Policy Easing Chorus Gets Louder for Indonesia, South Korea

Policy Easing Chorus Gets Louder for Indonesia, South Korea

(Bloomberg) --

There’s a growing consensus between the swap markets and economists that central banks across emerging Asia are set to ease policy further. What nobody can agree on is whether rock-bottom interest rates will be enough to reignite growth and inflation.

In Indonesia, interbank rates and economists both signal at least one more 25-basis-point rate cut this year. For South Korea, forward swaps -- an indicator of future rate expectations -- and the majority of economists surveyed by Bloomberg also see another 25-basis-point rate cut by the end of the year.

As fears intensify about the outlook for trade and global growth, economists’ forecasts for upcoming rate decisions are starting to align with what traders expect. That’s a change from earlier this month, when forward-swap indicators showed traders expected monetary authorities in India and Thailand to ease but economists were caught off-guard by the larger-than-expected dovish moves.

“Expectations for rate easing are adjusting to the deterioration in data, but in some cases swap rates are pricing in even a more aggressive policy response than might be warranted,” said Radhika Rao, an economist at DBS Group Holdings Ltd. in Singapore. “Effectiveness of monetary policy, however, boils down to the speed and extent of transmission and can only go that far in stimulating growth" -- particularly if demand is the problem, rather than the supply of funds, she said.

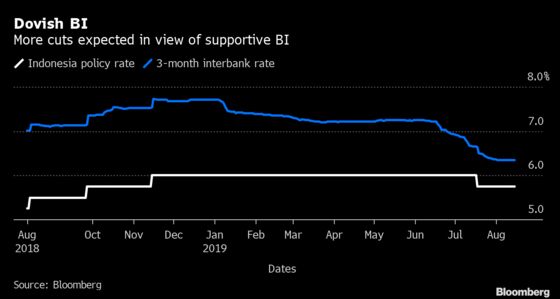

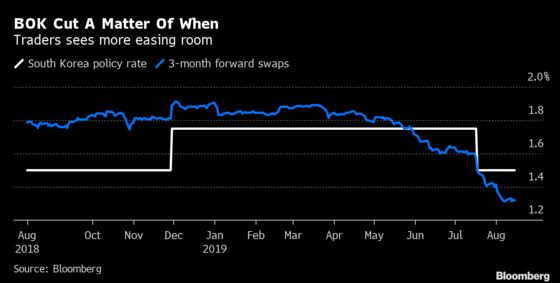

Here are some charts showing what rates markets are pricing in for Bank Indonesia -- due to decide on rates this week -- and for Bank of Korea, which meets at the end of the month.

The three-month interbank rate was trading around 65 basis points above Indonesia’s seven-day reverse repo policy rate ahead of the July meeting, and is now trading around 60 basis points above the new policy rate of 5.75%, signaling further easing expectations from Bank Indonesia. In contrast to the signals from the Thai central bank that confounded analysts, Bank Indonesia communicates its dovish intentions frequently, and has proactively limited declines in the rupiah, giving itself room for further easing.

Even so, any risk that could halt the recent strength in the rupiah and last Friday’s expansionary budget announcement may give the central bank reasons to pause. BI will hold the seven-day reverse repurchase rate at 5.75% on Thursday, according to 12 out of 19 economists surveyed by Bloomberg, though seven are still predicting a reduction.

South Korea surprised most economists in July by cutting rates 25 basis points to 1.5%, but traders were prepared: Forward swaps had been hovering about 18 basis points below the policy rate before the cut. Now they’re 21 basis points below the new policy rate, suggesting traders expect more easing. Eighteen out of 26 economists surveyed in August expect the key rate to fall to 1.25% by the end of the year, with one forecasting it at 1%.

READ: Traders Saw the Thailand Rate Cut That Surprised Economists

Governments will also have to loosen fiscal policy to have a significant impact, according to DBS’s Rao. Indonesia’s government is heeding this call, with President Joko Widodo’s budget announcement last week leaning on higher government spending to support the GDP growth target of 5.3% for 2020, the fastest since 2013.

“For a more direct and sector-specific support, fiscal stimulus might provide ‘more bang for the buck’ in lifting consumption and, broadly, demand,” she said. “Nonetheless, this also requires the respective economies to have the available room to raise spending and for consumers to be confident on their income prospects.”

--With assistance from Lilian Karunungan.

To contact the reporter on this story: Marcus Wong in Singapore at mwong547@bloomberg.net

To contact the editors responsible for this story: Tomoko Yamazaki at tyamazaki@bloomberg.net, Michael S. Arnold, Karl Lester M. Yap

©2019 Bloomberg L.P.