Playing to Preserve Capital, or Just Limit Losses: Taking Stock

Playing to Preserve Capital, or Just Limit Losses: Taking Stock

(Bloomberg) -- Sure, the number one goal of investors is to make money, but in times like this sometimes all you can do is look for the nearest lifeboat and hang on. Following yesterday’s slump hopes of a year-end rally are now pretty much gone, and with unpredictable political drama in the U.K., France and Italy, it has become nearly impossible for investors to guess what the next day will bring.

The Stoxx Europe 600 index has now erased more than two years of gains and reached an important level both technically, as the market is now in oversold territory, and psychologically, as the benchmark traded around that point during most of 2016. The visibility is so low that Allianz Global Investors, one of Europe’s biggest asset managers, is saying people should just sell the bounces and trim their exposure to stocks.

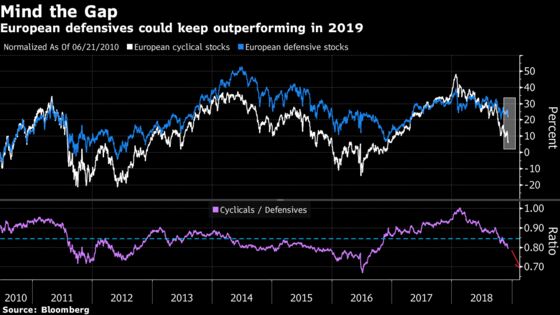

Any positive surprise aside, markets look set to move sideways and near their lows for the rest of the year with defensive sectors in favor. But as this rotation has been going on for a while this year, protecting capital is becoming more difficult. “The migration out of the most vulnerable cyclical and lower-quality stocks extends and positional risk is becoming more significant,” Kepler strategist Christopher Potts wrote in a note.

So while sticking to stocks with strong balance sheets and resilient earnings might not make investors immune from losses in a feeble market, some of them have held up well most recently. Looking at individual sectors, telecoms and utilities have been the best-performing industries on the Stoxx Europe 600 over the past three months, offering superior dividend yields. While European equities trade at 4 percent estimated dividend yield on average, telecoms and utilities trade at 5.6 percent and 5.5 percent respectively.

Because, while December is often the time of year when investors can just take stock on their performance, risks remain high in this market. The uncertainties surrounding Brexit are just mounting. By canceling the Parliament vote to go back to Brussels and try to get some final reassurance regarding the Ireland border, Prime Minister Theresa May has taken a big gamble. There is no date for the final vote and no guarantee she will get anything else from the EU, risking a no-deal crash-out. Looking at the pound trading 1.255 to the dollar and 1.106 to the euro, this is the risk currently being assessed.

As for France, the efforts made by French president Emmanuel Macron to defuse the “Yellow Vest” crisis are likely to weigh hard on the French budget. According to newspaper Les Echos, they come with a price tag of about 11 billion euros, and may leave the country will a budget gap of 3.5 percent of GDP in 2019. So much for the Italian budget debate.

Potts puts it this way: “The conversion of the investor community to the bearish interpretation of the investment world is proceeding more rapidly than we appreciated.” In his view, many market participants are just itching to sell on any decent year-end rally to cut risk just as long as so much uncertainly prevails. Meanwhile, the Euro Stoxx 50 future is trading up 1.1% ahead of the European open.

- Watch French stocks, including retailers Carrefour, Casino, Fnac Darty and Maisons du Monde, after French President Emmanuel Macron made a move on Monday evening to try to quell the “Yellow Vest” protests which have gripped the country in recent weeks. Also keep an eye on other French stocks including hotel owner Accor and toll road operators Vinci and Eiffage.

- Watch U.K. stocks and the pound as Theresa May makes a big gamble. The prime minister appears to be betting that by running down the clock on Brexit and by talking further with European Union negotiators, she’ll be able to eventually push a deal through closer to the deadline for Britain to leave in March. Ultimately, for U.K. assets, it means Brexit-related uncertainty shows no sign of ending any time soon.

- Watch trade-sensitive equities after Chinese and American trade officials spoke by phone as the two countries continue to attempt to work through their trade spat amid ongoing tensions over the arrest of the CFO of Chinese telecoms firm Huawei Technologies Ltd. No details came out of the discussions, but just the fact the two sides are still talking is probably a good sign and could help to underpin a recovery in European stocks today after the beating taken on Monday.

COMMENT:

- “We have spent most of the year worrying about the effects of higher U.S. bond yields on equity markets, and, in particular, how that would affect expensive Quality and Growth stocks, and conversely how it might benefit ‘beaten-up’ Value stocks,” Societe Generale strategists write in a note. “Our aversion to expensive Growth and Quality stocks and our relatively sanguine view on global Value despite significant economic slowdown concerns, is that Value stocks and cyclicals more generally have spent much of the year pricing in a slowdown already. Over the last few months, this has largely played out for Growth, but Quality has remained defensive and Quality Income (i.e., defensive with a high yield) has proved its relative worth during the sell-off.”

COMPANY NEWS AND M&A:

- Anheuser-Busch InBev’s credit rating was cut to the lowest tier of investment-grade by Moody’s Investors Service, which warned that the brewer is struggling to whittle down its $100 billion debt load.

- Vivendi is competing with Argyle Street Management to invest in the television operations of Indonesia’s largest media company PT Global Mediacom, people with knowledge of the matter said.

