QE Is Back in Europe. These Charts Show the Bond Market Winners

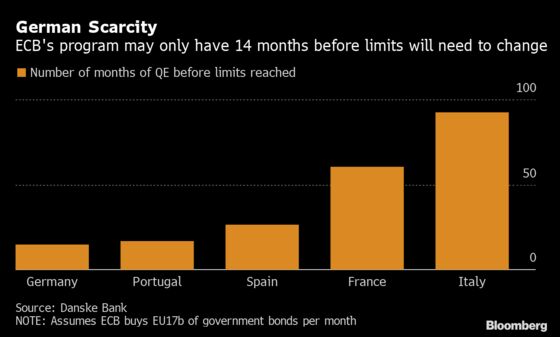

Strategists are modeling just how long the ECB can buy bonds for under its current self-imposed limits.

(Bloomberg) -- The European Central Bank is starting to pump billions into bonds again, stimulus that may further warp markets after its previous efforts drove yields down to record lows.

At a pace of 20 billion euros ($22 billion) per month from Wednesday, the ECB’s latest asset-purchase program is likely to favor some markets over others. Investors and governments in the region’s most indebted nations -- such as Italy and France -- are set to be the biggest beneficiaries, simply because they have the most bonds left for the central bank to buy.

Given that the ECB has already sucked up 2.6 trillion euros of bonds, funds may have to scrabble to pick up what’s left after the fresh buying. Yields on two-thirds of the region’s government debt are already below zero, meaning investors will have to believe bonds are set to rally further, or they will be left with negative returns.

“The force bearing down on yields is not cyclical, it’s structural,” said Richard McGuire, head of rates strategy at Rabobank International. “Financial repression is going to become an increasingly powerful force.”

Strategists are modeling just how long the ECB can buy bonds for under its current self-imposed limits, designed to prevent the institution having undue influence over national governments. The central bank has 14 months before it hits the 33% threshold for Germany’s sovereign debt, but in countries such as Italy there is much more headway, according to Danske Bank A/S.

In smaller nations, such as Finland, Rabobank calculates that the ECB buying may only be able to continue until the middle of next year. That would mean it has to buy other assets or alter the parameters of the program, which has already stirred unprecedented divisions among policy makers. Either of those options would lift bond prices.

The ECB must also buy debt in proportion to the size of each nation’s economy and its population. But these limits have proved to be less binding, with the institution willing to diverge from them and buy above the so-called capital key when it comes up against a shortage of available securities.

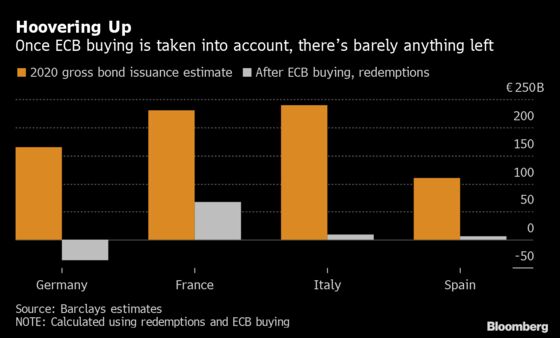

That has worked to the benefit of Italy and France, which are the two nations with the largest stock of debt in the euro area. Unless there are signs of a boost in bond supply -- through governments borrowing more -- this is unlikely to change soon.

Indeed, once the biggest buyer in the market has finished, there’s barely anything left for others to buy, creating a scarcity that ramps up bond prices. Once the ECB is taken into account, and investors reinvest proceeds from maturing bonds, Germany’s fresh issuance is completely soaked up, according to Barclays Plc estimates.

That helped to push the whole yield curve in the euro area’s largest economy below 0% this year, sparking envy from U.S. President Donald Trump over Germany’s ability to get paid to borrow for 30 years.

“We still believe that the ECB is not done yet in terms of easing,” said Pooja Kumra, a strategist at Toronto-Dominion Bank in London, in a note. “European rates will be marked by the ‘QE infinity’ program and a more persistent negative policy rate.”

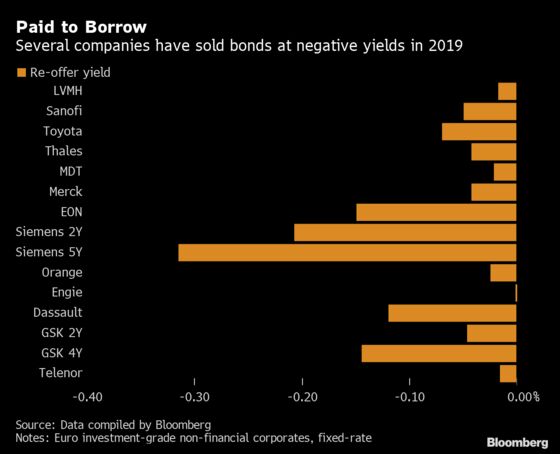

It’s not just governments who are likely to benefit. More companies will get the chance to raise new debt -- and get paid for doing so -- if fresh QE keeps sovereign bond yields well below zero and spreads continue to tighten.

Read More:

|

A dozen companies have already sold negative-yielding bonds this year. Almost 400 billion euros of investment-grade corporate bonds offer a negative return if held to maturity.

Of course, it’s not just QE that investors will have to deal with. After the ECB cut its deposit rate in September, traders in money markets are pricing in a 60% chance of another 10-basis-point drop to -0.6% by October next year. Should a German recession come before that, then it may not matter how negative bond yields are -- investors will have to buy to protect their portfolios.

“The door is open to more negative interest rates,” said Rabobank’s McGuire, who is targeting a drop in peripheral euro-area yields versus their German peers. “As more investors are forced to seek higher ground, then these sovereign interest costs will fall.”

--With assistance from Stephen Spratt, Vassilis Karamanis and Tasos Vossos.

To contact the reporters on this story: John Ainger in London at jainger@bloomberg.net;James Hirai in London at jhirai3@bloomberg.net

To contact the editors responsible for this story: Paul Dobson at pdobson2@bloomberg.net, Neil Chatterjee, William Shaw

©2019 Bloomberg L.P.