining most of theirs.

“Following what we expect will be a significant Fed-induced relief this week, the mini-positive trend in EM may keep the asset class in a good spot between now and the beginning of January,” writes Luis Costa, head of CEEMEA strategy at Citigroup.

“The truce will be enough to keep the EM rally going through the end of 2018,” said Per Hammarlund, chief emerging-markets strategist at SEB SA in Stockholm. “In addition, EM risk appetite will get another boost from reduced inflationary pressure in both DM and EM since October.”

The Turkish lira, Brazilian real, South African rand, Indian rupee, and Indonesian rupiah should do particularly well in 2019 if investors price in a slower pace of global monetary tightening, the firm said.

This weekend’s progress was sufficient to get Morgan Stanley strategists to upgrade their positive forecast for Chinese stocks in 2019, expecting double-digit upside for the CSI 300 and the Hang Seng Index.

An extra fillip for developing nations could come from a weaker greenback, as there’s less need to seek safety in dollar-denominated assets perceived as more immune from conflicts over cross-border commerce.

“The bottom line is that global equity markets have been handed an early Xmas present wrapped in lower bond yields, weaker energy prices and a postponement in a debilitating trade war,” writes Sean Darby, chief global equity strategist at Jefferies. “Only the dollar hasn’t heard the referees’ whistle.”

--With assistance from Aline Oyamada and Sarah Ponczek.

To contact the reporter on this story: Luke Kawa in New York at lkawa@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Andrew Dunn

©2018 Bloomberg L.P.