- Aurubis 4Q Sales Beat Estimates, Sees Moderate Pretax Decline

- Deutsche Bank Adds LBO Advisers, Equities Traders in U.S.: FT

- Alfa-Bank Discussed Potential Sale With VTB, UniCredit: FT

- Engie to Maintain Current Suez Stake: Les Echos

- Publicis to Pay EU1,000 Bonus to Some Employees in France

- Hornbach Holding 3Q Prelim. Adjusted Ebit Falls 31% Y/y

- Hornbach Baumarkt Cuts 3Q Adjusted Ebit View

- Saipem Assessing Impact of ‘Cyber Attack’ on Servers

- Santhera Adjusts Proposed Share Capital Increase to 5m Shares

- Icelandair Forgoes Share Capital Boost for Private Placement

- GBL Says Gallienne Becomes Sole CEO, Names Desmarais Chairman

- WPP Sees Restructuring Costs of GBP300M Over Next Three Years

- Danske Agrees to Sell Swedish Pension Assets for $286 Million

- Ashtead Second Quarter Adjusted Pretax Profit GBP347.8 Mln

NOTES FROM THE SELL SIDE:

- Morgan Stanley upgrades Covestro to overweight while cutting Givaudan to equal-weight, saying timing rotation into value is key next year. Looking to 2019, the bank says restoring consumer confidence in China remains critical to chemical sector demand, and expects companies to focus more and more on self help, with major M&A opportunities less likely following an active 2016/17.

- Citi writes Danone’s model is only in transition, not broken, and the stock’s current ~15% discount to peers on most valuation metrics is “unjustifiable,” reiterating its buy recommendation, and EU81 price target on the stock.

- Jefferies says European large-cap pharmaceuticals stocks are entering a period of sustained earnings momentum which should justify valuations above the historic average for the sector. Roche (buy) is the preferred name on confidence in earnings momentum and underappreciated pipeline. GlaxoSmithLine, Novartis and Sanofi are all rated buy; AstraZeneca and Novo Nordisk are rated hold.

- Berenberg believes Superdry’s “dreadful year” probably continued and cut its recommendation to hold from buy (PT to 950p from 1,200p). The broker cites the latest retail sector data and comments from international clothing peer Primark, providing little evidence of an improvement in trading since Superdry’s last update.

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 341.4 (61.8% Fibo); 353.2 (50% Fibo)

- Support at 326.5 (74.4% Fibo); 302.6 (100% Fibo)

- RSI: 29.3

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,072 (61.8% Fibo); 3,193.5 (50% Fibo)

- Support at 2,921 (76.4% Fibo); 2,678 (100% Fibo)

- RSI: 30.4

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- Aviva upgraded to top pick at RBC; Price Target 5.40 Pounds

- Barry Callebaut raised to hold at Mirabaud Securities

- Covestro upgraded to overweight at Morgan Stanley; PT 60 Euros

- Lancashire upgraded to outperform at RBC; PT 7.25 Pounds

- Nordex upgraded to buy at Goldman; PT 11 Euros

- Partners Group raised to outperform at Macquarie; PT 770 Francs

- Sanofi upgraded to buy at Jefferies; PT 90 Euros

- Unicaja Banco raised to buy at Ahorro Corporacion; PT 1.39 Euros

DOWNGRADES:

- BASF downgraded to hold at Kepler Cheuvreux; PT 60 Euros

- Derwent London cut to equal-weight at Barclays; PT 29 Pounds

- Givaudan cut to equal-weight at Morgan Stanley; PT 2,400 Francs

- Lindt & Spruengli cut to sell at Mirabaud Securities

- Phoenix cut to outperform at RBC; Price Target 8.20 Pounds

- Photo-Me downgraded to hold at Kepler Cheuvreux; PT 1.15 Pounds

- Standard Life Aberdeen cut to sector perform at RBC

- Superdry downgraded to hold at Berenberg

- Tod’s downgraded to reduce at HSBC; PT 37 Euros

INITIATIONS:

- Workspace rated new overweight at Barclays; PT 9.80 Pounds

MARKETS:

- MSCI Asia Pacific down 1.8%, Nikkei 225 down 0.3%

- S&P 500 up 0.2%, Dow up 0.1%, Nasdaq up 0.7%

- Euro up 0.08% at $1.1365

- Dollar Index down 0.09% at 97.14

- Yen up 0.17% at 113.14

- Brent up 0% at $60/bbl, WTI up 0% to $51/bbl

- LME 3m Copper up 0.7% at $6132.5/MT

- Gold spot up 0.2% at $1246.5/oz

- US 10Yr yield up 0bps at 2.86%

MAIN MACRO DATA (all times CET):

- 8:45am: (FR) 3Q F Wages QoQ, est. 0.3%, prior 0.3%

- 10:30am: (UK) Nov. Claimant Count Rate, prior 2.7%

- 10:30am: (UK) Oct. Average Weekly Earnings 3M/YoY, est. 3.0%, prior 3.0%

- 10:30am: (UK) Oct. ILO Unemployment Rate 3Mths, est. 4.1%, prior 4.1%

- 10:30am: (UK) Oct. Employment Change 3M/3M, est. 25,000, prior 23,000

- 11am: (GE) Dec. ZEW Survey Current Situation, est. 55, prior 58.2

- 11am: (GE) Dec. ZEW Survey Expectations, est. -25, prior -24.1

- 11am: (EC) Dec. ZEW Survey Expectations, prior -22

--With assistance from Hanna Hoikkala.

To contact the reporters on this story: Jan-Patrick Barnert in Frankfurt at jbarnert3@bloomberg.net;Michael Msika in London at mmsika4@bloomberg.net

To contact the editors responsible for this story: Celeste Perri at cperri@bloomberg.net, Jon Menon

©2018 Bloomberg L.P.