Private Equity Turns to $3 Trillion in Untapped Value for Loans

Private Equity Turns to $3 Trillion in Unlocked Value for Loans

(Bloomberg) -- Private equity firms on the hunt for capital are increasingly turning to specialty lenders for financing and providing a valuable asset as collateral: stakes in their funds.

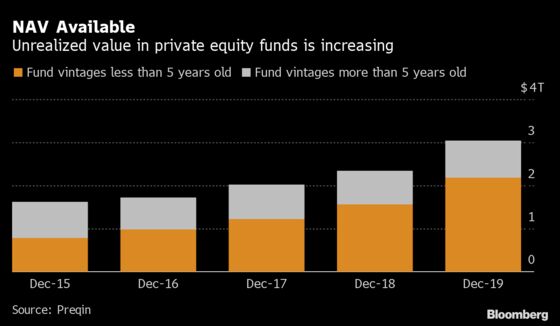

The buyout industry has about $3 trillion of unrealized value on its books, according to Preqin. And it’s tapping that to land loans for bolt-on deals, to refinance debt or bail out struggling companies in their portfolios.

Investors are racing to make loans. Lender 17Capital saw record demand and provided $1.5 billion of portfolio financing this year. U.K.-based Silicon Valley Bank, part of SVB Financial Group, did a year’s worth of deals in March alone. Investec Plc’s fund finance division has seen $4.5 billion of inquiries related to this financing through to September, more than double the value for 2019, a spokesman said.

“Volumes have gone through the roof,” said Pierre-Antoine de Selancy, co-founder of 17Capital, which manages around $5 billion. “Private equity portfolio companies will continue to need more cash as the economy struggles.”

Known as net-asset-value facility lending, the loans are popular primarily with mid-sized funds that hold assets that have appreciated in recent years. Because the loans are secured against the whole fund, lending rates are usually lower than the debt issued to finance the original buyouts.

“Private equity sponsors see a lot of flexibility in these types of loans,” said Brian Foster, fund finance partner at Cadwalader, Wickersham & Taft LLP. “They can leverage the stronger companies in an investment portfolio in order to deploy capital across the broader portfolio.”

Interest in such loans accelerated early on in the Covid-19 outbreak when credit markets seized and remains robust. NAV lender Crestline Investors has seen its deal pipeline increase by up to five-fold compared to 2019, according to managing director David Philipp. It recently loaned $30 million to an agricultural technology fund and $45 million to a real estate fund.

The International Private Equity and Venture Capital Valuation Guidelines, an industry body, has helped by giving the nod to temporarily smooth over Covid-related blips in earnings as revenues have plunged in sectors like hospitality.

Private equity has always had a lot of leeway when valuing NAV, said Christiaan de Lint, co-founder of Headway Capital Partners, a private markets investment firm based in London.

“Managers already play with earnings and multiples,” he said. “So the new guidance raised a great point for everyone: What is the actual NAV and how is it calculated?”

Some lenders have started to tighten standards.

17Capital partner Thomas Doyle said that, in the second quarter of this year, the firm established a 10% to 15% loan-to-value standard, down from 25% to 35% before the pandemic. The firm has become wary of funds that haven’t marked down their portfolios in 2020.

NAV loans can add a fourth level of debt in a private equity fund, said Gabriel Boghossian, partner in the private equity team at Stephenson Harwood LLP. That increases the risk that funds will breach covenants and cause losses to institutional investors .

Yet there’s no stopping the flow of NAV loans -- at least for now.

“The industry seems to have found another source of funding and they really like it,” said de Lint. “It’s not going away anytime soon.”

©2021 Bloomberg L.P.