Is Value Dead? Debate Rages Among Quant Greats From Fama to AQR

Quant Fight 2020: Inside Wall Street’s Big Argument on Value

(Bloomberg) -- Is value dead? One of the most heated debates in quant finance is in the spotlight like never before.

After the factor’s worst quarter this century in the coronavirus crash, Wall Street players are butting heads on what comes next for the famed investing style that scoops up stocks that look alluringly cheap.

After kicking off the factor boom in the early 90s, value is punishing the faithful three decades on. Billions are getting wiped out, quant shops are shrinking, and even its architects Eugene Fama and Kenneth French can’t quite figure out if the strategy’s alive or dead.

Unbowed, Cliff Asness at AQR Capital Management LLC and Rob Arnott at Research Affiliates LLC are leading a storied cohort defending the factor’s core foundations with fresh data and research -- while detractors attack in kind.

As hopes abound for a value comeback, the debate is frazzling the smartest minds in this corner of systematic finance.

Critics point to the worst recession since the Great Depression as the final nail in more than a decade of value underperformance relative to a strategy of buying stocks that tend to grow faster than the market norm. Banks and oil drillers that make up value portfolios look permanently screwed -- while a winner-takes-all economy dominated by Big Tech means a growth stock like Facebook Inc. can get pricier still.

Value loyalists cite decades of rigorous academic research, with extreme valuation gaps boosting their confidence that a comeback is nigh. Consider last week when value posted its biggest two-day jump since at least 2002, or amid Wednesday trading as a rush of optimism buoys the factor. Yet even within this community of believers, there’s deep controversy on how to find the premium and whether to time the market.

Drawing on recent research on both sides of the argument from Man Numeric to Dimensional Fund Advisors, here’s a guide to the most tortured debate in quantland.

1. Do stocks that look cheap relative to metrics like earnings actually outperform in the long run?

Yes:

Let’s start off with the basics. The value factor was made famous by the Fama-French model that kickstarted the factor revolution. With evidence documented by multiple academic luminaries across global markets and various periods, the quant consensus has largely been in favor of the factor up until the past decade.

For good reason. “Buy low, sell high” has a famously intuitive appeal to discretionary stock pickers like Warren Buffett. Similarly, in the factor community the risk-based rationale posits that value shares compensate their holders for the higher risks. Meanwhile the behavioral theory is that these shares are undervalued by investors blinded by the glamor of growth stocks such as Facebook.

But in a reflection of the growing disquiet among their acolytes, even Fama and French couldn’t offer much solace when they revisited the topic this year. While the duo conceded that the factor’s returns have plunged since the 1990s, they conclude that the data is too volatile to determine if the expected premium has vanished.

Not exactly:

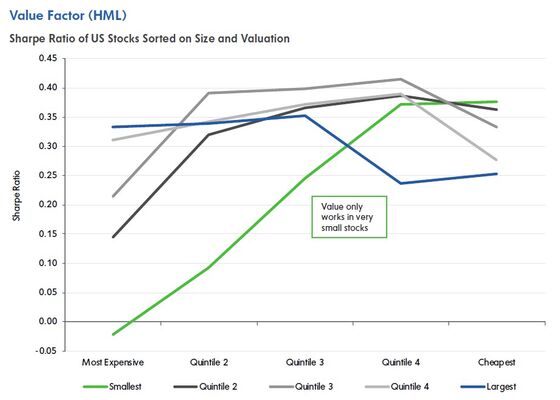

Rob Croce at Mellon Investments argues that value has never actually delivered across the large-cap stocks traded by major funds.

It outperforms within small caps, yet that segment isn’t large enough to accommodate the current size of factor portfolios. That means value might look good in academic studies but has been “misappropriated by practitioners to sell ‘smart beta’ value products,” he wrote in a May paper, referring to the boom in mass-market factor funds.

2. Have structural economic changes broken it?

Yes:

Technological advances have made a slew of stocks structural winners and losers in an age of rising market concentration. Consider the companies reaping gains from the pandemic: Netflix Inc. and Amazon.com Inc. Growth stocks like these -- the opposite of value -- have forged large networks that justify their rich valuations in the digital economy.

