Quant Funds Hit By Misfiring Strategies

Quant Funds Hit By Misfiring Strategies

(Bloomberg) -- When it comes to slicing and dicing equities based on their factors, the strategy beloved by quants is exhibiting symptoms of sickness. The challenge is diagnosing how serious it is.

This month, Neuberger Berman will become the latest big name to close a fund based on factor investing, which uses characteristics like quality and value to bet which stocks will outperform over time. The decision follows a similar move by Columbia Threadneedle in December.

Other funds have been bleeding cash. The Man Numeric Market Neutral Alternative Fund for UCITS has shriveled to $20 million from around $300 million in mid-2018. Assets in the AQR Equity Market Neutral Fund have fallen nearly 50 percent to $1.1 billion.

It’s anecdotal, sure, but it’s adding up to an increasingly gloomy picture across the industry and re-energizing a debate about the effectiveness of such strategies. One of the most popular factors, momentum, has extended a miserable 2018 into this year. Value, another key style, has gone nowhere.

“If investors believe factor returns are well-behaved, they are mistaken,” said Vitali Kalesnik, head of equity research at Research Affiliates, a firm that runs such strategies and has also become a frequent public critic of them. “When investors need it the most, diversification may fade away and factors can go down together. This is exacerbated by the fact that they can go down several months in a row.”

And they have gone down. The AQR Equity Market Neutral Fund is on course for its sixth quarterly decline in a row, extending a 12 percent slump in 2018 -- the worst year since its inception. The Vanguard Market Neutral Fund has dropped 4 percent in 2019. The Merian Global Equity Absolute Return Fund, one of the largest in the space, is down 3 percent.

Divining the cause of all this is a big challenge given these complex, opaque pools of money, and some of the funds in question are modest in size. But for critics, there’s a pattern of factor investing delivering less than it promises.

In a February paper from Research Affiliates titled “Alice’s Adventures in Factorland,” authors including Kalesnik and Rob Arnott pointed out that not a single popular factor has provided statistically significant excess returns since 2003.

The paper noted this could be down to sheer bad luck since the benchmark for U.S. stocks did so exceptionally well in the period. But Arnott and his colleagues also wrote that investors may be disappointed as factors get too crowded, trading costs eat into returns and data mining exaggerates expected performance. The team, who are pioneers of smart beta and say they still believe in it, stress caution is warranted.

One big problem of late has been a diversification fail. Sanford C Bernstein Ltd. reckons the co-movement between factors recently reached the highest level in at least two decades, implying a change in the structure of the market that makes it harder for quants to generate idiosyncratic returns.

Momentum is down 3 percent this year, while value has posted a small decline after 2018 delivered the worst annual loss since at least 2000, according to portfolios compiled by Bloomberg.

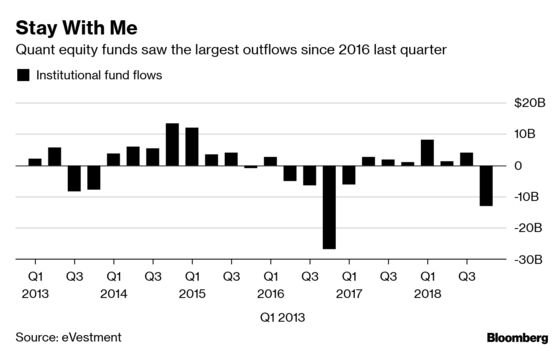

All this may help explain why the fourth quarter was the industry’s worst for institutional fund outflows in two years, according to eVestment data. Equity quants on Credit Suisse’s prime services platform saw gross exposure fall 19 percent in the second half of last year.

Still, those eye-catching stats came alongside big losses in the wider market. It’s late in the global expansion, and investors have been ditching stocks seemingly across the board. Institutions redeemed $748 billion from equity funds in 2018, according to eVestment.

Nor is it only equity factor funds that have suffered. A Goldman Sachs multi-asset risk premia portfolio saw its assets plunge to below $3 million from about $50 million over six months. GAM Holding AG was forced to write down a quant unit whose funds posted steep losses in 2018. Hedge fund Winton Group saw assets plunge by about $5 billion last year, part of the turmoil engulfing trend-following quants known as Commodity Trading Advisors.

Test of Time

At their peak, the Neuberger Berman and Threadneedle funds oversaw about $100 million and $40 million respectively, according to Bloomberg data.

A spokesman for Neuberger Berman said it’s closing its fund as the small size has made it hard to pursue its strategy, while a representative at Threadneedle also attributed its decision to the size of the fund, alongside limited demand. Both firms emphasized their commitment to alternative risk premia strategies.

For factor proponents, it’s all serving to test the courage of their convictions -- possibly for years to come.

“You can’t win in active factors if you don’t have horizon and you’re so worried about relative performance,” said Wes Gray, chief executive officer of Alpha Architect LLC. “The reality is if you’re doing factors as espoused in academic research we already know ex-ante that they have many many periods of five- or 10-year underperformance.”

Viewed through that lens, the performance in 2018 should be no cause for concern. Factor investing enjoyed a multi-year boom in popularity before the recent whipsawing markets wrecked popular strategies such as momentum.

“Depending how adaptive your momentum factor is, it may take a while for momentum performance to be reflected again,” said Georg Elsaesser, a quantitative fund manager at Invesco Asset Management in Frankfurt. While momentum can fare well in both bullish and bearish regimes, it requires steady market conditions, he said.

There are reasons for optimism. Some riskier factor styles such as volatility, leverage and small size have fared better as animal spirits revived amid signs the Federal Reserve will pause tightening. Equity quants saw their exposure jump by around 9 percent in January and February in concert with the broad stock rally, Credit Suisse’s platform shows.

Meanwhile, smart beta (which tracks factors typically through long-only investments) remained in demand in the exchange-traded funds market, drawing a record $33 billion of inflows last quarter led by value and low-volatility, Bloomberg Intelligence data show.

A spokeswoman at Vanguard said its fund’s performance was affected by value stocks and geopolitical uncertainty, while AQR referred to an earlier defense of factor investing by founder Cliff Asness.

A spokeswoman at Man Group declined to comment, while a representative Goldman Sachs didn’t respond to a request for comment. A spokeswoman at Merian Global Investors said that weak performance across the industry is “not outside of expectations,” and likely due to changes in monetary policy. The firm pointed to the diversification offered by its fund.

Quant Quake

Doubts and redemptions in quant land are as old as they come. Erik Rubingh, a fund manager at BMO Global Asset Management, recalls after the so-called Quant Quake in 2007, money managers changed the names of quantitative teams a few times until they became trendy again.

After a relatively benign 2 percent loss in 2018, Rubingh’s own BMO Global Equity Market Neutral V10 Fund is down 12 percent this year. In a mid-February report, he noted that returns in the year following a drawdown tend to be strong.

“I don’t think institutions have given up on quant investing or factor investing, but now we have some question marks,” said Tayfun Icten, an analyst at Morningstar in Chicago. “So the firms that have an operational edge and more sophisticated infrastructure to execute will probably do better than wannabes.”

--With assistance from Dani Burger.

To contact the reporter on this story: Justina Lee in London at jlee1489@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma

©2019 Bloomberg L.P.