Rally Skeptics Might Want to Look at Dividends: Taking Stock

Rally Skeptics Might Want to Look at Dividends: Taking Stock

(Bloomberg) -- Want the lowdown on European markets? In your inbox before the open, every day. Sign up here.

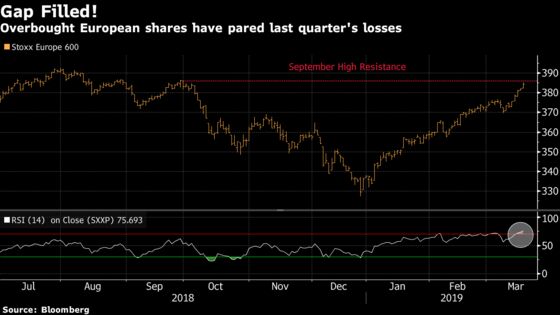

This has been quite a rally that has caught a lot of portfolio managers by surprise. With the Stoxx 600 now firmly in overbought territory, it’s worth having a look again at the longer-term picture for positioning and valuation.

According to Bank of America Merrill Lynch’s latest poll of fund managers, European equities are still the most crowded short among global assets. The region’s stocks have only beaten their peers in two quarters every two years, yet, given the shorts, the strategists suggest they’ll soon do it again.

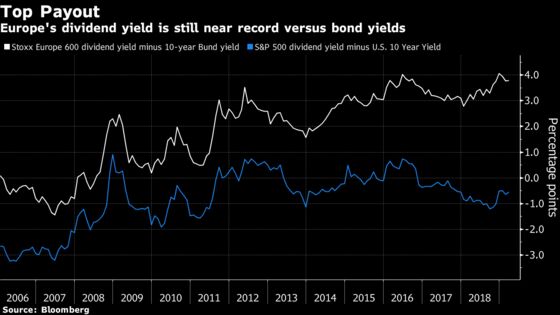

In terms of valuation, one thing to keep in mind is the dividend yield. Bund yields and other risk-free assets are hovering at a very low level, keeping the gap with dividends near historical highs. And about 80 percent of European companies have a dividend yield above their corporate bond yield.

Goldman Sachs strategists are neutral to slightly bearish on European stocks, but are optimistic about dividends and payout ratios. They see the low leverage of companies supporting cash returns, while expecting a 2 percent 2019 earnings-per-share growth forecast to be enough to sustain the payouts.

Ah, “but what about the dangers of value traps?” you might ask, whereby a stock appears cheap only for the shares to fall further or for the company to cut its dividend. For Goldman strategists, the timing is right to play the high dividend yield that’s on offer.

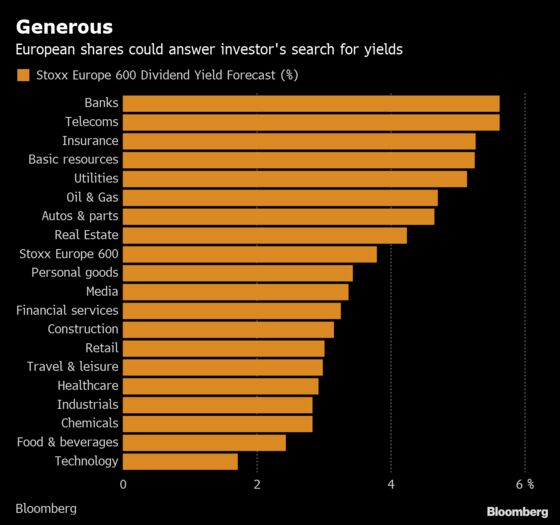

And Citigroup strategists share the view, citing strong balance sheets, surplus free cash flow, and high payout ratios of European shares. Sector-wise, basic resources, industrials, banks, oil & gas and insurance score best on dividend metrics, they said. They name Aviva, Deutsche Post, KBC, Lloyds and Volvo as “Dividend Kings.” Looking for dividend distortions, the strategists identify “cheap versus expensive” stocks and cite Adecco against Nestle, BNP versus Air Liquide, and Aviva versus Diageo.

| Stock | Est. Div. Yield | Stock | Est. Div. Yield |

| BNP Paribas | 6.7% | Air Liquide | 2.4% |

| Adecco | 4.6% | Nestle | 2.6% |

| Aviva | 7.1% | Diageo | 2.3% |

| Source: Bloomberg | |||

Ahead of the open today, Euro Stoxx 50 futures are down 0.5 percent.

- Watch European logistics names after U.S. delivery operator FedEx trimmed its annual profit forecast for the second time in three months, sending its shares lower in late trading. FedEx blamed the outlook cut on slowing global growth and rising costs from an acquisition made in Europe in 2016. Watch Deutsche Post, Royal Mail, Bpost, PostNL, Austrian Post and Poste Italiane.

- Watch satellite industry stocks after U.K. firm Inmarsat confirmed it has received a $3.3b takeover offer after the bell on Tuesday, with a 24% premium to the closing price. Watch peers including SES and Eutelsat, the latter of which weighed an offer for Inmarsat last year before eventually backing off.

- Watch the pound and U.K. stocks as the European Union is likely to give Theresa May until mid-April to decide whether to extend Brexit to 2020 or leave the bloc without a deal at the end of June. Yet from the pound to stocks, markets are getting optimistic.

- Watch trade-sensitive sectors after negotiators are concerned China is pushing back on the demands being made, reportedly because it hasn’t received assurances that the tariffs slapped on Chinese goods will be removed. The noise on the U.S.-Europe side of the trade war doesn’t sound too happy either. Watch carmakers and parts suppliers in particular after Nissan is said to cut a future target for car sales in China by around 8%.

