Quants With $275 Billion Are Buying Sleepiest Stocks Since Crash

Quants With $275 Billion Are Buying Sleepiest Stocks Since Crash

(Bloomberg) -- Volatility markets are flashing the green light for $49 billion of quant-driven cash to pour into U.S. stocks over the next month.

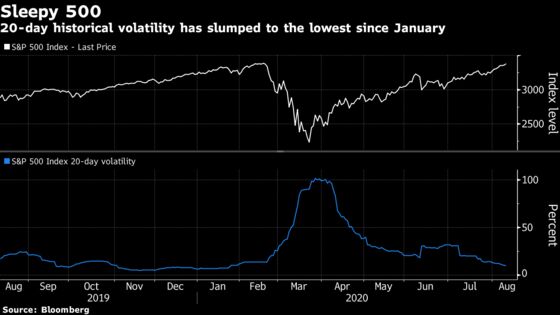

Historical price swings in the Standard & Poor’s 500 Index over 20 days have plummeted to the lowest since January, sending automated buying signals to quant traders that run $275 billion in volatility-targeting strategies.

After deleveraging en masse during the Covid selloff, these funds are set to add fuel to American equities trading around all-time highs, according to investment bank calculations.

Nomura Holdings Inc. estimates that if the S&P 500 swings an average of 1% in either direction every day over the next month, vol-targeting players could snap up $49 billion of stocks. BNP Paribas SA estimates a more conservative $12 billion if realized volatility remains at current levels.

The market calm comes as U.S. equity benchmarks near or surpass all-time highs on the back of central-bank support and hopes the coronavirus will be contained. The S&P 500 has risen for eight consecutive sessions, approaching its record close from before the pandemic.

“We are again seeing vol control ‘light’ of their target equities allocation and reaccelerating purchases,” Nomura strategist Charlie McElligott wrote in a note on Tuesday.

All told, there’s evidence that big-money players beyond vol-control funds are starting to warm to the market, potentially providing more ammo to stock indexes.

A gauge of so-called smart money and CFTC positioning data “now suggest institutional players are entering the market again,” BNP strategists wrote in a note on Tuesday.

©2020 Bloomberg L.P.