No:

Value’s defenders would advise against extrapolating from a few years of data. O’Shaughnessy Asset Management suggests that value tends to underperform during technological revolutions, but revive when those innovations mature. The crash of the dot-com bubble ushered in some of the best years for the value strategy. This time won’t be any different.

To AQR’s Asness, regardless of tech leaps, as long as there are wide valuation spreads, investors are probably too optimistic about growth and too down on value. In his analysis, even if you take out the mega caps or tech cohort, value is still near the cheapest it’s ever been versus growth, so it’s unlikely that the gap is being driven by the dominance of tech names.

3. Is the factor stuffed with broken businesses?

Yes:

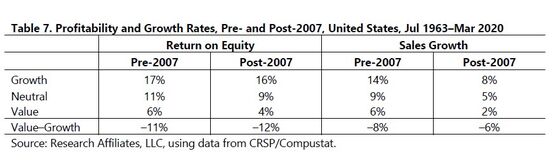

This concern lines up with post-crisis economic trends that are now being exacerbated by the pandemic. In a paper with University of Calgary’s Anup Srivastava, New York University professor Baruch Lev argues that as consumer demand and bank lending slumped after the 2008 recession, value shares have been unable to rebuild and innovate.

No:

AQR’s analysis shows that the gap in profitability and return on assets between value and growth stocks isn’t much wider than usual. That suggests fundamentals are far from driving value’s losing streak. Investors are simply paying less attention to them. Rob Arnott’s Research Affiliates LLC comes to a similar conclusion.

4. Is the rise of intangible assets the problem?

Yes:

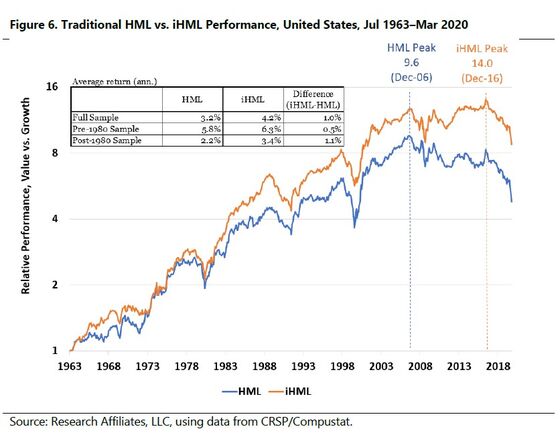

According to NYU’s Lev, the problem with value is that traditional metrics -- especially the price-to-book ratio used by Fama-French -- are broken. Outdated accounting rules consider spending on intangibles like patent research expenses rather than investments, making growth stocks seem pricier than they actually are. That’s a problem when companies are increasingly putting their money in people and research rather than factories.

Lev finds that capitalizing intangibles as actual assets -- an adjustment that affects earnings as well as book values -- would have pushed some growth stocks into the value category. And that would have yielded a much more profitable strategy for the latter from the 1980s onward.

In a way, this is a pro-value argument. It implies the premium still exists -- quants were just capturing it wrongly.

Still, the paper shows even returns on the adjusted value strategy dropped over the past decade, suggesting accounting is far from the main drag on returns.

No:

Dimensional Fund Advisors -- a value diehard that counts Fama and French among its advisers -- finds that capitalizing intangibles made little difference to return spreads in data starting from 1963.

5. Are persistently low interest rates the cause of value’s slow death?

Yes:

Cheap stocks tend to be cheap because their profits are often more tethered to the business cycle -- think Exxon Mobil Corp. rather than Alphabet Inc. As such they tend to fare poorly when rates are low because the economic outlook is weak. More directly a lower discount rate makes short-term cash flows -- something value tends to offer -- less valuable versus long-term ones. And that’s by definition better for growth companies since they tend to reliably provide cash flows over the long haul.

All that means value is, as Man Numeric puts it, a “pseudo-short duration strategy.”

