Pioneers of Value Investing Are Trying to See If It’s Dead

Pioneers of Value Investing Are Trying to See If It’s Dead

(Bloomberg) -- Is the value factor dying? Even the finance legends who helped give birth to the quant strategy can’t tell for sure.

In their latest study, Eugene Fama and Ken French calculate that the investing style of buying stocks with depressed valuations has notched lower returns in recent decades.

But the academic duo who fueled the value boom with their groundbreaking research in 1992 can’t figure out if the systematic trade has in effect fizzled out. Its performance, or realized premium, has just been too volatile month by month.

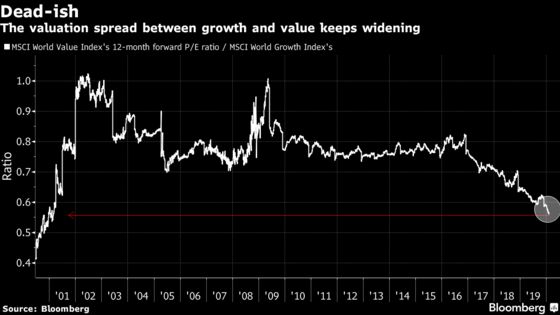

Their research helps to explain why managers in this corner of quantland are full of existential doubts. Value shares are underperforming yet again and near the cheapest versus growth counterparts since 2001.

In the U.S., the average monthly value return over a capitalization-weighted benchmark dropped to 0.11% between 1991 and 2019, as measured by their famed book-to-market value ratio, the authors calculate. That compares with a 0.42% premium harvested between 1963 and 1991, the timeframe for the original study.

“The initial tests confirm that realized value premiums fall from the first half of the sample to the second,” Fama at the University of Chicago and French at Dartmouth College wrote in the January paper. “But inferences from average premiums are clouded by the high volatility of monthly premiums.”

In other words, value’s worsening returns are effectively beyond dispute. But whether that represents an extended bout of misfortune or tells you something’s fundamentally broken remains the still unanswered question.

It’s a nuanced point. The authors just aren’t sure the returns in the second half of the sample period give them the statistical ammo to make firm conclusions. The good news: If you look at all the data since 1963, the strategy has valid foundations.

Getting Meta

The twist to the whole debate is that if the value strategy is dying, it may have been Fama-French who helped kill it.

Their landmark paper in the 90s concluded that differences in stock returns can be explained by the book-to-market ratio, in addition to capitalization, thereby spurring the boom in factor investing itself. Yet the fear among some quants and academics is that an investing rule will fail “out of sample” -- and that can happen if the strategy gets so popular it stops working, or if the theory was spurious in the first place.

Fama and French, who serve as consultants to quant firm Dimensional Fund Advisors, don’t seek to address these concerns head-on in this study. But their research suggests anyone seeking firm convictions will have a hard time of it.

Loyalists like AQR Capital Management LLC say a rebound is surely nigh given the factor’s solid academic backing, among other reasons. Critics reckon that macro-market forces are structurally capping returns for good.

It’s a big question. The original Fama-French framework says investors are compensated for bearing the higher risks inherent in apparently cheap shares -- and thus the premium should endure.

But the data makes it hard to elicit a clear conclusion either way because it’s so noisy. The debate over the vexed factor goes on.

To contact the reporter on this story: Justina Lee in London at jlee1489@bloomberg.net

To contact the editors responsible for this story: Sam Potter at spotter33@bloomberg.net, Sid Verma, Chris Nagi

©2020 Bloomberg L.P.