COMPANY NEWS AND M&A:

- Bayer Loses First Phase of Roundup Trial, Liability Up Next

- Bayer down 10% on Tradegate vs Xetra close

- Inmarsat Receives $3.3 Billion Private Equity-Led Bid

- Fuchs Petrolub Sees Revenue +2% to +4% While Ebit to Fall

- Kappahl Reports Unexpected Second Quarter Profit

- Cellnex Looks to Buy Majority Stake in TDF: Expansion

- Zooplus Sees 2019 Pretax Loss EU15 Mln To Pretax Profit EU5 Mln

- Norma Full Year Dividend Per Share Misses Estimates

- Merck KGaA, Pfizer Discontinue Phase III Javelin Ovarian Trial

- Novartis Says Probe Found No Trace of Payoffs to Greek Officials

- Ex-Altria CEO Tapped at World’s Biggest Brewer Amid Beer Slump

- TechnipFMC Gets Sverdrup Phase 2 Subsea Contract From Equinor

- Big Tobacco’s Legal Woes in Canada Pose Severest Risk in Decades

NOTES FROM THE SELL SIDE:

- Morgan Stanley upgrades Teleperformance to overweight from equal-weight, saying the company may face some concerns longer term, but near-term gains look attractive. Within the business services sector, Morgan Stanley prefers Teleperformance, DCC, Applus, Ashtead and Hays, while it’s cautious on Bunzl, Eurofins and Experian.

- RBC raised Beiersdorf to outperform from sector perform, with more than a 23% increase in price target to EU100, saying the company deserves credit for step up in revenue investment.

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 392.7 (July high); 397.9 (May high)

- Support at 379.9 (23.6% Fibo); 369.3 (200-DMA)

- RSI: 75.7

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,466 (23.6% Fibo); 3,596 (May high)

- Support at 3,349 (August low); 3,315 (38.2% Fibo)

- RSI: 77.4

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- B&S Group raised to overweight at Morgan Stanley; PT 16.50 Euros

- Beiersdorf upgraded to outperform at RBC; PT 100 Euros

- Deutsche Post upgraded to buy at HSBC; PT 36 Euros

- Lastminute.com upgraded to outperform at Mediobanca SpA

- TLG Immobilien upgraded to buy at HSBC; Price Target 28.50 Euros

- TUI upgraded to buy at Oddo BHF

- Teleperformance raised to overweight at Morgan Stanley

- Zurich Airport upgraded to neutral at Goldman; PT 174 Francs

DOWNGRADES:

- Aena downgraded to sell at Goldman; PT 152 Euros

- Antofagasta downgraded to reduce at HSBC; PT 7.90 Pounds

- Bayer downgraded to neutral at MainFirst; PT 60 Euros

- DSV downgraded to hold at HSBC; PT 620 Kroner

- Eurofins Scientific cut to hold at Jefferies; PT 400 Euros

- Fraport downgraded to sell at Goldman; PT 67 Euros

- Getlink SE cut to neutral at Goldman; Price Target 15.30 Euros

- Motor Oil Hellas downgraded to hold at HSBC; PT 24 Euros

- Rheinmetall downgraded to hold at HSBC; PT 110 Euros

- Veolia downgraded to neutral at JPMorgan; PT 20.50 Euros

INITIATIONS:

- Puma rated new buy at SocGen; PT 627 Euros

- Yellow Cake rated new buy at Cantor; PT 3 Pounds

MARKETS:

- MSCI Asia Pacific little changed, Nikkei 225 up 0.2%

- S&P 500 little changed, Dow down 0.1%, Nasdaq up 0.1%

- Euro down 0.03% at $1.1349

- Dollar Index up 0.08% at 96.46

- Yen down 0.14% at 111.55

- Brent up 0.1% at $67.7/bbl, WTI little changed $59/bbl

- LME 3m Copper down 0.1% at $6455/MT

- Gold spot little changed at $1305.9/oz

- US 10Yr yield little changed at 2.61%

MAIN MACRO DATA (all times CET):

- 10:30am: (UK) Feb. CPIH YoY, est. 1.8%, prior 1.8%

- 10:30am: (UK) Feb. CPI MoM, est. 0.4%, prior -0.8%

- 10:30am: (UK) Feb. CPI YoY, est. 1.8%, prior 1.8%

- 10:30am: (UK) Feb. CPI Core YoY, est. 1.9%, prior 1.9%

- 10:30am: (UK) Feb. Retail Price Index, est. 285.1, prior 283

- 10:30am: (UK) Feb. RPI MoM, est. 0.7%, prior -0.9%

- 10:30am: (UK) Feb. RPI YoY, est. 2.5%, prior 2.5%

- 10:30am: (UK) Feb. RPI Ex Mort Int.Payments (YoY), est. 2.5%, prior 2.5%

- 10:30am: (UK) Feb. PPI Input NSA MoM, est. 0.6%, prior -0.1%

- 10:30am: (UK) Feb. PPI Input NSA YoY, est. 4.1%, prior 2.9%

- 10:30am: (UK) Feb. PPI Output NSA MoM, est. 0.1%, prior 0.0%

- 10:30am: (UK) Feb. PPI Output NSA YoY, est. 2.2%, prior 2.1%

- 10:30am: (UK) Feb. PPI Output Core NSA MoM, est. 0.2%, prior 0.4%

- 10:30am: (UK) Feb. PPI Output Core NSA YoY, est. 2.3%, prior 2.4%

- 10:30am: (UK) Jan. House Price Index YoY, est. 2.4%, prior 2.5%

- 12pm: (UK) March CBI Trends Total Orders, est. 4.5, prior 6

- 12pm: (UK) March CBI Trends Selling Prices, prior 22

--With assistance from Hanna Hoikkala.

To contact the reporter on this story: Michael Msika in London at mmsika4@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Jon Menon

©2019 Bloomberg L.P.