The last decade has seen an increasingly positive relationship between the returns of U.S. Treasuries and growth stocks, and the opposite dynamic for value, the paper finds. While it can still recover, low rates aren’t a great backdrop for the value strategy, the research concludes.

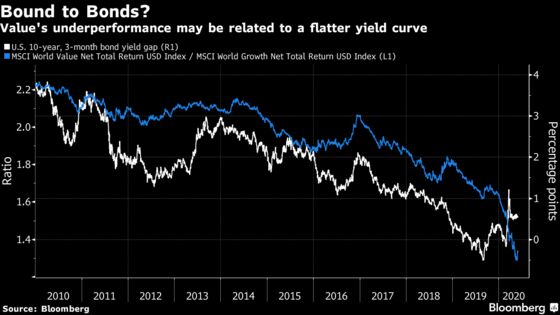

Another version of this explanation is that value has suffered owing to a flattening yield curve, or lower gap between long- and short-term rates. As Nomura Instinet strategist Joseph Mezrich argues, value companies have been relying more on short-term debt financing relative to growth names since the 2008 crisis. A flattening yield curve is therefore more of a benefit for growth companies terming out their debt.

No:

A new AQR paper calls that putative relationship between rates and value “suspect” based on the fact that it varies greatly depending on the period, markets and measurements studied. The strongest result they find is one between the yield curve and value returns, but even that link doesn’t explain much.

6. Is value doomed by the boom in passive index investing?

Yes:

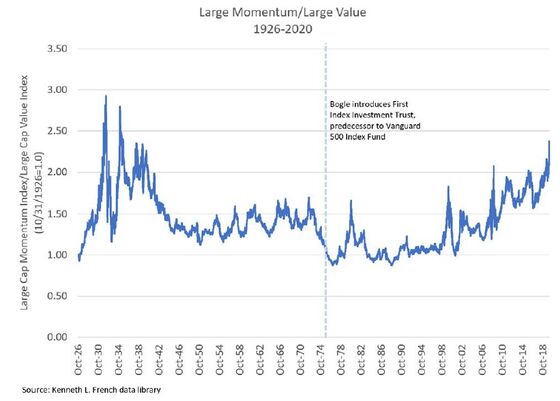

To Michael Green at Logica Funds, the boom in exchange-traded funds is partly why momentum -- a strategy of buying and selling stocks based on their recent performance -- has increasingly outperformed value since the mid-90s. Funds tracking capitalization-weighted indexes are inherently anti-value and pro-momentum, since they have to mechanically put more money into rising stocks.

Securities struggle to re-price without these funds buying them, so as long as index players are luring fresh cash, it’s hard to see valuation spreads closing.

No:

On Twitter, AQR’s Asness responded by saying value doesn’t necessarily need valuation spreads to narrow, since it’s a bet on undervalued future cash flows. Sanford C. Bernstein’s quant strategists have also noted in their research on value last year that the factor has staged brief rallies in the past -- even as cash kept rushing into index funds, suggesting this issue isn’t the factor’s bane.

7. Can you actually tell me when to rotate to value?

Yes, up to a point:

There is now a strong case for value’s comeback after its worst drawdown in history by some measures. MFS Investment says factors tend to revert to their average returns in the long run. SEI Investments’ Eugene Barbaneagra writes in a recent paper, “the relationship between a firm’s cash flow and stock price should not vary by large degrees for long periods of time.”

Even AQR added a tilt toward value last year in what Asness dubbed a “venial sin” of market timing.

But just because a factor rotation looks likely doesn’t mean quants can time it effectively, especially after trading costs are taken into account. Dimensional Fund Advisors says that while wide valuation spreads tend to augur stronger returns, timing a value strategy based on that doesn’t beat a simple buy-and-hold strategy.

No:

In a rebuttal to value’s defenders, Logica’s Green points out that wide valuation spreads haven’t always led to strong absolute returns for the factor. And on an absolute basis, it isn’t particularly cheap.

The upshot? To value diehards, all the hate, skepticism and outflows mean the factor won’t be arbitraged away anytime soon. So no pain, no gain.

As long as you survive long enough.

©2020 Bloomberg L.P.