These Are the Signs Traders Are Watching for Quantitative Easing in Australia

These Are the Signs Traders Are Watching for Quantitative Easing in Australia

(Bloomberg) -- Explore what’s moving the global economy in the new season of the Stephanomics podcast. Subscribe via Pocket Cast or iTunes.

The weakest economic growth since the global financial crisis is fueling speculation the Reserve Bank of Australia will join its global peers and kick-start quantitative easing.

No fewer than seven central banks around the world have employed QE programs over the past decade, according to the Bank of International Settlements. Given this has become a well-trodden path, here are some of the tell-tale signs that show up in rate markets ahead of unconventional easing:

1. Flattening Yield Curve

Sovereign yield curves have a tendency to flatten in the run-up to QE. This occurs because shorter-maturity yields are pinned down close to the floor for the benchmark rate at the so-called “effective lower bound.” At the same time, longer-term yields are free to decline as investors buy the bonds in anticipation the central bank will step in as a buyer.

The RBA may cut its policy rate again in February to 0.5%, which is seen as its lower bound, according to Westpac Banking Corp. Asset purchases could then start over the course of next year, chief economist Bill Evans said last month.

The spread between French three- and 10-year yields shrank by half in the six months before the European Central Bank started its 60 billion euros ($66.5 billion) a month bond-purchase program in March 2015. It then bounced back as the ECB began its purchases.

In Australia’s case, the key thing to watch is also the three- to 10-year yield spread. The difference shrank to a nine-year low of 15 basis points in early September, but has since ticked back up to 37 basis points.

2. Widening Swap Spreads

A widening spread between bond yields and interest-rate swaps is also a signal of impending QE. Swap spreads tend to expand as markets begin to anticipate that bonds will benefit from fresh demand.

The spread widening can sometimes be tempered for shorter maturities as interest-rate cuts and other liquidity measures keep short-term rates suppressed. The move therefore manifests itself to a greater extent in the longer-end of the curve.

This was the European experience with German 30-year spreads widening by 30 basis points in the run up to the ECB’s 2015 bond-buying announcement. There’s little sign of this happening yet in Australia, but it is definitely something to watch.

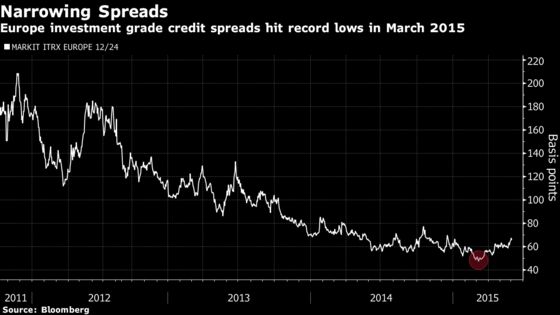

3. Narrower Corporate Spreads

The approach of QE also tends to feature a shrinking of corporate bond spreads. In Europe, investment-grade bond yields fell and credit spreads hit the tightest levels on record into the ECB’s buying wave. Spreads then rebounded as the decline in yields encouraged companies to take advantage of the more attractive funding levels by selling new bonds.

There was a record 60 billion euros of corporate debt sales in Europe in March 2015 when the ECB started QE.

The fact Australia’s government has a comparatively small amount of bonds on issue, about A$550 billion ($380 billion), means any RBA debt purchase-program would probably need to include corporate and semi-government paper and perhaps even mortgage-backed bonds, compressing their spreads to sovereign debt.

Australian credit spreads have tightened about 20 basis points this year, according to an index compiled by Bloomberg. The performance of these spreads is an important clue to the approach of QE, though it can be volatile.

Pacific Investment Management Co.’s Robert Mead, who is co-head of portfolio management for Asia Pacific, said the RBA has signaled it won’t allow its benchmark rate to become negative, which increases the likelihood it will start QE. Pimco has been buying local-currency bonds issued by top-rated semi-government borrowers, he said.

To contact the reporter on this story: Stephen Spratt in Hong Kong at sspratt3@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Nicholas Reynolds

©2019 Bloomberg L.P.