Quants Are Netting Record Gains in Treasury Rally. It Can’t Last

Quants Are Netting Record Gains in Treasury Rally. It Can’t Last

(Bloomberg) -- Fast-money quants have scaled record heights riding the bond rally this year. Now they’re in danger of falling back down to Earth.

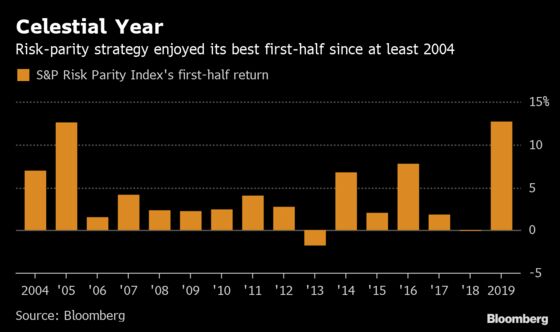

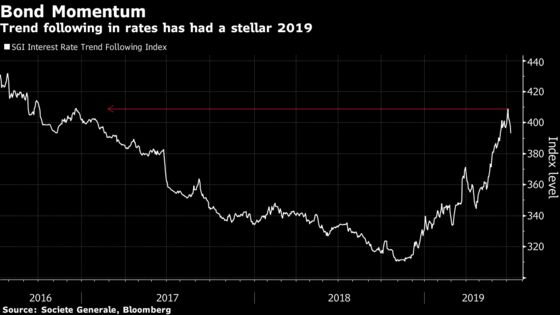

Risk-parity funds are off to their best start since at least 2004 after ramping up exposure to government debt and levering up, while trend followers in interest rates just notched the strongest half-year in nearly three decades.

But the pile-on in Treasuries has left quantitative and discretionary investors alike at the mercy of a bond market that can turn on a dime. Risk-parity funds are particularly vulnerable with their heavy weighting in fixed income.

“I don’t think risk-parity funds are likely to post higher performance going forward,” said Masanari Takada, a cross-asset quant strategist at Nomura Holdings Inc. “Government bond positions are already crowded and systematic trend-followers will be forced to exit if bond prices decline and volatility goes up.”

Trend followers, also known as Commodity Trading Advisors, take positions only after momentum appears in the price, while risk-parity funds aim to hold an equal amount of risk among investment classes. Both strategies have loaded up on bonds thanks to muted cross-asset volatility and surging prices.

Risk-parity players in particular have taken advantage of calm markets to boost their average leverage ratio to about 190% -- near historical norms -- from about 50% in January, according to Nomura.

AQR’s Risk Parity II MV Fund is up 15%, beating 93% of peers, in what Principal John Huss calls an “unusually good year” for the strategy.

But steep leverage could backfire if market swings increase, a risk investors of all stripes face. With Nomura predicting cross-asset jitters will likely rise going into the 2020 U.S. presidential election cycle, risk-parity funds could be forced to rapidly deleverage to maintain their target volatility levels.

AQR’s Huss, who oversees the $203 billion firm’s risk-parity strategies, says that while volatility is below average across most asset classes, the swings in developed-market equities and commodities aren’t too far below historical levels.

“Not every asset class has unusually low volatility levels,” he said by phone. “As a result, our position sizes are larger than they would be in a higher risk environment but not necessarily as large as you might guess.”

Trend followers in rates have already experienced a dip in performance of late, slipping 1.5% in July. Momentum signals flashing green this year prompted CTAs to go all-in on government notes, with bond positions “sky-rocketing,” according to Lyxor Asset Management.

The firm now suggests investors “take some profits and rebalance towards strategies that are positioned for a rise in bond yields,” strategists led by Philippe Ferreira wrote in a note.

For quants like PanAgora Asset Management’s Bryan Belton, the possibility of a large slide in bond prices is actually an argument for strategies like risk parity that eschew the traditional 60-40 portfolio weighting scheme.

“When everything goes up, diversification is less important,’’ said the director at PanAgora, the professional home of Edward Qian, who coined the term for the investing style. “It is when one of the asset classes experiences a large drawdown that diversification becomes more important.’’

To contact the reporters on this story: Ksenia Galouchko in London at kgalouchko1@bloomberg.net;Justina Lee in London at jlee1489@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Yakob Peterseil, Sid Verma

©2019 Bloomberg L.P.