Quants Reboot Factor Investing as Ebbing Demand Bites at ETFs

Quants Reboot Factor Investing as Ebbing Demand Bites at ETFs

(Bloomberg) -- A rough start to the year for more than $850 billion exchange-traded funds with quantitative strategies is fueling a product rethink.

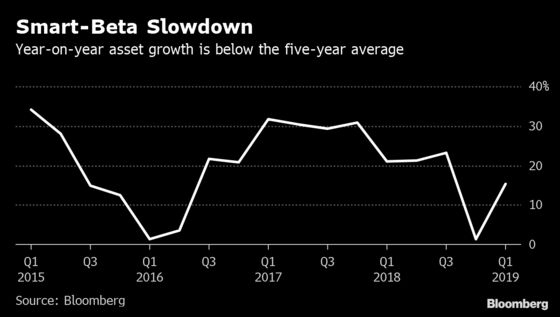

Smart-beta stock ETFs -- which use characteristics such as a company’s value, size or momentum to direct investments -- lured the least money in 12 months in the U.S., dragging asset growth below the five-year average for a second quarter, according to data compiled by Bloomberg. Instead of quitting, ETF providers are doubling down and trying to woo investors with all-in-one funds that pull together several factors.

Money managers have come to rely on smart-beta funds. As differentiated products, they can justify higher fees, offsetting lower revenue from broad-indexed funds -- which are now virtually free. So factor investing is getting a reboot: Rather than teach investors how to pivot between products, issuers are creating multi-factor funds that offer exposure to several return-enhancing characteristics. And that seems to be working.

“The multi-factor funds really address the bulk of investors who want something there, but just don’t know how to play it,” said Paul Kim, the head of ETF strategy at Principal Financial Group Inc., which runs several of the funds. “That’s where we’re seeing the most client demand.”

‘Democratize Access’

Multi-factor ETFs emerged as a bright spot amid the smart-beta slowdown last quarter. These funds added $5.7 billion, half of the overall intake of equity factor funds, with inflows in March exceeding all but one rival -- low volatility, data compiled by Bloomberg show.

No wonder then that BlackRock Inc., Pacific Investment Management Co. and OppenheimerFunds Inc. have all started funds targeting more than one equity characteristic. Many of these funds dynamically rotate between different types of stocks in response to market conditions, countering a concern that buy-and-hold factor investors could suffer long periods of underperformance.

“We want to democratize access to all of those return drivers and make them available for moms and dads,” Andrew Ang, BlackRock’s head of factor investing strategies said at a press briefing last month. “We want to bring these active insights in new ways to all investors.”

BlackRock started a rotating strategy last month, and WisdomTree Investments Inc. gave its Japan- and Europe-focused funds active managers. Meanwhile, Principal’s funds are being used to make a Nasdaq Dorsey Wright model portfolio that rotates between factors, the financial adviser said in March.

More Complex?

But with the flood of new entrants, the devil’s in the detail.

Investors often underestimate the scale of possible losses from multi-factor funds and diversification benefits tend to be overstated, Research Affiliates warned in a paper last year. Complexity is a key reason why adoption by financial advisers has lagged, Cerulli Associates, a Boston-based research and consulting firm, wrote in a report in March.

While a rotating Oppenheimer product adjusts its holdings monthly, for example, a dynamic fund run by Pimco tweaks its fund holdings once a quarter. Oppenheimer’s fund has returned 15 percent over the last year, double Pimco’s product, even though their management fees are the same.

Multi-factor funds do however satisfy asset managers’ hunger for fees, charging an average $4.70 for every $1,000 invested, exceeding the 20 cents charged by the cheapest U.S. ETF and smart-beta ETFs overall. The spate of new funds is likely to continue as a result.

“I haven’t noticed as much fee compression in the active or smart-beta space,” said Lance Humphrey, a money manager in the global multi-assets team at USAA Asset Management, which runs four multi-factor funds. “People are willing to pay a little bit more to get a better outcome.”

--With assistance from Annie Massa.

To contact the reporter on this story: Rachel Evans in New York at revans43@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Rita Nazareth, Dave Liedtka

©2019 Bloomberg L.P.