(Bloomberg Opinion) -- Even China's IPO-mad retail investors are souring on the country's banks.

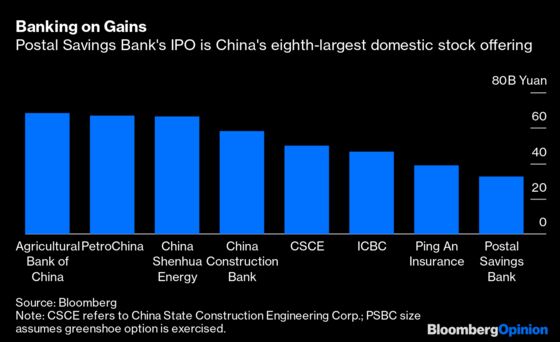

Postal Savings Bank of China Co. began trading with a whimper in Shanghai on Tuesday, after a 32.7 billion yuan ($4.6 billion) share sale that was the nation’s largest since 2010. The stock rose as much as 2.7% in morning trading, a fraction of the 44% limit that most newly listed shares hit on their debut.

So much for being a large state-owned lender with the world’s largest branch network. PSBC is free of the funding concerns that bedevil some smaller Chinese banks, with almost 40,000 branches supplying a wealth of deposits. China’s biggest lenders also come with a cast-iron state guarantee, being too big to fail. Investors have reason to run scared of smaller financial institutions since the government takeover of Baoshang Bank Co. in May. For larger lenders such as PSBC, the concern is more that they may be press-ganged into helping with profit-sapping rescues of weaker players.

But PSBC’s tepid debut isn’t just about the issues facing China’s banks: A skewed IPO system is also at fault.

Take the pricing dilemma. State-owned companies are barred from selling shares for less than book value, to prevent public assets from passing into private hands on the cheap. For banks, that translates into instantly overpriced deals. PSBC has been trading at about 0.8 times book in Hong Kong recently, according to data compiled by Bloomberg. That meant the Shanghai stock had to be priced at a premium. Early on Tuesday afternoon, PSBC was trading at the equivalent of about HK$6.20 — 19% higher than the Hong Kong-listed stock’s price of HK$5.19.

So the lack of a first-day pop could have been foretold. Hong Kong-listed Chongqing Rural Commercial Bank Co. was trading at only 0.5 times book when it went public in Shanghai on Oct. 29. It rose 27% on its debut, only to slump by the 10% limit the following day. China Zheshang Bank Co, meanwhile, climbed a mere 0.6% on its first day of trading last month — the worst mainland debut since 2012, according to data compiled by Bloomberg.

There are other distortions. Notably, there’s a valuation cap of 23 times earnings on initial public offerings on China’s domestic exchanges — except for those on Shanghai’s technology-focused Star board, which started trading in July. That’s why so many listings hit the 44% first-day limit. While PSBC and its ilk are forcibly overpriced, other issues are systematically underpriced.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nisha Gopalan is a Bloomberg Opinion columnist covering deals and banking. She previously worked for the Wall Street Journal and Dow Jones as an editor and a reporter.

©2019 Bloomberg L.P.