Quant Strategy Once Powering Bull Market Is Set for Comeback

Quant Strategy Once Powering Bull Market Looks Set for Comeback

(Bloomberg) -- The U.S. stock rally can boast a slew of feats, but breathing life into an investing strategy that once anchored this post-crisis bull market isn’t one of them.

Not yet, anyway.

The S&P 500 has enjoyed the best start to a year in at least three decades, gaining 13 weeks out of 17 on the march to an all-time high.

Yet for the once red-hot quantitative style known as momentum, which buys the past year’s winning shares and sells its laggards, it hasn’t been enough to trigger a rebound after the strategy was upended by the turmoil of late 2018.

The question is, when will relentless equity gains jump-start one of Wall Street’s most revered trades? For humans and robots alike, it’s a battle for the soul of this unloved market rally.

“It may take a few more months,” said Sean Phayre, the global head of quantitative investments at Aberdeen Standard Investments. These strategies need to “re-balance into the current high-momentum names and for those momentum names to then continue. That will be key,” he said.

Investors who chase trends are struggling, according to key metrics.

A market-neutral momentum portfolio compiled by Bloomberg has dropped 4 percent this year to trade near the lowest since 2017, compared with a 17 percent gain for the S&P 500. While the biggest exchange-traded fund tracking the style, ticker MTUM, has done better, it still lags the U.S. benchmark by five percentage points.

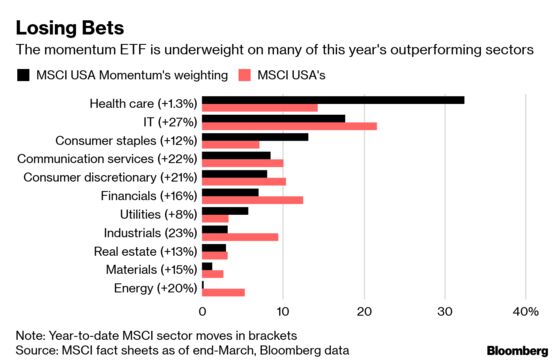

The issue is momentum is backward-looking by definition. Many such strategies bought defensive shares during the 2018 selloff because they were relative winners. Not only have portfolios yet to rebalance into this year’s market leaders, those defensive names have been tumbling down the performance league table as risk appetite has revived.

For instance, the MTUM ETF remains heavily exposed to health care companies and underweight on technology. Health care has been the worst-performing sector in 2019; tech has been the best.

Momentum “suffers from the initial sell-off of what has been doing well, and then it suffers from the bounce because of the subsequent reversal of that trend,” said Phayre.

Mo Problems

Until mid-2018, momentum was a star performer of the decade-long bull market for stocks.

When volatility was muted, monetary policy was accommodative and the tech darlings looked like they could do no wrong, the winners kept on winning. The main momentum ETF beat the U.S. equity benchmark by more than 30 percentage points in the five years through Tuesday.

As market trends reversed sharply and repeatedly, the factor started flailing. A market-neutral momentum portfolio’s three-month correlation with cyclical stocks has plunged to the lowest since 2016, according to Macro Risk Advisors. Cyclical shares have surged to near the highest versus defensives since 2004.

“Momentum is clearly an optimistic factor in the way that it considers that what is in place -- a trend, a phenomenon, a way of thinking -- should continue,” said Etienne Vincent, global head of quantitative portfolio management at BNP Paribas Asset Management. “The drawback of momentum is of course the fact that it’s subject to fashions and bubbles.”

The longer a trend holds, the more chance for a momentum rebound. Bloomberg’s version of the portfolio, representing a relatively simple approach, typically tracks the broader market with a lag of about two quarters. Four months into the U.S. stock rebound, that suggests a bounce could be coming soon.

Of course, in reality it’s more complicated, as any shifts in market leadership by definition will interfere with the factor’s performance. In January, industrial shares led the market rebound, but more recently technology and consumer discretionary stocks have set the pace.

Meanwhile, one of the most straight-forward momentum strategies -- buying the best performers and shorting the worst -- often crashes when markets rebound drastically after sliding, according to a 2016 paper from AQR Capital Management, a pioneer in using these styles.

That’s because the losing stocks -- the short side of the portfolio -- are likely to surge with the rebounding market, displaying higher beta than expected. The researchers reckon investors can improve risk-adjusted returns by tweaking the strategy’s weight based on expected portfolio volatility and performance.

And as with any other factor, construction matters. MTUM re-balances every six months, for instance. That reduces turnover but means it doesn’t capture the true winners, according to Cirrus Research LLC’s Pankaj Patel, the former head of quantitative research at Evercore ISI and Credit Suisse Group AG.

His own large-cap momentum index is an equal-weighted, long-short strategy re-balanced monthly, and gained nearly 17 percent in the first three months of the year.

At BNP Paribas Asset, momentum is measured based on prices and earnings revision, and exposures to beta, sectors and capitalization are neutralized, said Vincent. He says on that basis momentum is up 0.6 percent globally this year through March.

And the second-largest U.S. momentum ETF, Invesco DWA Momentum ETF, uses another proprietary methodology. It’s beaten the S&P 500 by 4 percentage points this year.

Bad Value

For many of the quant funds grappling with momentum’s recent performance, the problem has been exacerbated by the weak showing of the value factor.

In the past, momentum and value have moved in opposite directions, but both have been selling off in 2019. That’s not a good sign for factor portfolios on the whole, since many quants expect the two to hedge each other, according to Aberdeen’s Phayre.

Nor are the issues limited to the factor cohort. The challenge of riding such fickle markets is one reason trend-following quants known as commodity-trading advisers, or CTAs, have been bleeding cash over the past year.

It all adds up to a testing time for portfolios designed to capture the leaders and ditch the laggards in these complex markets. Fortunately, many of these strategies are designed to work over very long time frames, and managers expect periods of underperformance.

Meanwhile, thanks to the macro backdrop, including central bank moves to shore up growth and easing trade tensions, hopes remain that the tide will turn for momentum before long. Having closed at a new record on Tuesday, the S&P 500 edged lower Wednesday in New York trading.

“Momentum loves persistent trends in prices, either up or down, it dislikes trend-less volatility markets and it definitely hates sudden inflection points,” Andrzej Pioch, a fund manager at Legal & General Investment Management, wrote in an email. “We might be at a relatively more favorable environment for the momentum factor, in particular when more dovish Fed, no sign of excess inflation and more encouraging ‘noise’ around trade wars means that markets continue its climb higher.”

To contact the reporter on this story: Justina Lee in London at jlee1489@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Samuel Potter, Sid Verma

©2019 Bloomberg L.P.