Private Equity is Raising Dividend-Linked Debt Like It’s 2007

Private Equity is Raising Dividend-Linked Debt Like It’s 2007

(Bloomberg) -- Europe’s private equity patrons are piling debt onto the books of their companies to support dividend payouts, a move which could threaten these firms’ prospects when the fiscal and monetary stimulus of the pandemic era starts to wind down.

Just under 13 billion euros ($16 billion) of leveraged loan deals linked to dividend recapitalizations took place by early June -- the highest level in 14 years -- according to S&P Global Market Intelligence’s Leveraged Commentary & Data unit. That’s only 4 billion euros shy of the total for the same period in 2007, on the eve of the great financial crisis.

The stimulus deployed since March last year has kept many companies afloat amid ruinous lockdowns. Some private equity owners have seized the chance to issue more debt from their companies, potentially jeopardizing how quickly they can bounce back as economies start to open up and policymakers mull tapering.

“A dividend recap isn’t a positive credit scenario for any company,” said BlackRock Inc.’s Head of European Leveraged Finance James Turner. “But whether or not we decide to support them is dependent on each individual case.”

German buildings material maker Xella International GmbH, for instance, was downgraded after it sought to borrow 1.95 billion euros in March this year, with nearly a third of that amount slated to go to private equity sponsor Lone Star Funds.

S&P Global Ratings cited the dividend distribution in its downgrade report, saying it would negatively affect the company in the short-term. Further dividend payments in the near term would trigger another downgrade, it added. Lone Star declined to comment and Xella did not respond to a request for one.

Recovery Risk

Dividend recaps have on average put debt up by 0.5 times that of core earnings for the financing that’s repaid first in the event of insolvency, according to Marta Stojanova, director of European leveraged finance at S&P Global Ratings.

“The continued rise in first lien leverage has negatively impacted our expected recovery rates at default for most senior lenders,” she wrote in an email to Bloomberg News. Recovery rates are closely watched as a gauge of how much lenders can expect to recoup in the event of bankruptcy.

Investor Push-back

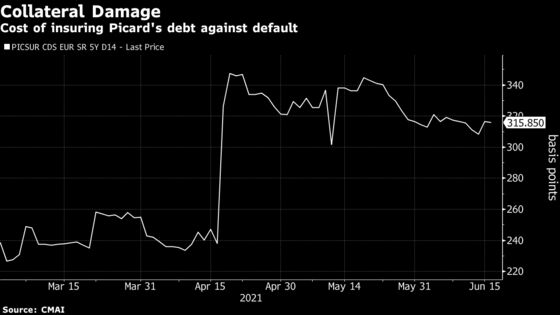

French frozen food retailer Picard Groupe SAS is another company that did well out of the pandemic and whose private equity sponsor sought to pay itself a dividend by getting the company to borrow more.

However the company pulled its 1.7 billion-euro bond offering on the grounds the debt would be too expensive. Owner Lion Capital had planned to pay itself 276 million euros, and went on to take a dividend three weeks later from another French company it owned.

Picard, on the other hand, was left with a negative outlook from Fitch Ratings. Neither company responded to a request for comment.

“The outlook remains negative for Picard as we believe the intention to relaunch a dividend recap still exists, suggesting a highly opportunistic financial behavior,” said Ed Eyerman, Fitch’s head of European leveraged finance.

Meanwhile, private equity sponsor Cinven has had to back off from a recent dividend-seeking attempt after investor resistance.

Scandinavian web-hosting company Group.One’s refinancing deal originally included a 65 million-euro element for Cinven. In the event, the company cut the loan size and will use the additional cash to grow the business.

Taper Risk

For the time being, the European Central Bank is continuing to support the environment that makes debt so cheap. After its latest meeting on June 10 the governing council said it would continue the policy until at least March 2022 or when it determines the end of the “coronavirus crisis phase.”

While the central bank’s asset-buying does not involve the junk-rated companies that private equity firms typically own, quantitative easing fosters the low interest rate environment that is driving debt-funded payouts.

“More leverage means more fragile companies,” said Ludovic Phalippou, professor of financial economics at Oxford’s Said Business School. “So, if another downturn arrives and if governments and others do not come to the rescue, then we will have a lot of financial bankruptcies to deal with.”

©2021 Bloomberg L.P.