Quants With 20% of U.S. Stock Funds Puzzle Over Timing of Cycle

Quants With 20% of U.S. Stock Funds Can't Agree on Cycle Risks

(Bloomberg) -- Wall Street quants are taking sides on the trajectory of the U.S. business cycle -- and money is riding on their investing styles like never before.

The high-stakes call -- risking some of the stock market’s hottest trades -- is reigniting one of the most contested debates in the quantitative community: Can investors time the market? And even if so, should they?

It’s all down to conflicting economic signals in factor investing, which slice and dice equities by their traits like value, volatility and growth. As warnings snowball that markets are entering a new era of tighter global liquidity, the conundrum has gained urgency.

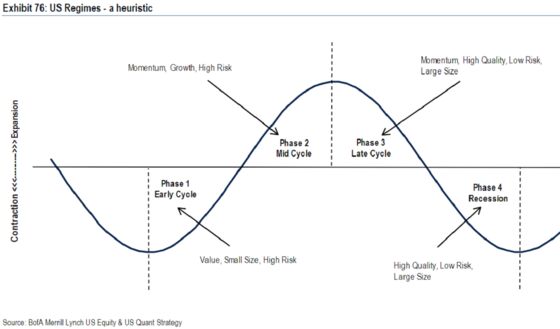

In the green corner is Bank of America, which argues U.S. markets are in the throes of mid-cycle expansion. That is, when “macro indicators are generally above average and improving.” If the strategists are right, riskier factors like momentum -- wagering on stocks with the biggest gains over the past year -- will power quants’ money-making engine going forward.

In the red corner are Sanford C. Bernstein analysts. They cite the outperformance of quality factors like low leverage as a signal that developed markets are engulfed in late-cycle angst. If their bearish prognostications come to pass, some of the most popular bets on market leaders like technology shares are headed for danger.

Conflicting signals

For now, there’s data to back up whichever group of quants you believe. Volatile and momentum equities have continued to notch gains, lending credence to the Bank of America mid-cycle thesis. On the other hand, cheap value shares and those with high leverage have slumped -- both characteristics of late-cycle dynamics.

This is far from an esoteric debate for math geeks. A record swath of the global investment community will be affected by structural shifts in factor performance. About 20 percent of managed U.S. stock assets reside in quantitative strategies, and effectively up to 40 percent in passive, according to JPMorgan Chase & Co.

“The center of gravity has been shifting from a primarily active fundamental approach to more of a quantitative/passive approach that should be primarily analyzed through a factor-driven framework,” strategists at the U.S. bank headed by Dubravko Lakos-Bujas wrote in a Friday note. “As a result, the role of factor analysis has gained increasing importance within the investment process.”

Market Clock

Factor timing has also grown popular as quants in a relatively crowded field try to squeeze out alpha, or outperformance, despite skepticism over the strategy. AQR Capital Management, for example, has long argued that it’s unwise to pop in and out of factor investments merely based on valuation.

In a blog post earlier this month, the firm posited that macro factors can’t explain the slump in value stocks across the board. For example, a stock may be cheap either due to weak growth prospects, poor management, or high debt levels. In each scenario, the equity would react differently to say, high inflation, AQR argues.

Others are happy to assign a big-picture rationale. Take the Bernstein analysis. Companies with low levels of leverage have outperformed across the globe this year -- indicating investors are taking a defensive stance to prepare for a downturn in economic momentum.

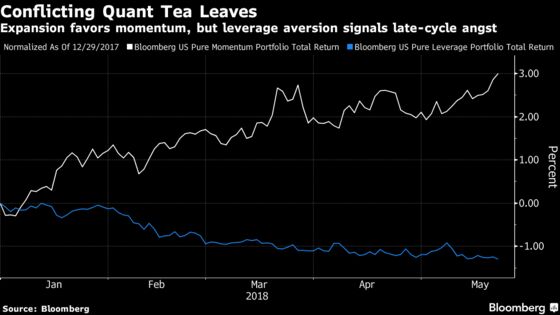

A concentrated portfolio that bets on U.S. companies with the most leverage has been falling for six consecutive quarters, the longest losing streak since March 2009, according to a market-neutral Bloomberg index.

“Late expansion and rising rates are good for low leverage stocks,” the Bernstein team, headed by Alla Harmsworth, wrote in a Friday note.

There’s also evidence that investors aren’t confident over the profit outlook. Companies with high earnings growth have outperformed cheaper companies as money managers flock to stocks that have already proven they can supply profits.

Keep the Faith

All that hasn’t deterred Bank of America, however.

“We expect value could lead in the near-term, given a continued acceleration in profits growth (the critical macro driver of style cycles),” Savita Subramanian, head of U.S. equity and quantitative strategy at the bank, wrote in a note last week.

Supporting Subramanian’s call: A momentum strategy -- buying the best performing U.S. shares over the past year and shorting the worst performers -- is on track to post the best first-half performance since 2011. What’s more, equities with the biggest price swings have climbed for the past consecutive seven weeks, the longest streak since 2012. An appetite for riskier, volatile stocks occurs during expansionary periods, according to analysis conducted by JPMorgan and Bank of America, respectively.

Sure, some of the differences in opinion hinge on how cycles and factors are defined. But with the U.S. economic expansion the second-longest on record, risks for robots and humans alike are rising.

“Momentum becomes most hazardous during contraction when the trends that have driven the market higher until then start to crumble and even reverse,” JPMorgan’s Lakos-Bujas wrote.

To contact the reporter on this story: Dani Burger in London at dburger7@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma, Cecile Gutscher

©2018 Bloomberg L.P.