Quants Cut Stock Exposures to Lowest Since 2014 as S&P Crawled to Record

Quants Cut Stock Exposures to Lowest Since 2014 as S&P Crawled to Record

(Bloomberg) -- As the S&P 500 crawled its way to a new record, some of the smartest investors were creeping to the exit.

Coming into this week, market-neutral quants had cut their gross stock allocations to the lowest in nearly five years, according to data compiled by Credit Suisse Group AG’s prime brokerage.

Conflicting signals on risk appetite and economic growth are whiplashing funds that dissect equities based on traits like value and momentum. All that is stoking factor volatility and increasing the temptation to delever as the anxiety-ridden rally of 2019 rolls on.

The market-neutral cohort, which take no directional bets on the benchmark, eked out a return of 1% in the nine months through September, compared with 6% for hedge funds overall. They recorded some $3.9 billion of outflows in the period, taking total assets to $66 billion, Eurekahedge data show.

“It looks nice -- the market’s up 20%, but it’s been a wild ride underneath the covers,” said Mark Connors, global head of risk advisory at Credit Suisse in New York. “The factor path has been unpredictable.”

Case in point: Last week saw the value strategy revive once more as hopes for a U.S.-China trade deal buoyed economic prospects, just weeks after a rotation in the opposite direction driven in part by recession fears.

To some, it’s a sign of late-cycle fragility as investors turn on every economic and political headline on a dime. But there’s also a whiff of suspicion that choppy rotations have been exacerbated by deleveraging among systematic funds.

“Quants sometimes can be a canary in the coal mine,” said Melissa Brown, managing director of applied research at Qontigo GmbH, which provides tools for portfolio construction and risk analytics. “Maybe we are going to see going forward more volatility in style factors as funds need to deleverage or people pull their money.”

Some factors are becoming more sensitive to shifts in positioning. The strength of the recent rally in cheap cyclical shares, for instance, caught many by surprise given the lack of a fundamental catalyst, Bank of America Corp. strategists led by Derek Harris wrote in a note.

At Los Angeles Capital Management, while cheap relative valuations are starting to push portfolios toward value shares, its models still favor more expensive growth stocks because the fund expects global economic growth to remain weak.

“We are in a choppier environment,” said chief investment officer Hal Reynolds at the firm overseeing $25 billion including absolute-return strategies. “Compression in returns and pick-up in risk have both occurred this year, leading to the reduction in risk budgets.”

Relative to their market-neutral quant peers, other hedge funds appear to have turned more bullish. Macro funds and commodity trading advisors, which mostly trade index futures rather than individual stocks, have expanded their long bets this month, Credit Suisse data show.

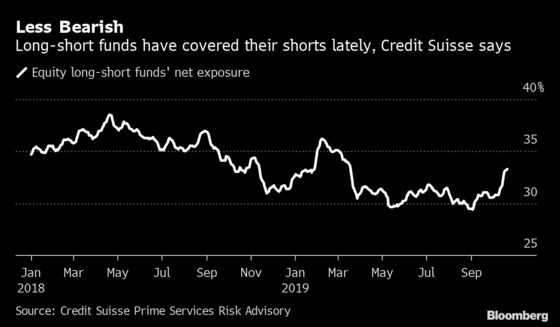

Meanwhile, long-short stock pickers have boosted net exposure to the highest since March as they covered short positions amid the surprise resurgence this month of trades betting on higher inflation and growth. Financial stocks have outperformed, while defensive sectors from consumer staples to utilities have lost money -- a reversal of market trends seen earlier this year.

Still, the very fact that these funds haven’t added longs aggressively underscores the persistent caution stalking the 2019 rally.

“The short didn’t work, so you reduce it -- but don’t commit your capital to going long something that may be just a short-lived rotation,” said Credit Suisse’s Connors. “They don’t see a reflation trade there.”

--With assistance from Ksenia Galouchko and Cecile Gutscher.

To contact the reporter on this story: Justina Lee in London at jlee1489@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma

©2019 Bloomberg L.P.