Rally Caught by Stretched Signals and Bad Numbers: Taking Stock

Rally Caught by Stretched Signals and Bad Numbers: Taking Stock

(Bloomberg) -- After a pretty good run, we had our first dismal trading day in over a week. Trade clouds re-emerged, reminding us that equities remain exposed to a quick change in sentiment. The dovish tone from the Fed had a very short-lived positive impact on stocks, and the S&P ended the day lower.

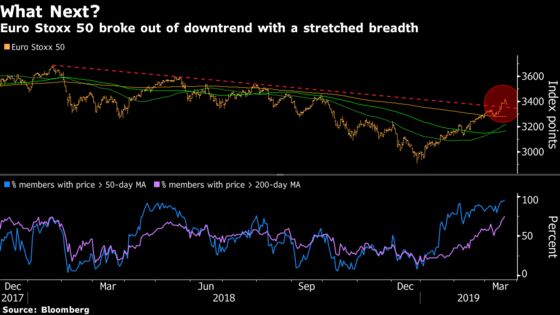

In Taking Stock last week we mentioned that the blue-chip Euro Stoxx 50 Index was sending some mixed signals. So far the bulls have kept the upper hand and pushed the gauge above a trend line that dates back to May 2018. Now, more than 75 percent of the benchmark’s components are above their 200-day moving average. On top of that, 30 percent of the constituents are now overbought, according to technical analysis. So will success bring vulnerability?

“The market had a brutal approach in pricing risks like trade and Brexit in the last quarter of 2018,” commented Andre Koppers, a portfolio manager at Oberbanscheidt & Cie. “Those negative surprises have reduced in 2019 and stock markets have stabilized. We see this continuing, however in a volatile environment.”

Indeed, the picture is more reassuring for the bigger Stoxx Europe 600 Index. Only 12 percent of its members are in overbought territory and sell signals are on the decline.

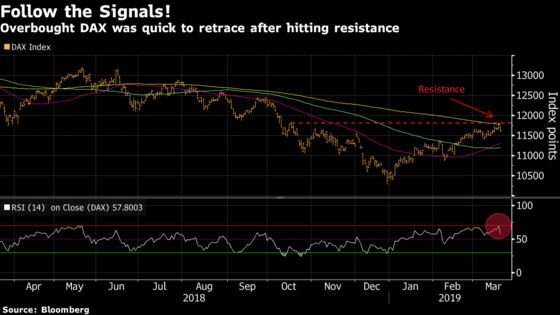

There are still areas of gloom, such as Germany’s DAX. The benchmark is vulnerable to trade jitters as its car industry is far from being out of the woods. Yesterday, BMW warned earnings will fall “well below” last year’s level, adding to the woes of an already disrupted industry. No wonder the DAX is the worst-performing index among major European peers this year.

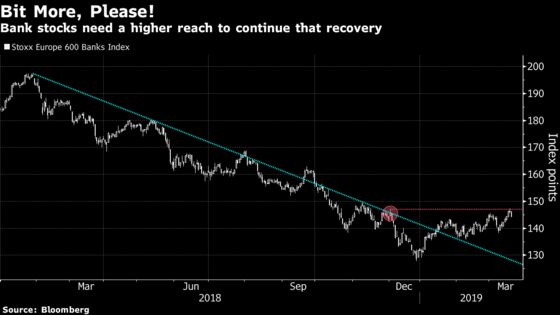

And of course, there are the banks. Just as it looked like things were turning for the better, as lenders overcame the bad news from the ECB’s guidance shift, UBS killed the mood. The Swiss bank’s CEO even qualified the first quarter as one of the worst in recent history. Earnings in Europe for the period kick off on April 25 with UBS’s cross-town rival Credit Suisse. That leaves four weeks for bank chiefs to further steer the market.

And it seems that strategists are now starting to cast doubt on the new-year rally in European equities, and expect the Stoxx Europe 600 to lose 6 percent from Wednesday’s closing levels to 358 points by the end of 2019, according to our latest survey. Grim. In the meantime, Euro Stoxx 50 futures are trading little changed ahead of the open.

