Private Equity Billions Aren’t So Bad After All, Germans Concede

Private Equity Billions Aren’t So Bad After All, Europe Concedes

(Bloomberg) --

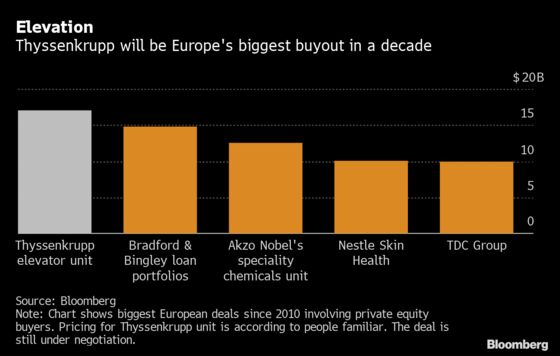

Once reviled by German politicians, private equity firms are now getting a warmer reception in Europe’s largest economy as industry heavyweights ink the continent’s biggest buyout deal in a decade.

Advent International and Blackstone Group Inc. are among firms planning to address several thousand of their peers in Berlin at this week’s SuperReturn International forum. Meanwhile, just a few hundred miles west, the bosses of Thyssenkrupp AG are deciding which of the two two buyout groups will triumph in a $17 billion battle for their crown-jewel elevator business.

The purchase could be one of the biggest global private equity deals this year -- and help cement Germany as a go-to destination for such firms. Buyers such as KKR & Co. pumped more than 30 billion euros ($32.6 billion) into the nation last year, snapping up some of its biggest and most-well known names such as Axel Springer SE.

It’s quite a turnaround from the 2000s, when Franz Muentefering, then-head of Germany’s Social Democratic Party, likened the firms to locusts for stripping companies of value and leaving an empty husk.

Even the labor unions have come around, supporting Thyssenkrupp selling to private equity instead of industry rivals, believing financial investors will be better at securing jobs. And in the takeover battle for Germany’s Osram Licht AG, worker representatives pushed, and eventually failed, to sell to private equity buyers after securing generous job guarantees.

“You’re seeing more large transactions where sponsors outbid strategic buyers,” said Simona Maellare, global co-head of financial sponsors at UBS Group AG in London. “For the private equity industry, that’s an upend and a shift.”

The reality is that private equity is one of the few games in town: it offers a white knight to yield-chasing investors and for companies eager to placate increasingly activist shareholders by selling off divisions. The industry last year raised $537.2 billion globally, the most since 2008, according to data compiled by Private Equity International.

European buyout funds are seeking to raise more than $80 billion this year, according to data provider Preqin Ltd. If they all succeed, that amount would mark an annual record for the region, the data show.

Private equity firms are no longer seen as the “bad guys,” says Stefano Sciolla, an Italy-based lawyer for Latham & Watkins. Compared to a decade ago, they’re far more accepted by business, government and regulators, he said.

Still, while private equity firms were sitting on a record $1.5 trillion of unspent capital at the start of this year, the continuous flow of cash may lead to more pressure to deploy money, and possible higher risk.

Investing money in this environment is probably the most difficult thing to do, said Philippe Poletti, head of the buyout team at Ardian, which manages $96 billion in assets. “You have to source deals differently and that’s why you need deep roots in the countries where you invest,” he said.

The challenge for private equity managers is deploying all the capital accumulated without overpaying and hurting returns. The average purchase prices for leveraged buyouts are hovering around all-time highs in the U.S. and Europe, according to a recent report from Bain & Company.

Firms that may start fundraising this year include Charterhouse Capital Partners and Nordic Capital, according to people familiar with the matter. CVC Partners is raising more than 18 billion euros, a record amount for its flagship fund, joining a flurry of other investment firms including CVC, EQT AB, Apax Partners and BC Partners.

Representatives for Charterhouse and Nordic declined to comment.

The total value of private equity-owned assets across Europe now account for between 5% to 10% of the region’s gross domestic product, Eurazeo SE Chief Executive Officer Virginie Morgon said in a speech at the IPEM conference in Cannes in January.

Private equity names are now commonplace on almost every large- and mid-cap deal with major industry players often appearing on both sides of the ticket. In the battle for Thyssenkrupp’s elevator unit, the shortlist of potential buyers comprises a consortium backed by Blackstone, Carlyle Group Inc. and Canada Pension Plan Investment Board, and a second group of Advent International, Cinven and the Abu Dhabi Investment Authority.

The rendezvous in Berlin between so-called general partners and their investors who meet in back-to-back speed dating sessions may give an indication how much longer the bullish deal flow will continue.

“SuperReturn has become an important barometer for the industry -- if it’s booming that’s when risk is up,” said Jim Strang, chairman for Europe, the Middle East and Africa at Hamilton Lane. “Private equity is still tiny and offers a good value proposition,” he said.

To contact the reporters on this story: Jan-Henrik Förster in London at jforster20@bloomberg.net;Benjamin Robertson in london at brobertson29@bloomberg.net

To contact the editors responsible for this story: Aaron Kirchfeld at akirchfeld@bloomberg.net, Chris Bourke, Elizabeth Fournier

©2020 Bloomberg L.P.