QE-Versus-Recession Battle Will Seal Stocks’ Fate, Top CIO Says

QE-Versus-Recession Battle Will Seal Stocks’ Fate, Top CIO Says

(Bloomberg) -- A tug of war between recession fears and faith in central banks’ ability to keep asset prices aloft could end in a dramatic showdown -- and a top-performing Canadian fund manager is preparing for either eventuality.

Recent profit warnings by bellwethers like German chemical maker BASF SE and U.S. freight shipper CSX Corp. are heightening fears of an economic slump, while a dovish turn by central banks is underpinning expectations that accommodative policies will remain in place.

“So what do you as an investor?” said Paul Moroz, chief investment officer at Mawer Investment Management Ltd., which manages C$59.5 billion ($45.3 billion). “You’ve got to be pretty flexible to recognize this could go either way.”

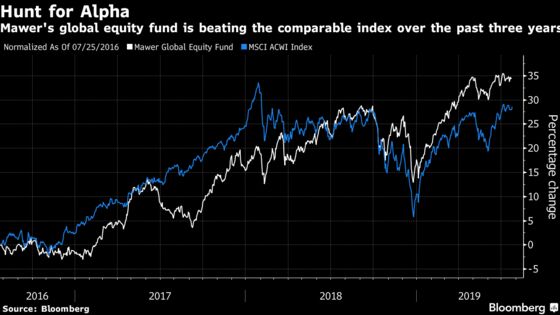

Mawer’s New Canada Fund, which is now closed to new investors, has returned 322% over the past 10 years, the best-performing Canadian equity-focused mutual fund with more than C$1 billion in assets, according to data compiled by Bloomberg. Among Canadian-based funds with C$500 million or more in assets, the firm’s international equity fund is the top performer in its class over the past decade and its global equity fund is the ninth-best in the past five years.

Given the opposing tensions, determining the right discount rate for valuing stocks is proving challenging, Moroz said. Investors could reasonably add 1 percentage point on recession fears or subtract 1 percentage point on the belief that central bank support will inoculate stocks from any turbulence ahead, Moroz, 39, said.

Valuation Canyon

That 2 percentage point difference multiplied by an equity duration -- a measure of stocks’ sensitivity to their discount rate -- of 20%, amounts to a 40% “canyon” in the present-day value of securities, he said in an interview at Mawer’s headquarters in Calgary.

Among stocks Moroz is betting may be resilient in either scenario is French luxury-goods maker LVMH, which he sees as well-managed with “wonderful” brands that could continue raising prices even during a recession.

“Earnings may hold in there because of their clientele, and they still may have pricing power, and it’s a stock that may benefit from ultra low rates,” Moroz said. “We’re trying to play that great divide, that canyon between those two scenarios.”

Microsoft Corp. could continue to grow in the years ahead as it benefits from a structural shift toward cloud-computing, Moroz said. The shares have climbed to a record after sales and profit beat estimates last week.

Companies without recurring revenue or that are dependent on other businesses’ capital spending may be particularly susceptible to declines, he said. That includes railroads, chemicals and even autos, all of which already are getting hit, he said.

Top holdings in the New Canada Fund include Solium Capital Inc., Boyd Group Income Fund and MTY Food Group Inc.

Here are Moroz’s other thoughts on economics and investing.

Negative Rates in Canada?

Canada could “absolutely” see negative rates if the current softness in company and manufacturing data turns into a full-blown recession. That would likely send investors fleeing into bonds and prompt North American central banks to cut rates, he said. The Bank of Canada would get “locked into the interest rate tractor beam” and have to cut rates so the loonie doesn’t get too strong.

“You need an earnings recession. You need people to get scared of the stock market because what would drive it is both government policy and investors having no other alternative.”

The yield on the Canadian 10-year bond already is at 1.5%, near the lowest in about two years.

India Versus China

“From a company perspective, I would bet on India ahead of China. There’s a number of talented entrepreneurs and a real entrepreneurial culture in India, and I think there will be some marvelous investment opportunities there over time. There will be in China too, but I think that there’s just so much more control in China, and culturally I don’t think it has the same ingredients that facilitate capitalism and wealth creation.”

Moroz sees large Chinese companies like Tencent Holdings Ltd. and Alibaba Group Holding Ltd. as “test cases” for how the government will influence large domestic corporations and use them for its own policies and desires.

Passive Versus Active

Even as passive, index investing grows, active managers still are needed to “keep the market honest” and help investors dodge risks that come from indexes “doing terribly silly things.” While the spread of passive funds makes it even more important for active managers to beat their benchmarks, it also may give surviving active funds an advantage as more of their rivals close up shop.

“On one side, there’s alpha or death. On the other side, the opportunity might be even more significant.”

“There’s a possibility we might already be seeing effects of less competition. Or we might just be lucky.”

To contact the reporter on this story: Kevin Orland in Calgary at korland@bloomberg.net

To contact the editors responsible for this story: David Scanlan at dscanlan@bloomberg.net, Jacqueline Thorpe

©2019 Bloomberg L.P.