Rally Killer Resurfaces as Stocks and Volatility Gain in Tandem

Rally Killer Resurfaces as Stocks and Volatility Gain in Tandem

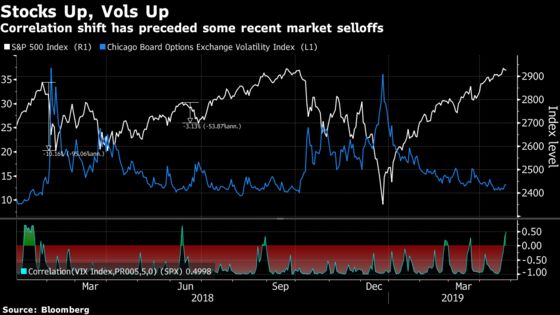

(Bloomberg) -- Volatility markets may be flashing a warning to U.S. stocks.

As the S&P 500 reclaims fresh record highs, the Cboe Volatility Index has crept up, with the five-session correlation between the two strengthening to levels not seen since the middle of 2018.

This relatively rare dynamic has often portended a retreat in U.S. equities. The benchmark stock gauge and the VIX, which measures implied share swings over the next month, are negatively correlated because markets tend to move more violently on the way down.

The last time the VIX and S&P 500 were moving in tandem like this, the latter sold off by more than 3 percent over the next two weeks. An even-more robust episode at the start of 2018 ended with the biggest one-day jump ever in the volatility gauge on Feb. 5, which felled exchange-traded products that let investors bet on enduring tranquility.

Implied correlations among S&P 500 constituents are also starting to inch higher as earnings season progresses -- a period in which stocks have the most reason to dance to the beat of their own drummers. That’s contributing to an upward drift in measures of implied volatility. The VIX edged higher to 13.25 on Thursday, a level still well below its historical average, as U.S. equities ended flat.

For Pravit Chintawongvanich, Wells Fargo’s equity derivative strategist, there’s a more benign explanation: The phenomenon is a reminder that the VIX’s nickname -- the fear gauge -- can be a misnomer.

“In an environment where volatility is very low and stocks are near highs, larger-than-expected rallies can make volatility go up,’’ he said. “After all, volatility reflects both upside and downside movement.’’

The S&P 500’s biggest moves over the past month -- that is, times of higher realized volatility -- have occurred on up rather than down days, he added.

While a market melt-up may come to mind, there are some key differences between January 2018 and today. Chiefly, positioning.

Limited flows into U.S. equity funds and low implied hedge-fund exposure to the market stand in stark contrast to the conditions prevailing in early 2018, when corporate tax cuts galvanized investors’ enthusiasm for U.S. stocks.

In addition, there’s much less complacency evident in what awaits U.S. shares relative to their recent history. The volatility risk premium -- the difference between implied gyrations and realized -- was much tighter in January 2018 than it is at present.

To contact the reporter on this story: Luke Kawa in New York at lkawa@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Joanna Ossinger, Yakob Peterseil

©2019 Bloomberg L.P.