Quant Blame Game Over Stock Sell-Off Pits Nomura Against Nomura

Quant Blame Game Over Stock Sell-Off Pits Nomura Against Nomura

(Bloomberg) -- After Nomura apportioned blame for Tuesday’s dramatic stock plunge on trend-following quants, an unlikely defender has emerged for the systematic hedge funds: Nomura.

In the quest to uncover the culprit behind the S&P 500’s 3.2 percent rout, the investment bank has emerged conflicted over the role of computer-driven traders that surf the market’s momentum.

The schism hinges on differences in how strategists there calculate the way programmatic traders reacted to shifts in sentiment this week -- and the buy and sell orders seen along the way. Figuring out their next moves could be crucial in prepping for the next downleg -- depending on whose quant story you buy into.

Their esoteric investing style and billions in equity holdings that can be liquidated en masse once again finds trend-chasers at the center of market intrigue. In the past, it’s pit AQR Capital Management against the likes of JPMorgan Chase & Co.

At Nomura right now, it’s in-house. The first shot came from Charlie McElligott on the equity-derivatives sales team in New York. His quant model, which reverse-engineers returns, has obtained something of a cult-following on Wall Street -- flashing out sell signals during especially tumultuous days.

On Tuesday, he argued commodity trading advisers, or CTAs, hammered markets to the downside as a three-month measure of S&P 500 momentum turned negative.

Less than 24 hours later, his Tokyo-based colleague with the research team, Masanari Takada, told clients CTAs couldn’t possibly serve as the whipping boy -- having pared their bullish positions in the earlier autumn swoon.

“On our research side, the CTA model did not show any selling signal beforehand, and CTAs were forced to follow the market decline somewhat,” Takada said by email.

His model suggests coming into this week, CTAs had a modest overweight position that fell in sympathy with the broader market on Tuesday -- the worst day since the Brexit referendum for the S&P following a 1 percent gain.

Differences in published opinion within investment banks are common given the complexity of high-octane markets.

Max Long, Max Short

McElligott reckons these leveraged funds were bullish to the max -- adding $42 billion of fresh exposure thanks to Monday’s rally, which was spurred by expectations the G-20 had secured a thawing in Sino-U.S. trade tensions.

Those longs were then abruptly whittled down to a fifth the following day -- helping to whipsaw U.S. stock markets in the process, according to the strategist.

“Due to the choppiness and volatility profile year-to-date, you’ve had a really tight band -- basically 100 points -- that in two days of trading can go from max long to max short,” McElligott said by telephone. “CTAs’ impact, and potentially their part in the overall market, is larger than usual because fundamental managers have been so crushed by performance and grossed down.”

The emerging consensus, however, favors Takada’s analysis.

With CTAs following the ebbs and flows of the broader market and offloading with rising volatility, the tumultuous trading over the past two months suggest they had largely reduced their bullish holdings -- leaving them with little firepower to exacerbate the latest downdraft, according to Wall Street strategists.

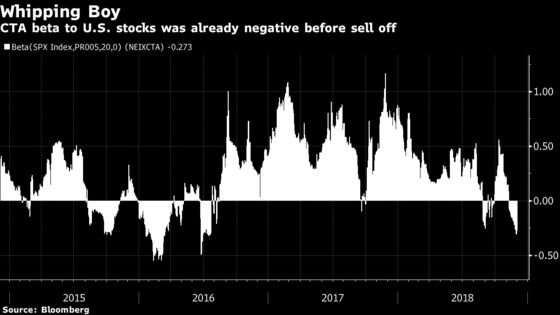

One way market participants judge the average exposure of trend-followers is through a measure called beta, or the portion of their returns attributable to the benchmark. In that view, the majority of the selling had already occurred in early November.

Wells Fargo and Societe General SA, for example, estimate the cohort had a neutral to slightly short position going into Tuesday. Neither models reflect a forced fire-sale of $50 billion in notional exposure that McElligott points to.

“We are highly skeptical of such claims,” Pravit Chintawongvanich, equity derivatives strategist at Wells Fargo Securities, wrote Tuesday, without mentioning Nomura calculations specifically. “CTAs in aggregate do not operate on a single ‘trigger point.”’

JPMorgan Chase & Co., for its part, sympathizes with the view that short-term momentum inputs tracked by CTAs encouraged them to offload -- with a three-month signal flipping to negative on Tuesday. Crucially, however, long-term metrics remain relatively positive, according to Nikolaos Panigirtzoglou, a global strategist at the U.S. bank.

“Assuming that in aggregate, CTAs look at both short and long momentum signals, we conclude that any short base on S&P 500 futures contracts by CTAs is likely to be small at the moment,” he said via email.

--With assistance from Luke Kawa.

To contact the reporter on this story: Dani Burger in London at dburger7@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma, Cecile Gutscher

©2018 Bloomberg L.P.