- Watch for further impact from the Fed’s dovish stance, with no interest rate hikes coming in 2019. Treasury yields dropped to the lowest in more than a year. The central bank’s unexpected move to scrap its forecast for rate hikes this year has led to increased bets that a cut will happen. Dollar bears may be pleased, but investors are dubious.

- Watch semiconductors after U.S. memory chip maker Micron Technology said it will cut production in response to a slump in demand for its key products but indicated the bottom of the chip cycle is in view. Watch chipmakers like STMicroelectronics, Infineon and AMS and chip equipment firms ASML, ASM International and BE Semiconductor.

- Watch food-delivery firms Just Eat, Delivery Hero, and Takeaway.com after ride-sharing firm Bolt said it intends to expand into the European market.

- Watch the pound and U.K. stocks after the short delay requested by Theresa May pushed the U.K. to the brink of crashing out without a deal, to the dismay of British business and JPMorgan’s boss, unless May betting on a short delay forces lawmakers to act.

COMMENT:

- “We keep a cautious stance on euro-zone equities due to ongoing political uncertainty and structural issues, although a dovish European Central Bank should provide a floor for euro-zone equities’ underperformance,” Credit Suisse investment strategists wrote in their monthly note. “Following their strong underperformance last year, German equities appear best-positioned to benefit markedly from an expected recovery in global manufacturing activity.”

COMPANY NEWS AND M&A:

- Wirecard COO Was Aware of Allegedly Fraudulent Transactions: FT

- Carlsberg Faces EU250 Million Fine in German Cartel Case: Finans

- Ion Beam Full-Year Revenue Misses Lowest Estimate

- Meyer Burger Full-Year Sales Miss Lowest Estimate

- Hornbach Group FY Prelim. Adjusted EBIT EU135M, Est. EU149.75M

- Elior in Talks With PAI on Potential Sale of Catering Activities

- HeidelbergCement Sees Growth in 2019 as Profit Hurt by Weather

- VPS Healthcare Said to Reconsider London Listing on Brexit Woes

- Skanska: Unlikely to Reach Construction Margin Target in 2019-20

- Wendel FY Net Income Falls; Plans EU200m Share Buyback

- EssilorLuxottica’s Del Vecchio Links Fight to Promotions: Figaro

NOTES FROM THE SELL SIDE:

- Berenberg cut Bodycote to hold from buy, arguing the shares are fairly valued following a recovery, and adding that the industrial heat-treatment firm is “not immune” to the macroeconomic slowdown. However, the broker raised its PT to 940p from 915p.

- Gamma is rated a new buy at Jefferies, which sees substantial growth potential ahead, with the market continuing to shift away from legacy technologies and a new phase of adding capabilities to hosted phone systems underway.

- Berenberg says Merlin Entertainments may fail to achieve Ebit growth in any division this year, even with its cost-savings plan and continued investment in hotels and sites. The broker cuts rating to sell and PT to 315p.

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 392.7 (July high); 397.9 (May high)

- Support at 379.9 (23.6% Fibo); 369.2 (200-DMA)

- RSI: 65.8

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,466 (23.6% Fibo); 3,596 (May high)

- Support at 3,349 (August low); 3,315 (38.2% Fibo)

- RSI: 66.1

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- Bouygues upgraded to outperform at MainFirst; PT 37 Euros

- EasyJet upgraded to neutral at MainFirst; PT 13 Pounds

- Eurocommercial GDRs upgraded to hold at SocGen; PT 26 Euros

- ING Groep raised to outperform at RBC; Price Target 14.50 Euros

- Lanxess upgraded to hold at Berenberg

- Ryanair upgraded to outperform at MainFirst; PT 15 Euros

DOWNGRADES:

