These Lenders Are Making A Growing Number of LBOs Possible

These Lenders Are Making A Growing Number of LBOs Possible

(Bloomberg) -- Private equity firms are finding that more leveraged buyouts of tech companies are becoming possible, thanks to lenders that have deeper pockets than ever: private credit firms.

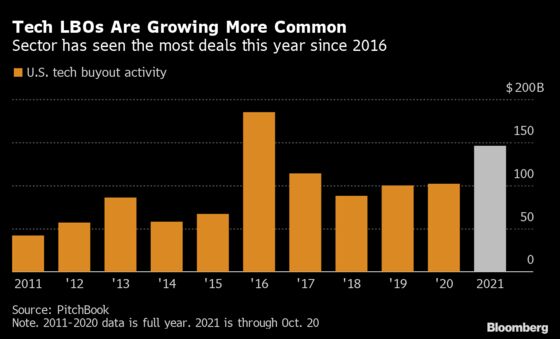

These lenders are providing financing to companies that wouldn’t be able to borrow as much in bond or leveraged loan markets. Private credit firms’ willingness to finance these kinds of deals is helping to fuel the highest volume of LBOs for tech companies since 2016. And they’ve enlarged the universe of publicly traded U.S. corporations that private equity firms can readily buy by somewhere around $550 billion.

“The sizable financing available from private credit is helping expand the scope of software or technology company transactions that PE can do,” said Dwight Scott, global head of Blackstone Credit.

The loans in question are either to companies that are burning through cash and don’t have enough earnings to pay interest, or to corporations that need more debt for a leveraged buyout than bond or syndicated loan markets will provide. Some of these financings can pay interest of 8 percentage points or more, far above yields available in other comparable markets.

For the buyout of Medallia Inc., a software maker, lenders including Blackstone, Apollo Global Management and KKR & Co. are giving $1.8 billion of debt financing. The company has negative earnings before interest, tax, depreciation and amortization, meaning it’s not making enough now to pay interest. Companies like these usually struggle to borrow in the leveraged loan or junk bond markets.

Read more in this week’s Credit Brief: Private Debt Expands LBOs; Fed’s Grinch

Blackstone, Owl Rock Capital Corp. and Apollo are privately lending $3.5 billion to private equity firms for the buyout of Inovalon Holdings, a healthcare software company. This deal, one of the biggest ever in direct lending, is saddling a company with a debt load far above what bond and loan investors would allow.

The lenders, often arms of private equity firms or standalone credit funds, have made loans like these for years at a much smaller scale. Now these asset managers are getting bigger and making larger loans. Private debt funds have $378 billion of dry powder, according to Preqin, the highest the data provider has ever recorded.

Tech companies seem like a good bet to many lenders, because they can generate so much money once they mature.

“The big question was what would happen in a business cycle,” said Matt Fleming, managing director at Antares. “We had a cycle last year during Covid, though it was very brief, and the sector outperformed every other sector.”

There have been around $145 billion of tech LBOs in 2021 through Oct. 20, and already more than every full year since 2016’s $185 billion, according to PitchBook. Private credit is only part of the reason for that jump, but it could drive more deals in the future.

Recurring Revenue

The Medallia financing is an example of a “recurring revenue loan,” where the company is losing money before it has even paid any interest. But these corporations usually have solid revenue under contract, high customer retention, and the deals have bigger equity cushions than other tech LBOs.

The targets in these deals are often too mature for loans from venture financing, but can now tap private credit firms. Lenders’ willingness to make larger recurring revenue loans has expanded the universe of publicly traded companies that can be bought out using debt by around $280 billion, according to a Bloomberg estimate.

The lending agreements contractually oblige borrowers to generate positive Ebitda within a few years. Bigger loans have shorter time frames, said Jake Mincemoyer, partner at Allen & Overy. Lenders view these companies as able to generate profit when they choose to, by cutting back on investments in areas like marketing.

“As recurring revenue loans get larger and larger, we’re lending to software companies that are approaching cash flow positive,” said Tiffany Gallo, managing director at Apollo. “They’re earlier in their life-cycle than those in the broadly syndicated market but are still very attractive credits.”

Two years ago, a $500 million recurring revenue loan was considered sizable. Now they can be twice that level or more. This kind of financing can generate an extra percentage point of annual interest compared with regular private loans.

That’s the sort of premium that has pulled investors into the market. Taylor Boswell, chief investment officer of direct lending at Carlyle Group, estimates that about 30 firms are making recurring revenue loans. The financing can make sense for lenders, Boswell said.

“They are more innovative and different from the traditional direct lending but not necessarily more risky,” Boswell said. “To succeed, you have to be highly selective with the credits you are willing to do.”

But the number of firms making these loans has roughly tripled from 2018, Boswell estimates. More lenders are entering the market, and not all have extensive experience with underwriting loans. Some worry about the rapid growth.

“If there is a fear I have about this space, it’s the possibility that new entrants will apply the structure to the wrong companies with poor revenue quality, at deeper leverage multiples, with looser covenants and lower economics,” said Brendan McGovern, president of Goldman Sachs BDC. “In credit, you can never underestimate the possibility for a good thing to go bad.”

More Leverage

For the other kind of loan, the LBO’s debt levels are substantially higher relative to earnings than possible in syndicated loans, traditionally the preferred market for financing buyouts. Banks that arrange syndicated loans do not underwrite deals that give borrowers debt loads of eight times their Ebitda or more.

And ratings firms will usually give too low a rating for such highly leveraged companies to sell debt easily to loan market investors like collateralized loan obligations, which have strict limits on what they buy.

In the private market, an LBO can sometimes be financed with debt equal to 10 times Ebitda or more. In the Inovalon deal, that figure is around 12 times Ebitda. Private credit’s willingness to make loans like these has increased the universe of potential tech LBOs by about another $270 billion, according to a Bloomberg estimate.

©2021 Bloomberg L.P.