Quants Claim It’s Their Time to Shine in the Bond Market

Quants Claim It’s Their Time to Shine in the Bond Market

(Bloomberg Opinion) -- The quants are coming for the bond kings.

In recent years, quantitative finance has reshaped equity-market investing, with trend-following strategies and risk-parity funds becoming such a force that they’re often seen as responsible for violent swings in stocks. Fixed income, on the other hand, has largely resisted the idea of using technology and models to automate bond buying, instead favoring the traditional model of leaving it to fund managers to decide how to beat their benchmarks.

That’s starting to change, thanks to a growing number of exchange-traded bond funds that pride themselves on “factor investing” or “smart beta” strategies. The rationale is compelling: Not all debt with the same credit rating is equal. Not all debt in the same sector is equal. Not all debt trading at a discount is equal. Quants say they can use historical return patterns to determine which securities are best for broad strategies like “quality” and “value.” It’s up to the machine, not the fund manager.

For the bond market, which seems to coronate a new king every year or two, that’s quite a different approach. But quant-oriented funds are emerging just as investors are looking for ways to be smarter about their fixed-income allocations. For one, the Federal Reserve’s path is no longer as clear, with policy makers poised to hold off on further interest-rate increases for now. Investors are also anxious about rising corporate leverage and the risk that some large borrowers could falter under the weight of their debt burdens. And as the final months of 2018 showed, when individuals want to get out of high-yield bonds and leveraged loans, prices can tumble in a hurry.

Rob Waldner, head of multisector for Invesco Fixed Income, is convinced factor investing is the path forward. The firm introduced a suite of fixed-income factor ETFs last year. Passive investing in bonds has one serious flaw, he said: Indexes are skewed toward the biggest borrowers. So if someone is concerned about the almost $300 billion in long-term debt between AT&T Inc. and Verizon Communications Inc., why buy a fund that tracks corporate credit broadly? As for those managers who think they can beat the market with an “unconstrained” fund, they may take outsized credit risk or severely reduce their interest-rate exposure, both of which create large downside risks. “Bad active” is no solution for the problems with passive, Waldner said.

That’s the pitch for factor investing. Now, here are the early results:

- BlackRock Inc.’s iShares Edge High Yield Defensive Bond ETF (ticker HYDB), which has a stated outcome of “high yield with potentially less risk,” fell 2.88 percent in 2018, compared with a decline of 2.6 percent for its benchmark. The iShares fixed-income balanced risk ETF (ticker FIBR) has also trailed its benchmark.

- Fidelity Investments released two fixed-income factor ETFs in mid-2018, one that invests in high yield (ticker FDHY) and another for low duration (ticker FLDR). The former has underperformed its benchmark since inception, while the latter has outperformed.

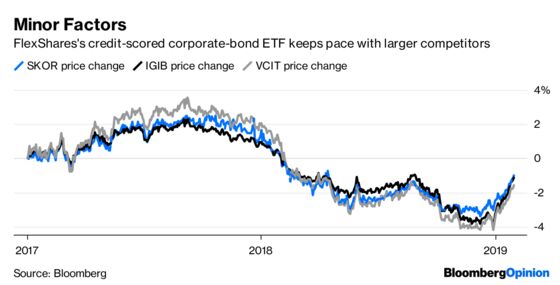

- FlexShares, which is managed by Northern Trust, has one of the longer-running fixed-income factor ETFs. The FlexShares Credit-Scored U.S. Corporate Bond Index ETF (ticker SKOR), which traces its roots to November 2014, has returned an average of 2 percent annually since inception, compared with 2.2 percent for its benchmark.

All told, it remains to be seen whether these types of strategies will deliver superior performance over a longer period. They’re still a small subset of the broader fixed-income universe and trade accordingly. Invesco’s investment-grade value ETF (ticker IIGV), which has $6.2 million in assets, still goes days without seeing any volume, according to Bloomberg data. BlackRock’s FIBR is the biggest of its five offerings, at about $121 million. FlexShares’s SKOR has about $96 million in assets.

By contrast, quant hedge fund assets as a whole totaled $967 billion as of June 2018, according to Hedge Fund Research. While that includes a range of strategies deemed quantitative, it’s clear that factor-based investing is likely to take some time to catch on in fixed income.

Michael Hunstad, Northern Trust Asset Management’s head of quantitative strategies, is undeterred. “We focus too much on returns and not risk-adjusted returns,” he said in an interview. “It’s really about picking out those risks that are compensated versus risks that are not compensated.” Indeed, SKOR compares favorably with big corporate-bond ETFs in terms of its Sharpe ratio, downside risk and standard deviation.

One good thing about factor-based investing is there are at least controls in place to prevent the fund from straying too far from its goals. “All the research suggests that you should be neutral to your benchmark in terms of sector exposure,” Hunstad said. If asset managers at Goldman Sachs can barely deliver positive returns over five years, maybe that’s a sign that go-anywhere funds aren’t the future of fixed-income.

For now, interest in factor investing seems to be stronger than actual adoption. Maybe it’ll just take more marketing. Maybe it’ll take a shock to passive investments to encourage individuals to look for an alternative. Maybe quants will never truly catch on in the vast and highly fragmented world of bonds, and the skeptics who claimed the strategy “is not a free lunch” will be vindicated.

I tend to think there’s ample room for innovation and experimentation within fixed-income investing. That’s not to say quants will turn out to be smarter than the market, but they’re welcome to give it a shot.

I amguilty of this as well,though here's the most recent offense.

The fund's fact sheet lists a Fidelity low-duration factor index as the benchmark. For my comparison, I used the "secondary benchmark," the Bloomberg Barclays U.S. Floating Rate Note < 5 Years Index.

Compared with the $31 billion LQD fund and the $20.9 billion VCIT fund.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.