Ripples From Puerto Rico’s Debt Crisis Reach the Mainland

Ripples From Puerto Rico’s Debt Crisis Reach the Mainland

(Bloomberg Opinion) -- Joe Mysak, Bloomberg News’s foremost expert on the $3.8 trillion municipal-bond market, has a saying about Puerto Rico: It was technically “in” the market for state and local government debt, but not “of” it. That is to say, for a number of reasons, it has always been considered an outlier.

Indeed, munis are off to a blistering pace in 2019, with mutual and exchange-traded funds focused on the debt on track to pull in a record amount of cash this year. Investors are buying even though a closely watched gauge of relative value would suggest the bonds are a screaming sell. Never mind that at the start of the year, a federal oversight board argued that more than $6 billion of Puerto Rico’s general-obligation bonds should be declared null and void because issuing them in the first place breached the island’s constitutional debt limit. It’s just an outlier, after all.

Or is it?

John Tillman, the CEO of conservative think tank Illinois Policy Institute, and Warlander Asset Management’s Eric Cole, a protege of Appaloosa Management’s David Tepper, are teaming up in an effort to invalidate a whopping $14.3 billion of Illinois debt on the grounds that the state’s pension bond sale in 2003 and securities issued in 2017 to pay a backlog of unpaid bills were in fact deficit-financing transactions prohibited by the constitution. Some pertinent details from Bloomberg News’s Martin Z. Braun:

The group said the goal of the debt limits in the state constitution is to ensure the state acts in a financially responsible manner. But they claim “the state’s elected officials have done just the opposite. They have mortgaged the state’s future to pay for the present.” ...

Article nine, section nine of the Illinois Constitution says the state may issue long-term debt only to finance “specific purposes” if approved by three-fifths of the legislature or by popular referendum. ...

Using bond money to cover general expenses, speculate in the market, or pay past-due bills isn’t a “specific purpose,” for incurring state debt, but rather another name for deficit financing, the complaint said.

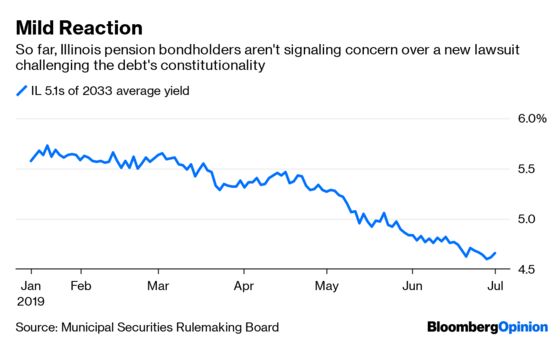

It’s still very early days, especially for this type of fundamental challenge to a state’s ability to finance itself. Illinois general obligations have long been considered to have some of the strongest legal protections among states. And most crucially, it’s not Illinois looking to invalidate its own debt but rather a hedge fund and Tillman, who has been at the forefront of legal challenges to public employee unions and progressive taxation. Even if they prevail, the state could very well repay investors entirely.

Illinois Comptroller Susana Mendoza, for her part, dismissed the lawsuit as “nothing more than garbage” and expects it to be “laughed out of court.”

Still, it looks to be the first significant ripple on the mainland from Puerto Rico’s unprecedented restructuring. As always, it raises the question of whether this is the final straw that will shake investors’ confidence in the market’s underpinnings.

Illinois is the natural starting place for this sort of reverberation. It’s the worst-rated U.S. state, clinging to the lowest investment grades from S&P Global Ratings and Moody’s Investors Service. The state’s unfunded pension liability is huge, about $168 billion, according to the complaint, and it struggled for years to pass a budget when the Republican governor at the time, Bruce Rauner, and the Democratic legislature couldn’t reach agreement. An effort in 2014 to increase revenue by replacing the state’s flat income tax with a progressive one was defeated, thanks in part to the Illinois Policy Institute.

So, yes, Illinois definitely has problems. But are they bad enough to wipe out a large chunk of bondholders? In theory, the move would free up billions of dollars in the coming years to fund pensions, but those savings could be wiped out by whatever extra yield investors would require to buy the state’s bonds in future offerings. It’s in Illinois’s best interest to make sure bondholders are repaid, even if this challenge isn’t struck down. It’s not nearly at the point yet at which it cares to risk the ire of the municipal market. Investors seem to get that, judging by Monday’s bond trading.

Puerto Rico, on the other hand, saw the writing on the wall years ago that its $70 billion debt load was unpayable. It was reeling from mass population exodus and high levels of poverty and joblessness, even before it was devastated by Hurricane Maria. It also had virtually no money left to pay pensioners.

There was no way out other than to have the oversight board created by Congress take drastic steps. In addition to attempting to nullify earlier bond sales, the board also sued dozens of banks and bondholders in May to claw back more than $1 billion in fees and interest payments. Two months earlier, an appeals court affirmed that Puerto Rico’s highway agency can tap tolls and other fees dedicated to bondholders until the bankruptcy is settled. That casts a pall over the rest of the market for revenue bonds sold for highways, airports and transit systems.

Braun noted in May that this isn’t the first time investors have fretted about precedent-setting events in the muni market, only to see their worst fears fail to materialize. Detroit’s bankruptcy, for one, has had no obvious long-term implications — in fact, the city easily issued $135 million of bonds in December, all with yields of less than 5%. Jefferson County, Alabama, which filed a then-record bankruptcy in 2011, had its credit rating raised to investment grade just four years later.

These examples suggest the muni market can withstand outliers. But compare the language in Illinois with that used in Puerto Rico. “The burden of servicing this unconstitutional debt falls on the taxpayers of Illinois, including Plaintiff John Tillman,” the complaint argued. Matthias Rieker, a spokesman for Puerto Rico’s oversight board, said in May with regards to invalidating bonds that “it is neither fair nor legal to burden Puerto Rico’s residents with that against which their Constitution protects them.”

The idea of pitting taxpayers against bondholders is one thing in an underdeveloped Florida community development district or a Missouri county that wants to be off the hook for a struggling retail project. It’s quite another at the level of the sixth-most-populous state. Illinois has options — dwindling ones, to be sure — to turn itself around without simply following in Puerto Rico’s footsteps. The same goes for Connecticut and New Jersey.

It might be too soon to say that Puerto Rico has opened up the muni market’s Pandora’s box. But this lawsuit against Illinois Governor J.B. Pritzker shows it’s at least cracked a little. It doesn’t truly matter if the challenge is coming from an oversight board, a hedge fund or the issuer itself. Either way, it reflects a threat to the core tenets of the market that no individual investor wants to see.

Specifically, according to the complaint, if the state ceases making principal and interest payments on the debt, it could contribute an additional $13 billion to its pensions over the next 14 years.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.