Quant Fund Shrinks 92% From 2018 Peak in Factor-Investing Crisis

Quant Fund Shrinks 92% From 2018 Peak in Factor-Investing Crisis

(Bloomberg) -- Like so many of his peers, Ian Heslop needs a turning point in markets to revive his misfiring quant strategies.

Yet for the Jupiter Fund Management investor, last week’s massive risk-on rotation only added insult to injury. As global markets cheered vaccine developments that point to a post-pandemic world, his Global Equity Absolute Return Fund fell the most ever -- cutting assets under management to just $1.3 billion.

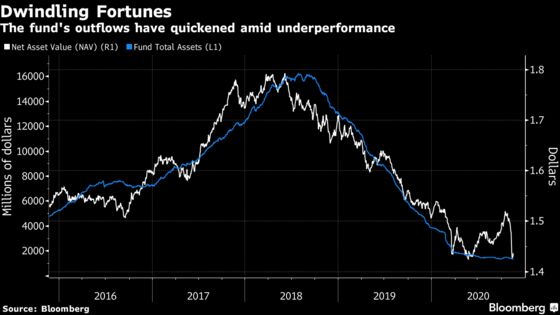

As recently as July 2018, it was a $16 billion powerhouse in the world of factor investing, popular with retail investors.

And the money manager has little confidence that there’s light at the end of tunnel.

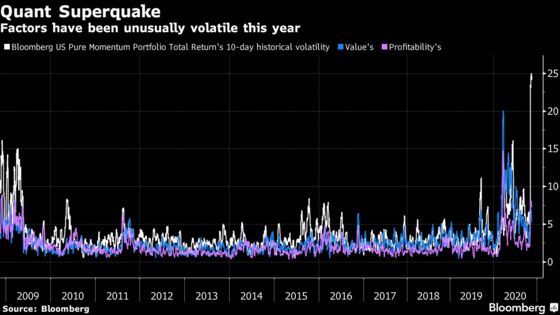

His style of systematic trading, which dissects stocks by factors like how cheap they look or how fast they’ve risen, is experiencing an unprecedented bout of volatility. Heslop says a herd of investors are plunging in and out of the most popular stock trades on Wall Street -- whipsawing rules-based fund managers like him along the way.

Originally launched at Old Mutual in 2009, the fund has seen its fortunes whipsawed against a backdrop of changing ownership.

The gyrations are “quite a difficult one to place in a coherent macro-environment argument,” the head of global systematic equities said in a telephone interview. “Rather than these being pure risk factors, they’re being driven by trading, and trading is necessarily something more difficult to forecast.”

His fund, which has both long and short bets, is down 4.8% this year in dollar terms -- set for its third straight year of losses. Its troubles are far from unique. AQR Capital Management on Tuesday announced it was shrinking its mutual fund lineup amid persistent outflows, while storied quant names from Renaissance Technologies and Two Sigma have stumbled of late.

Quants allocate money based on rules backed by decades of academic work which holds, for instance, that stocks with a low price-to-book ratio eventually outperform. But the worry is that these signals are misfiring as cash relentlessly chases the same trades.

In recent years, Big Tech has been the clear winner from this trend. But as an end to the pandemic appeared in sight last week, money rushed out of those megacap names and into more cyclical companies that benefit from an economic recovery.

For a fund like Heslop’s, the problem was that when stocks were rallying on the strength of Faang shares, it wasn’t betting big enough on them. When animal spirits roared back, its exposure to quality stocks -- which tend to underperform in risk-on climates -- lost money. And its tilt toward rising value stocks was too small to compensate.

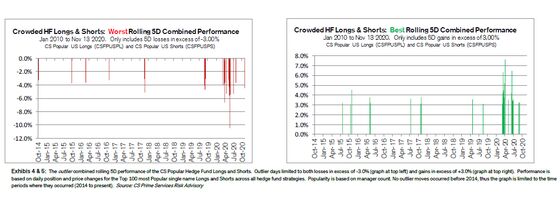

All this was amplified by investors moving in out and out of stocks en masse, in Heslop’s view. That’s backed by Credit Suisse Group AG’s data showing that among shares with crowded hedge-fund bets, 60% of all their unusually large moves over the past decade have occurred this year.

If herding continues to upend quant signals, the whole philosophy of picking stocks based on their fundamental characteristics could be in danger.

The good news: As Covid-19 fades, Heslop sees hope that factors could sway to their own beat again rather than being dominated by essentially unpredictable virus headlines. The rotation out of Faang stocks -- whose dominance has made it hard for active managers of all stripes to catch up -- is a start.

Still, the woes bedeviling stock quants began long before the first virus patient. One way the fund is addressing the crowding problem is by studying less common signals to give it an edge over exchange-traded products that use more generic inputs. Currently, its model is based on indicators such as analyst sentiment and sustainable growth.

“Our research is exploring areas where we can incorporate information that isn’t as well-traveled,” said Heslop, who holds a doctorate in chemistry.

It’s been quite the journey.

When the asset-management unit was spun off as Merian under private-equity ownership in late 2017, the product with its 20% performance fee was a $12 billion juggernaut accounting for roughly a third of the new company’s assets. By the time Merian was sold to Jupiter this February, the assets had fallen to around $3 billion thanks to underperformance and outflows.

Heslop hopes that fading virus risks will allow factors to trade like original quants once predicted. But even with progress on one vaccine candidate after another, that moment hasn’t arrived yet.

“There’s still a material concentration of risk above what we’ll normally see -- some of the factors are still correlated,” Heslop said.

©2020 Bloomberg L.P.