Pimco Lays Out Australian Bond Playbook as QE Talk Grows

Pimco Lays Out Australian Bond Playbook as QE Speculation Grows

(Bloomberg) -- Pacific Investment Management Co. expanded holdings of Australian state debt and Kangaroo bonds sold by top-rated borrowers as the prospect of further policy easing in the nation boosts their attractiveness.

The Reserve Bank of Australia will probably cut interest rates once more before potentially embarking on quantitative easing to spur inflation, according to Robert Mead, Pimco’s co-head of portfolio management for Asia Pacific. The money manager has turned neutral from overweight on Australian sovereign debt, he said in an interview from Sydney.

Debate over the likelihood of QE in Australia is picking up pace with economists arguing that one more rate cut will bring the central bank to the lowest policy level it can tolerate. A small sovereign debt market, which has rallied through the year as RBA slashed rates to a record low, suggests that any systemic asset purchases may need to cover a wider pool of securities.

“Any sort of QE that was targeted at that end of the spectrum would be largely ineffective,” Mead said, referring to sovereign bonds. “That leaves buying other assets that could be supportive whether that be residential mortgage-backed securities, or credit,” even though nothing is cheap any more, he added.

In such an environment, even the very low-risk securities, such as the semi-government bonds, will be very well supported, he said. “We’re very happy even though yields look low,” said Mead, who helps oversee the Pimco Australian Bond Fund which beat 92% of peers this year.

The RBA slashed its cash rate to 0.75% in October, the third reduction this year, and said it’s prepared to ease again to support growth and fuel inflation. Yields on 10-year sovereign notes have tumbled to as low as 0.85% in August from 2.37% in January.

The room for further rate cuts could be limited, with Westpac Banking Corp.’s influential economist Bill Evans arguing that a 0.5% policy rate could be the lower bound. RBA Governor Philip Lowe has also said that negative interest rates are “extraordinary unlikely.”

Massive purchases of sovereign bonds may be challenging, with Australia’s net government debt amounting to 21% of its gross domestic product. That compares with 81% in the U.S. and 154% in Japan.

Widening Spreads

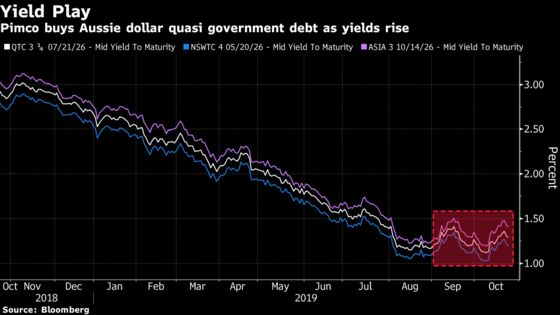

Pimco has snapped up Kangaroo bonds -- Aussie dollar debt sold by offshore institutions -- and local-currency notes issued by top-rated semi-government borrowers due in five to seven years where spreads have widened against sovereign paper, Mead said.

Sales of Kangaroo bonds swelled to A$10.7 billion ($7.3 billion) last quarter, the largest for a three-month period in more than a year, according to data compiled by Bloomberg.

Mead’s other comments on Australia:

We know that since central banks globally moved into negative rates territory, none of them have really been comfortable in the negative rates space. So for central banks that haven’t been into negative territory so far, I think it’s unlikely that they do anytime going forward.

The RBA has suggested that they wouldn’t go negative, they’ve intimated that QE or some form of alternative support will start before interest rates got to zero.

The thing to bear in mind though is when other central banks around the world first embarked on QE, assets were cheap. So for a central bank to start down the QE path now, there’s nothing cheap.

Our pension system in Australia is way underweight in fixed income anyway, so do we really want the central bank to buy even more?

If you put the whole mosaic together, as a bond investor you can have a high degree of comfort that interest rates might go up a little bit but they won’t go up much.

Fed Cuts

Mead also favors U.S. Treasuries, predicting that the Federal Reserve may deliver up to three more rate cuts should the U.S.-China trade conflict drag on. Policy makers could ease less than that if there is a resolution as “both sides now have enough real data to suggest that the trade war is contributing to this window of weakness” in growth, he said.

“We still see U.S. duration or U.S. Treasuries as one of the preferred defensive assets still available,” Mead said. Treasuries are “a place you want to be overweight versus areas like Europe, the U.K., Japan,” he said.

--With assistance from Stephen Spratt.

To contact the reporter on this story: Ruth Carson in Singapore at rliew6@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Liau Y-Sing

©2019 Bloomberg L.P.