- Bodycote downgraded to hold at Berenberg

- Compass downgraded to sell at Goldman; PT 16.50 Pounds

- Hoist Finance cut to hold at Pareto Securities; PT 40 Kronor

- IAG downgraded to neutral at MainFirst

- Lookers downgraded to neutral at JPMorgan; PT 98 Pence

- Lufthansa downgraded to underperform at MainFirst; PT 18 Euros

- Merlin downgraded to sell at Berenberg

- Munich Re downgraded to hold at Jefferies; PT 212 Euros

- SGS downgraded to sell at Goldman; PT 2,400 Francs

- Sodexo downgraded to sell at Goldman; PT 89 Euros

- Tryg downgraded to sell at SEB Equities; PT 175 Kroner

INITIATIONS:

- Assura rated new neutral at JPMorgan; PT 60 Pence

- Autogrill rated new buy at Goldman; PT 11 Euros

- Capital & Counties rated new hold at Panmure Gordon

- Derwent London rated new hold at Panmure Gordon; PT 32.96 Pounds

- Elior Group rated new neutral at Goldman; PT 12.60 Euros

- Gamma Communications rated new buy at Jefferies; PT 11.30 Pounds

- Great Portland rated new hold at Panmure Gordon; PT 7.41 Pounds

- Helical rated new buy at Panmure Gordon; PT 3.85 Pounds

- Shaftesbury rated new hold at Panmure Gordon; PT 9.35 Pounds

- Somfy rated new buy at Kepler Cheuvreux; PT 92 Euros

- Tikehau Capital rated new buy at Oddo BHF; PT 33.40 Euros

MARKETS:

- MSCI Asia Pacific down 0.1%, Nikkei 225 up 0.2%

- S&P 500 down 0.3%, Dow down 0.5%, Nasdaq up 0.1%

- Euro up 0.09% at $1.1423

- Dollar Index up 0.17% at 95.92

- Yen up 0.19% at 110.49

- Brent up 0.2% at $68.6/bbl, WTI little changed at $60.2/bbl

- LME 3m Copper up 1% at $6519/MT

- Gold spot up 0.5% at $1319.4/oz

- US 10Yr yield down 9bps at 2.53%

MAIN MACRO DATA (all times CET):

- 10am: (SP) Jan. Trade Balance, prior -3.25b

- 10am: (EC) ECB Publishes Economic Bulletin

- 10:30am: (UK) Feb. Public Finances (PSNCR), prior -25.4b

- 10:30am: (UK) Feb. Public Sector Net Borrowing, est. -800m, prior -15.8b

- 10:30am: (UK) Feb. PSNB ex Banking Groups, est. 700m, prior -14.9b

- 10:30am: (UK) Feb. Central Government NCR, prior -25.8b

- 10:30am: (UK) Feb. Retail Sales Ex Auto Fuel MoM, est. -0.4%, prior 1.2%

- 10:30am: (UK) Feb. Retail Sales Ex Auto Fuel YoY, est. 3.5%, prior 4.1%

- 10:30am: (UK) Feb. Retail Sales Inc Auto Fuel MoM, est. -0.4%, prior 1.0%

- 10:30am: (UK) Feb. Retail Sales Inc Auto Fuel YoY, est. 3.3%, prior 4.2%

- 1pm: (UK) March Bank of England Bank Rate, est. 0.75%, prior 0.75%

- 1pm: (UK) March BOE Corporate Bond Target, est. 10b, prior 10b

- 1pm: (UK) March BOE Asset Purchase Target, est. 435b, prior 435b

- 4pm: (EC) March Consumer Confidence, est. -7.1, prior -7.4

--With assistance from Joe Easton.

To contact the reporters on this story: Jan-Patrick Barnert in Frankfurt at jbarnert3@bloomberg.net;Michael Msika in London at mmsika4@bloomberg.net

To contact the editors responsible for this story: Jon Menon at jmenon1@bloomberg.net;Celeste Perri at cperri@bloomberg.net

©2019 Bloomberg L.P.