Quants Holding $1 Trillion Poised to Buy Stocks

Quants Holding $1 Trillion Poised to Buy Stocks

(Bloomberg) -- With the biggest event risk in recent memory over, Wall Street is quietly confident that systematic funds that take their cues from market swings are set to spend billions of dollars, fueling this stock rally.

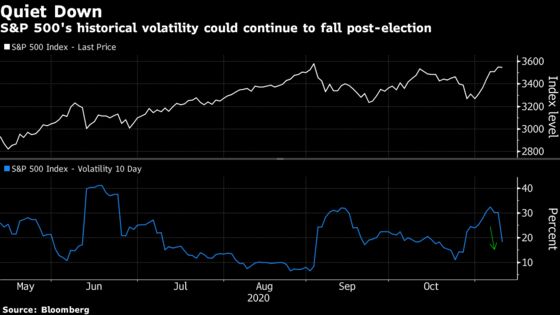

For this $1 trillion cohort, it all hinges on stable prices, a relative rarity during this rocky year. But lately, equities are sending the right signals. Realized volatility is starting to come down in the wake of the U.S. presidential election, while the futures market is more sanguine than it’s been in months.

Sure, this is still 2020: President Donald Trump has yet to concede the election to Joe Biden. Covid hospitalizations are hitting fresh records. Markets are awaiting a stimulus plan from a bickering U.S. Congress.

But the worst looks to be over, with JPMorgan Chase & Co. to Nomura Holdings Inc. projecting that fresh algorithmic money will power stocks into the new year.

“We don’t necessarily see volatility falling off a cliff just yet,” said Maxwell Grinacoff, a strategist at BNP Paribas SA. “However, we could see realized vol get back into the low-teens (~12-14%) as we move into the first quarter of 2021,” he said, referring to the one-month measure.

That means volatility-control strategies could plow between $25 billion and $32 billion into stocks over the next three months, according to Grinacoff. Ten-day historical volatility for the S&P 500 Index has dropped to 18%, the lowest in two weeks.

Other systematic traders would likely join the party, he said. That includes commodity trading advisers, who monitor how risky their exposures are with volatility measures, and risk parity models, which weight their portfolio by asset price swings.

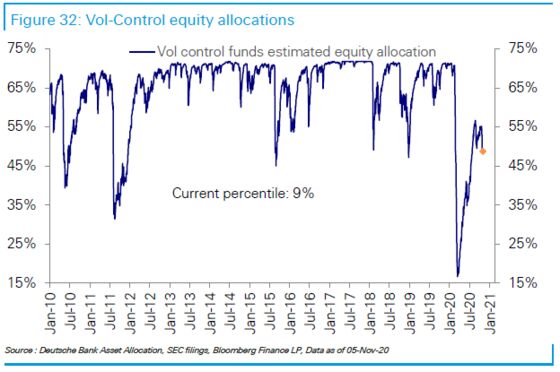

Altogether, these algorithmic players command $1 trillion in assets, according to a Bank for International Settlements estimate. After deleveraging earlier this year during the Covid crash, they’re dramatically underweight equities by historical standards.

Allocations among volatility-control funds are at around the tenth percentile, according to JPMorgan and Deutsche Bank Group AG estimates, which means they have only been lower 10% of the time. Nomura’s model pins this metric at the 16th percentile.

CTA exposure to stocks “remains below the five-year average even after building up some exposure over the summer months,“ according to BNP’s Grinacoff, leaving plenty of room to buy.

JPMorgan’s Marko Kolanovic and Bram Kaplan meanwhile see a virtuous cycle playing out as a Biden presidency ushers in a period of fewer market swings.

“Lower volatility could result in inflows to risk assets (e.g. inflow in volatility sensitive strategies like vol targeting, etc),” they wrote in a note on Nov. 6. “We believe the market should continue moving higher as investors increase exposure to stocks.”

©2020 Bloomberg L.P.